Australian Government Bond Yield Curve & Rates

Get Australian Government Bond Yield Curve Data across all standard maturities, from 1-year to 30-year bonds, updated daily.

We give you the clean, structured data you need without the overhead of a Bloomberg terminal.

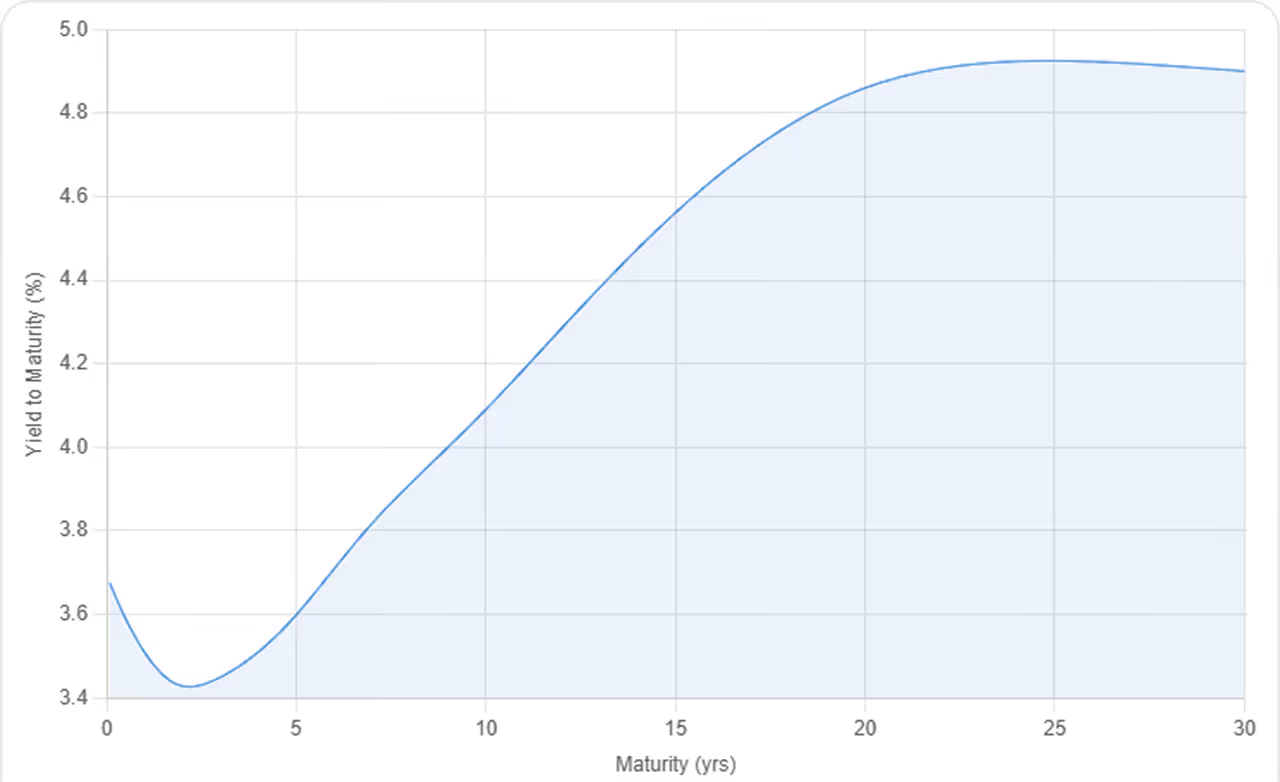

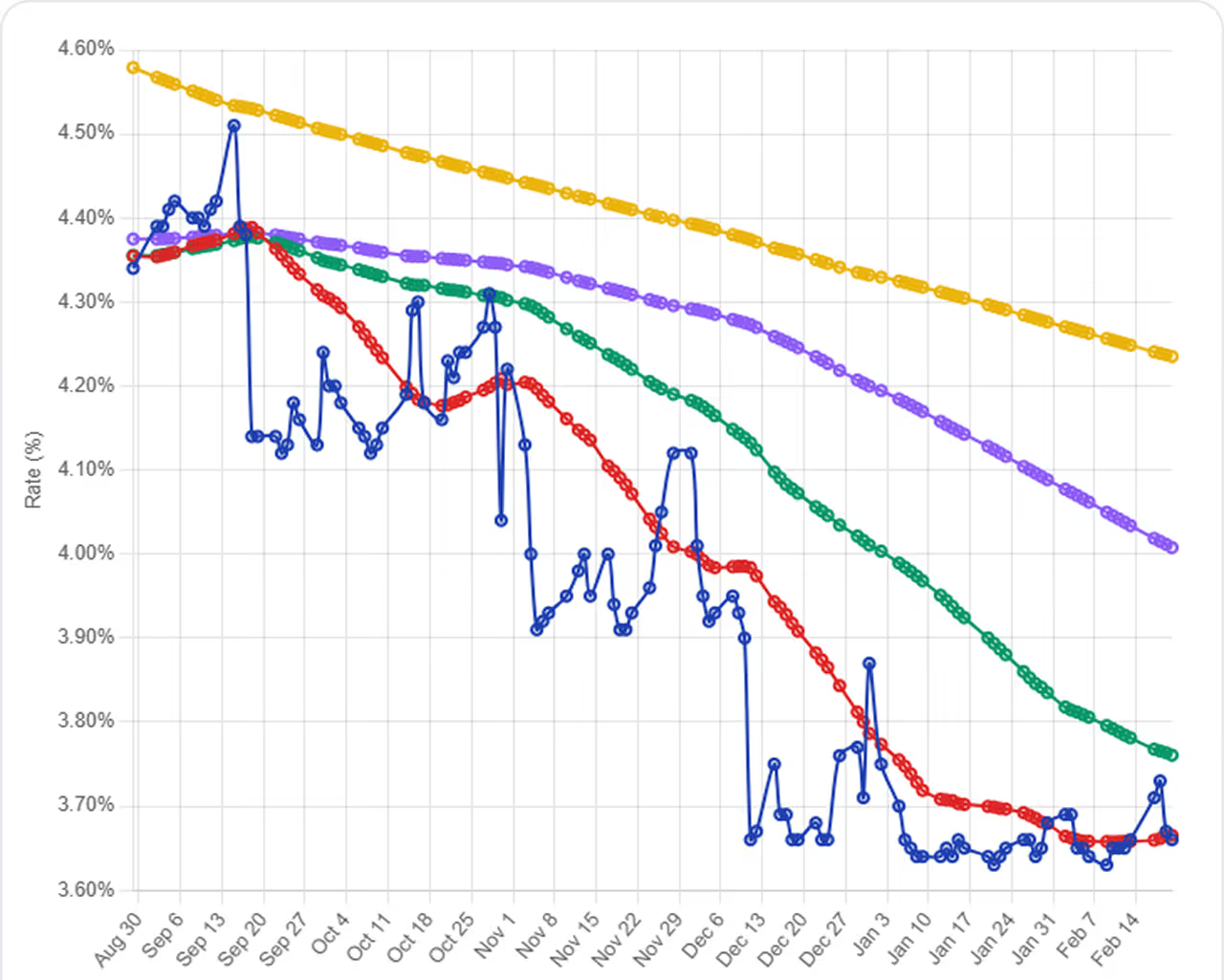

Access Government Bond Yield Curves

Get full government bond yield curves for Australia across all standard maturities, from 1-year to 30-year bonds, updated daily.

Ideal for treasury teams automating daily reporting, quant desks feeding pricing models, or fintechs building rate-dependent products.

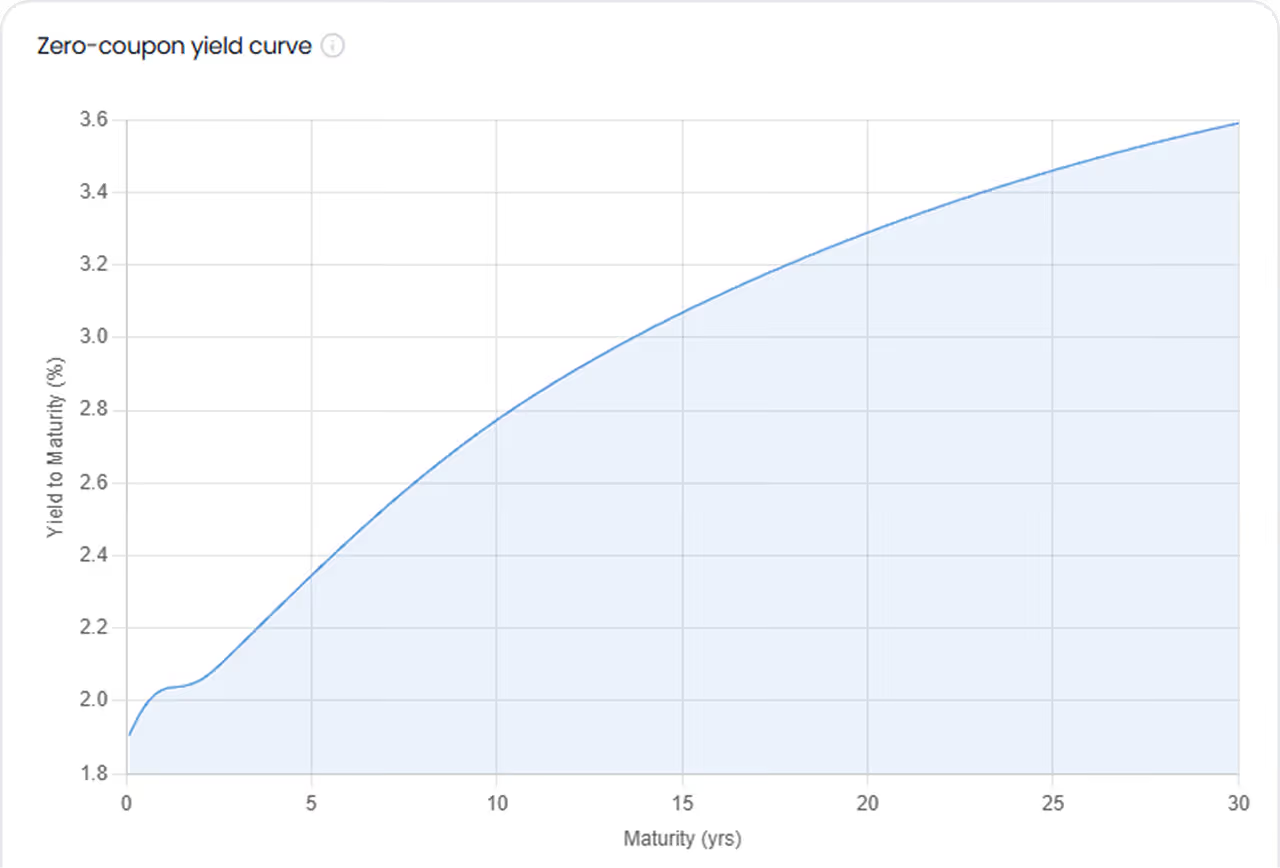

Easily Download Zero-Coupon Yields

Bootstrapped zero-coupon yield curves are essential for accurate discounting, bond valuation, and derivatives pricing, but building them yourself is time-consuming and error-prone. We do the heavy lifting for you, delivering bootstrapped zero-coupon rates for Australian government bonds daily.

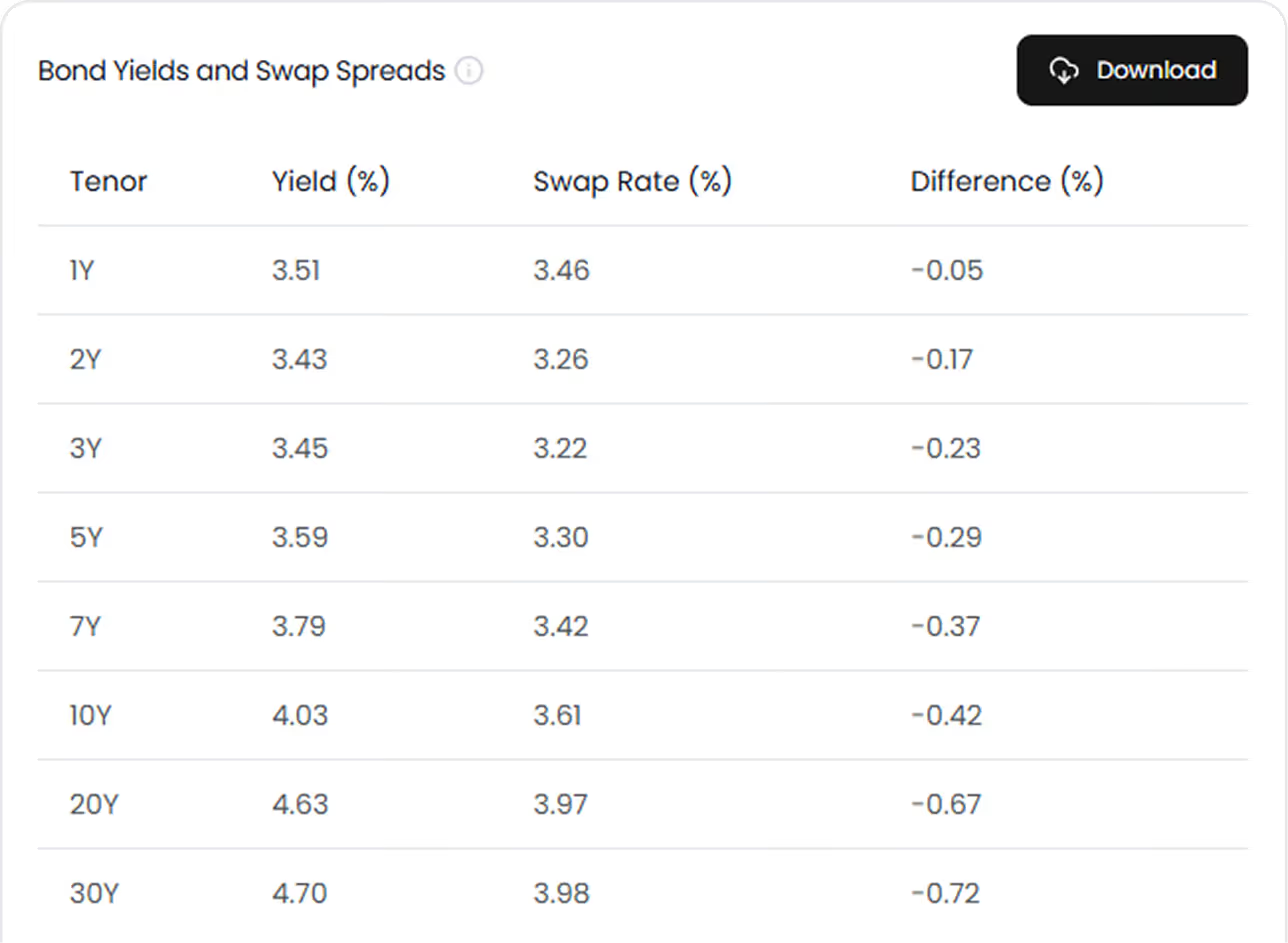

Access Swap Spreads for All Major Countries

We provide swap spread data for all major sovereign curves, so you can monitor the gap between government bond yields and interest rate swap rates across maturities.

Use our data to track swap spread dynamics over time, compare across countries, and identify relative value opportunities between government bonds and the swap market.

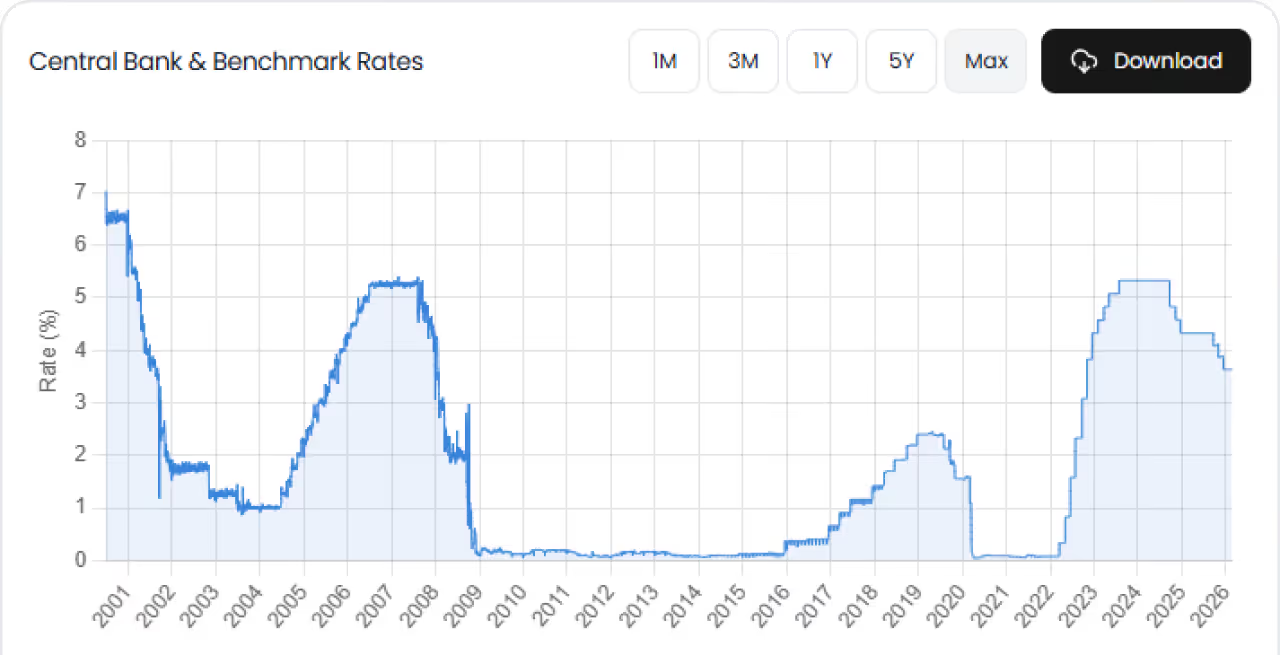

Access All Central Bank Benchmark Rates

Whether you're tracking the Fed, the ECB, the Bank of England, or the Bank of Japan, you get clean, current and historical timestamped data in a single platform. No more scraping central bank websites or reconciling inconsistent sources.

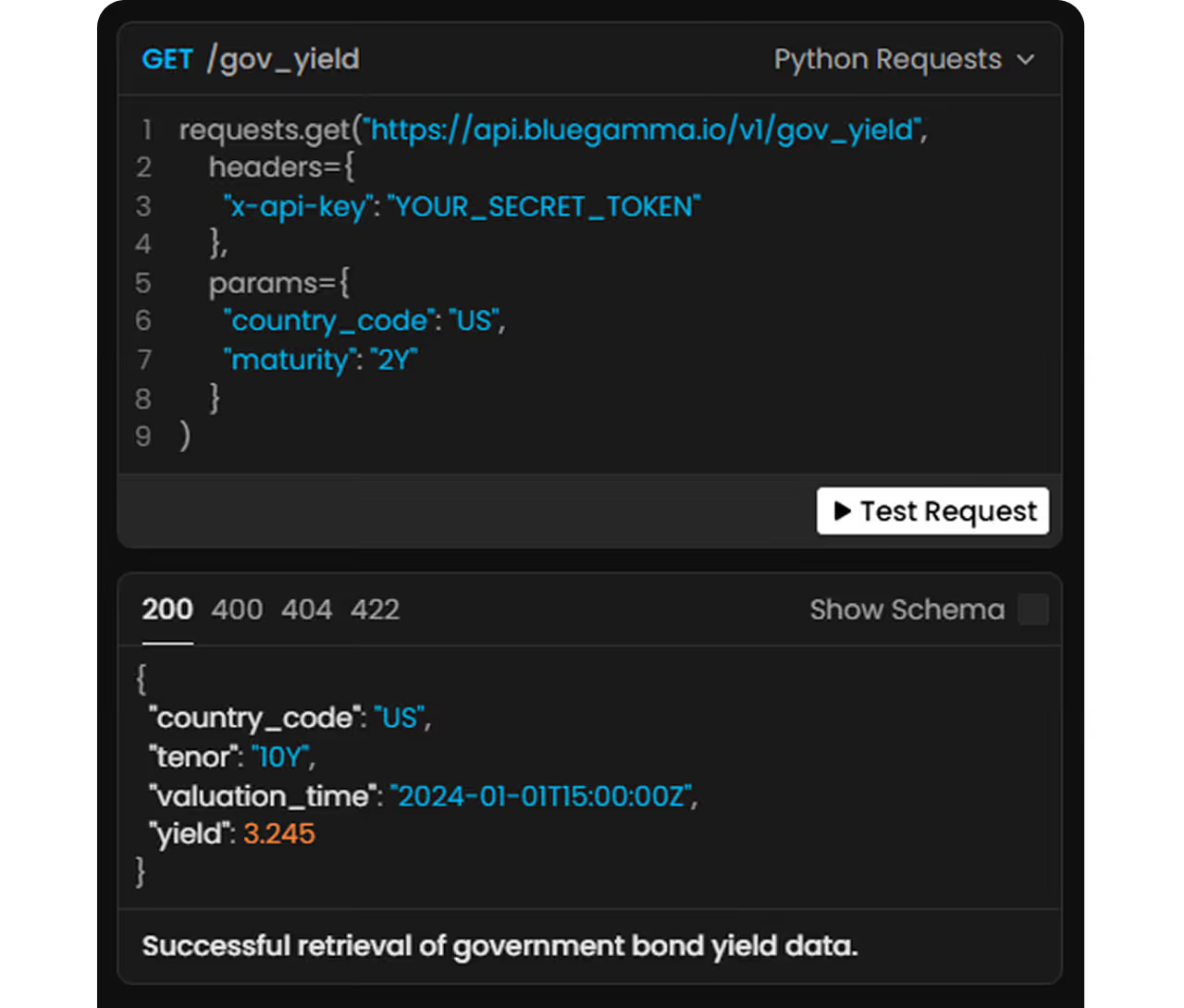

Use our Interest Rate API to Easily Integrate Government Yield Data at Scale

Our REST API lets you pull government bond zero-coupon yield curves and benchmark rates directly into your models, dashboards, and applications. Endpoints are designed for quant workflows, request by country and date to get back clean JSON.

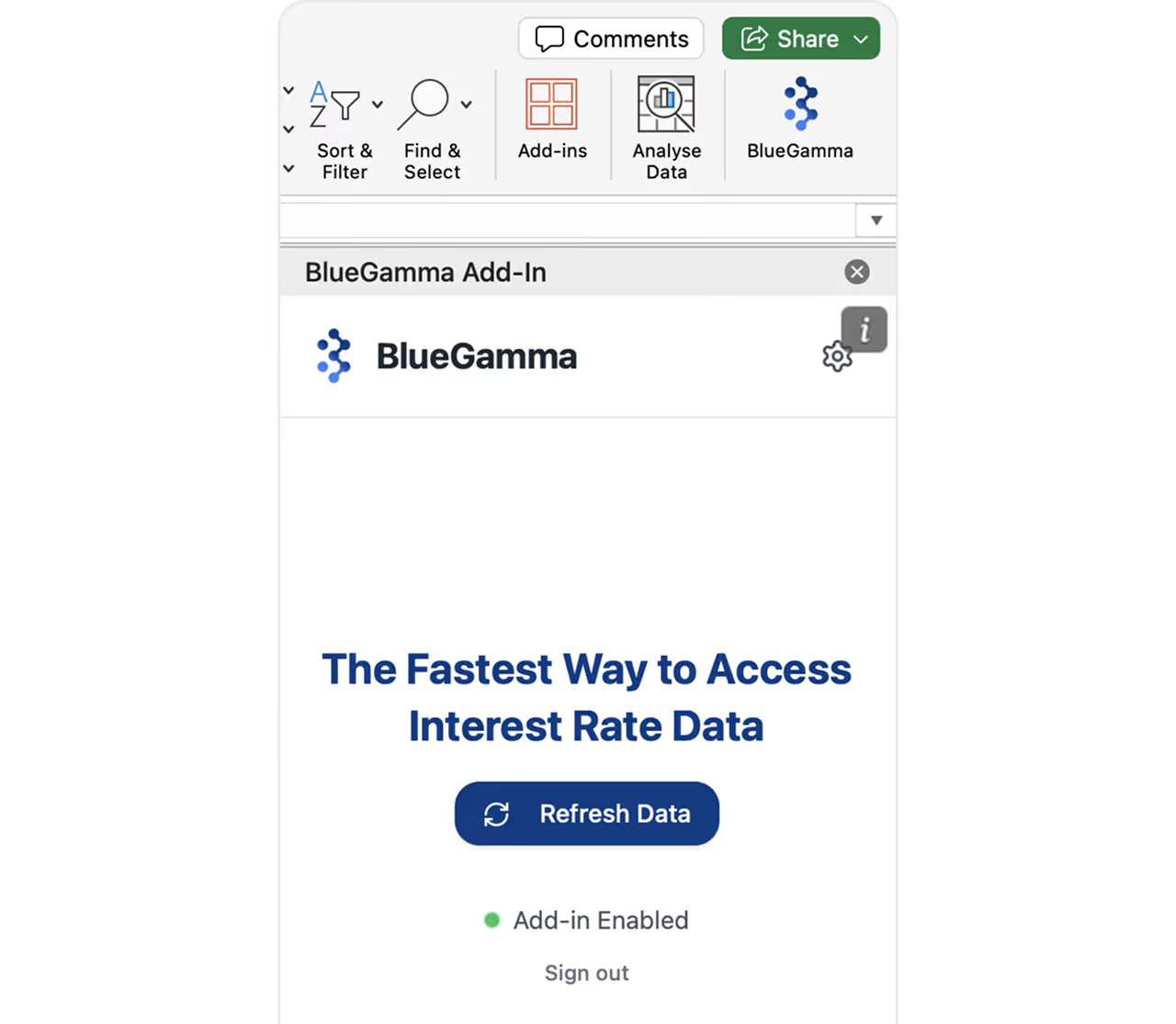

Download our Excel Add-In to Quickly Pull Rates Data

Our Excel Add-In lets you pull live and historical government bond yield curves directly into your spreadsheets with simple formulas. Build dynamic models that refresh automatically, no copy-pasting, no manual downloads.

Related Government Bond Yield Curves

US Treasury Government Bond Yield Curve

Real-time US Treasury government bond yields and yield curve data.

UK Gilt Government Bond Yield Curve

Real-time UK Gilt government bond yields and yield curve data.

Canadian Government Bond Yield Curve

Real-time Canadian government bond yields and yield curve data.

German Government Bond Yield Curve

Real-time German government bond yields and yield curve data.

French Government Bond Yield Curve

Real-time French government bond yields and yield curve data.

Brazilian Government Bond Yield Curve

Real-time Brazilian government bond yields and yield curve data.

Japanese Government Bond Yield Curve

Real-time Japanese government bond yields and yield curve data.

Indian Government Bond Yield Curve

Real-time Indian government bond yields and yield curve data.

Swiss Government Bond Yield Curve

Real-time Swiss government bond yields and yield curve data.

New Zealand Government Bond Yield Curve

Real-time New Zealand government bond yields and yield curve data.

Spanish Government Bond Yield Curve

Real-time Spanish government bond yields and yield curve data.

Turkish Government Bond Yield Curve

Real-time Turkish government bond yields and yield curve data.

Mexican Government Bond Yield Curve

Real-time Mexican government bond yields and yield curve data.

Italian Government Bond Yield Curve

Real-time Italian government bond yields and yield curve data.

Swedish Government Bond Yield Curve

Real-time Swedish government bond yields and yield curve data.

Chinese Government Bond Yield Curve

Real-time Chinese government bond yields and yield curve data.

Greek Government Bond Yield Curve

Real-time Greek government bond yields and yield curve data.

South African Government Bond Yield Curve

Real-time South African government bond yields and yield curve data.

Dutch Government Bond Yield Curve

Real-time Dutch government bond yields and yield curve data.

Austrian Government Bond Yield Curve

Real-time Austrian government bond yields and yield curve data.

Chilean Government Bond Yield Curve

Real-time Chilean government bond yields and yield curve data.

Danish Government Bond Yield Curve

Real-time Danish government bond yields and yield curve data.

Egyptian Government Bond Yield Curve

Real-time Egyptian government bond yields and yield curve data.

Finnish Government Bond Yield Curve

Real-time Finnish government bond yields and yield curve data.

Indonesian Government Bond Yield Curve

Real-time Indonesian government bond yields and yield curve data.

Kenyan Government Bond Yield Curve

Real-time Kenyan government bond yields and yield curve data.

Malaysian Government Bond Yield Curve

Real-time Malaysian government bond yields and yield curve data.

Nigerian Government Bond Yield Curve

Real-time Nigerian government bond yields and yield curve data.

Norwegian Government Bond Yield Curve

Real-time Norwegian government bond yields and yield curve data.

Polish Government Bond Yield Curve

Real-time Polish government bond yields and yield curve data.

Portuguese Government Bond Yield Curve

Real-time Portuguese government bond yields and yield curve data.

Romanian Government Bond Yield Curve

Real-time Romanian government bond yields and yield curve data.

Saudi Arabian Government Bond Yield Curve

Real-time Saudi Arabian government bond yields and yield curve data.

South Korean Government Bond Yield Curve

Real-time South Korean government bond yields and yield curve data.