New features & improvements added in April

New features

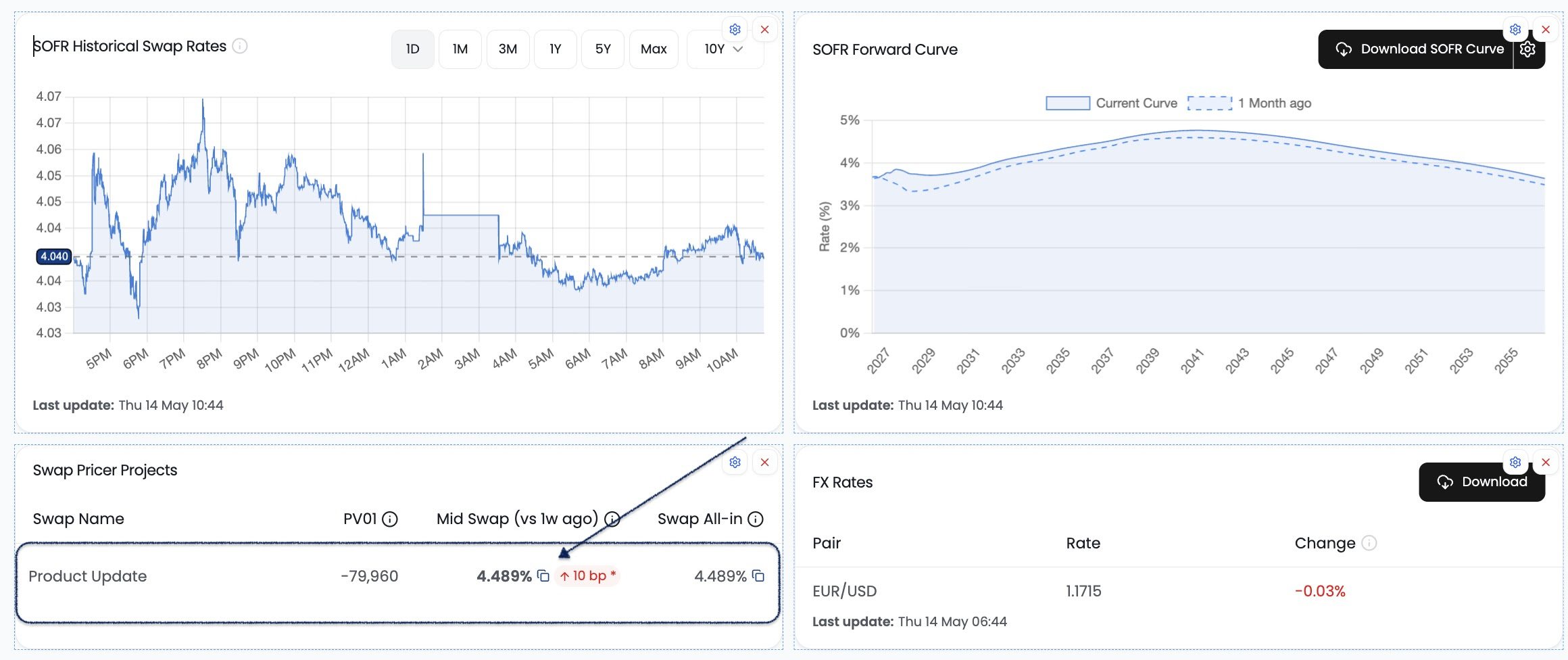

New Swap dashboard widget

You can now pin swaps from Swap Pricer and Swap MtM to your custom dashboards.

This means you can track the rate or value of a specific swap alongside other market variables like historical swap rates, forward curves, and FX rates - helping you stay better informed when discussing that swap or the wider market.

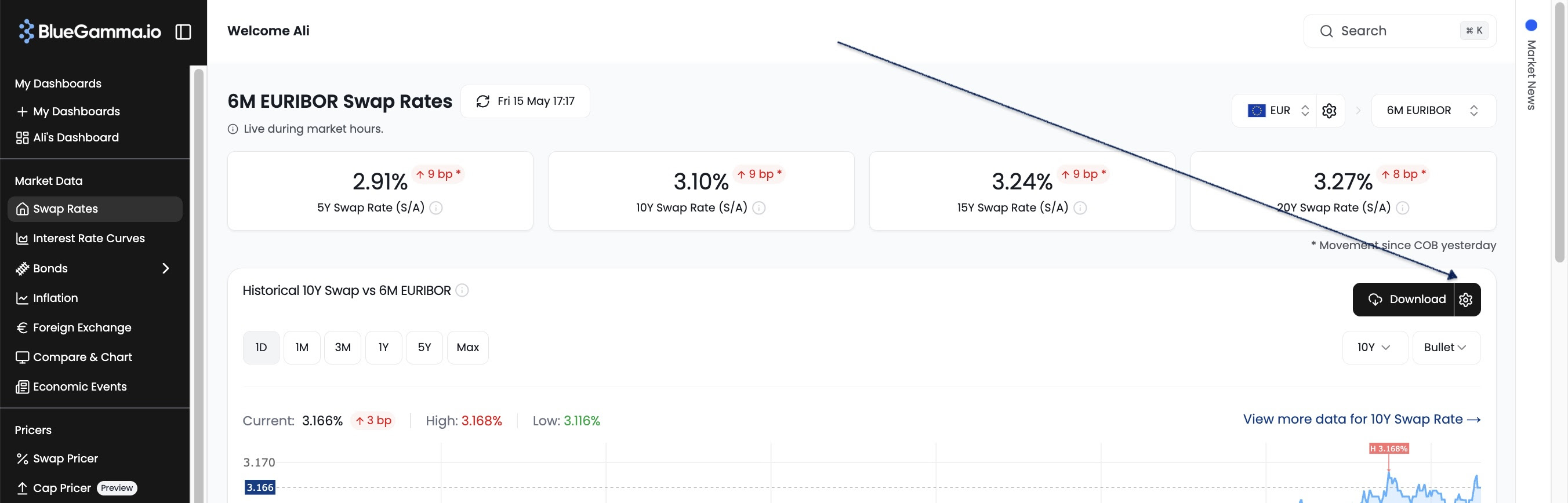

Easier historical rates download

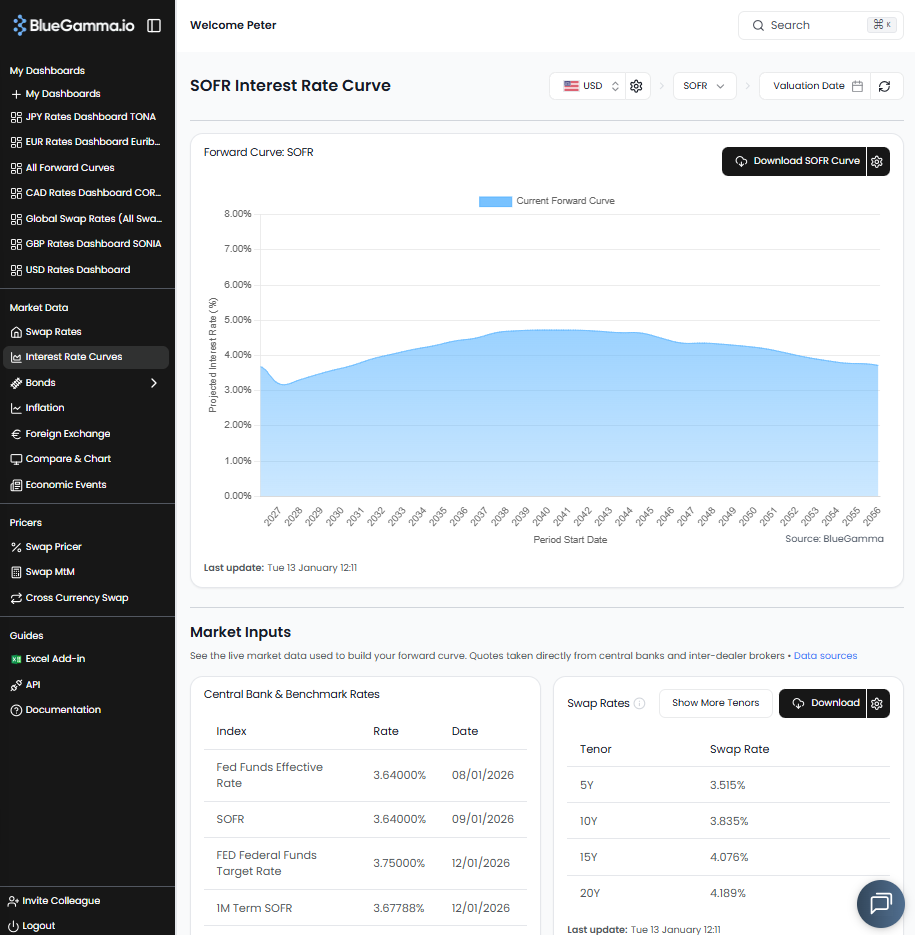

You can now select multiple tenors and download them in a single file from the home page.

This removes repetitive manual exports and makes it much faster to pull curve data into Excel models.

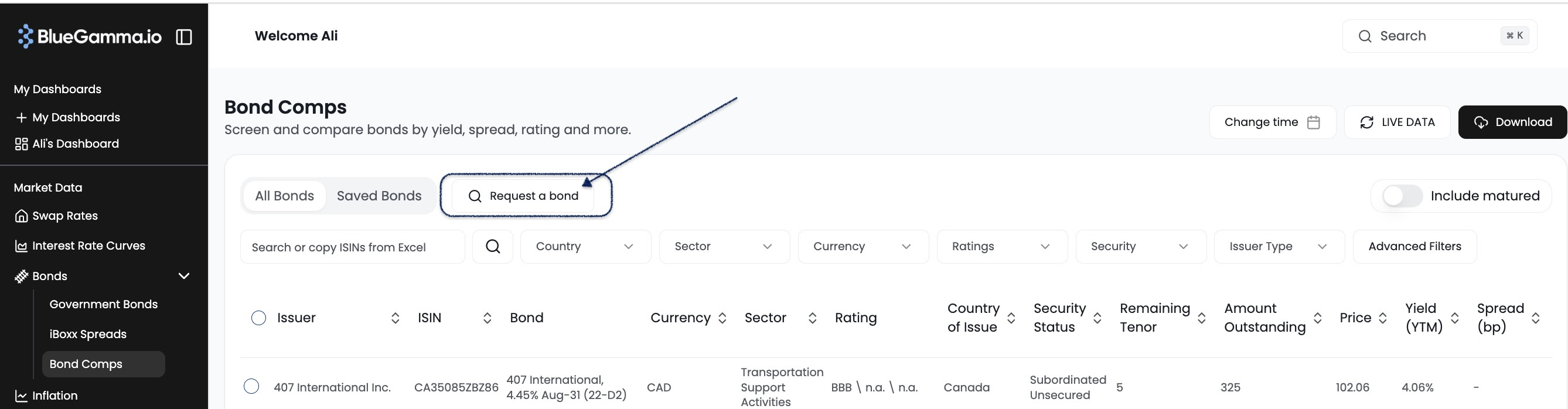

Bond comparables request flow

You can now request a specific bond by submitting an ISIN and an optional note.

Requests now go straight to our support team, helping remove the old email back-and-forth and speeding up the process.

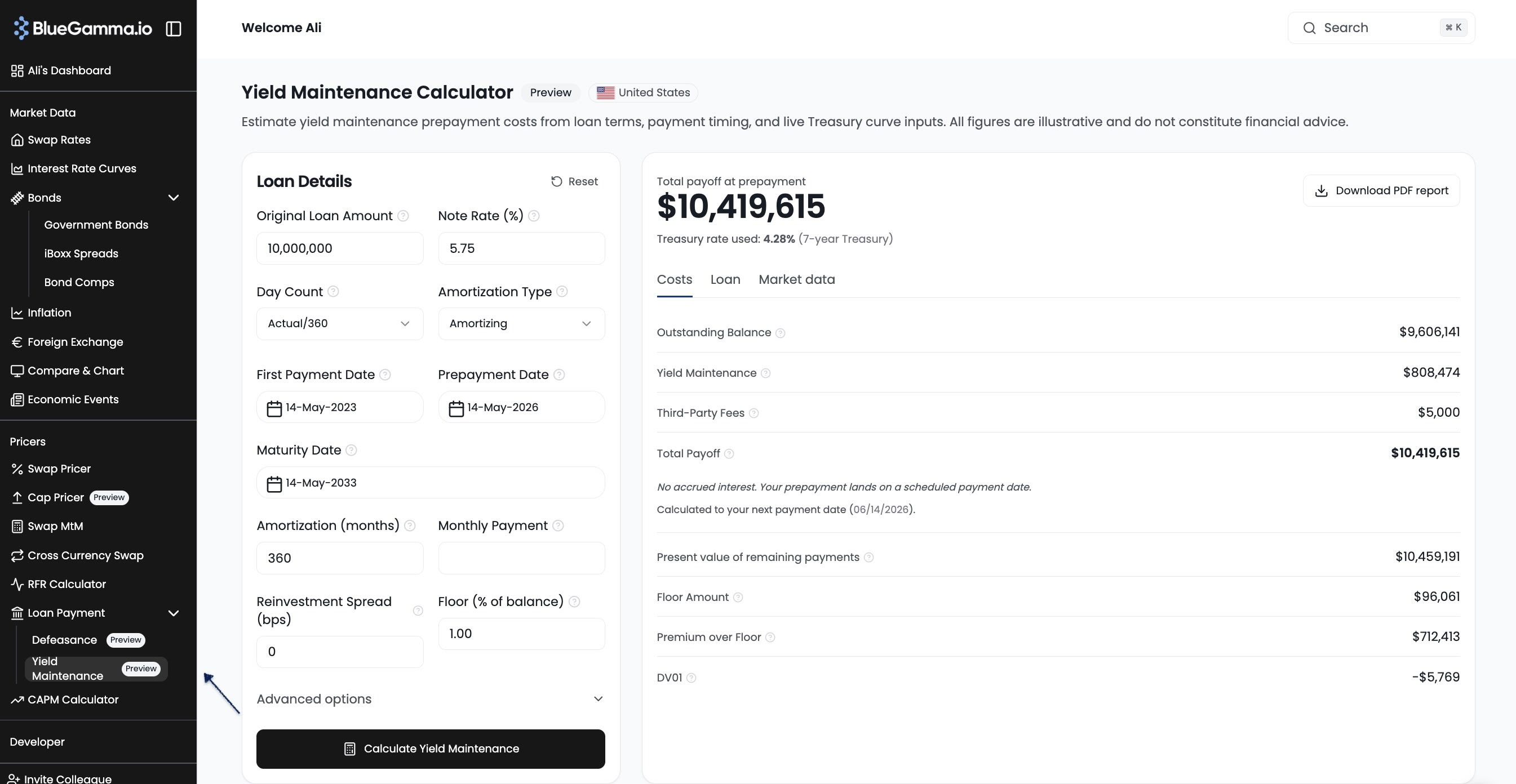

Yield Maintenance Calculator

Our Yield Maintenance Calculator is now live.

You now get live Treasury curves, optional Treasury overrides, payment discounting breakdowns, prepayment burndown charts, and PDF export - all in one place.

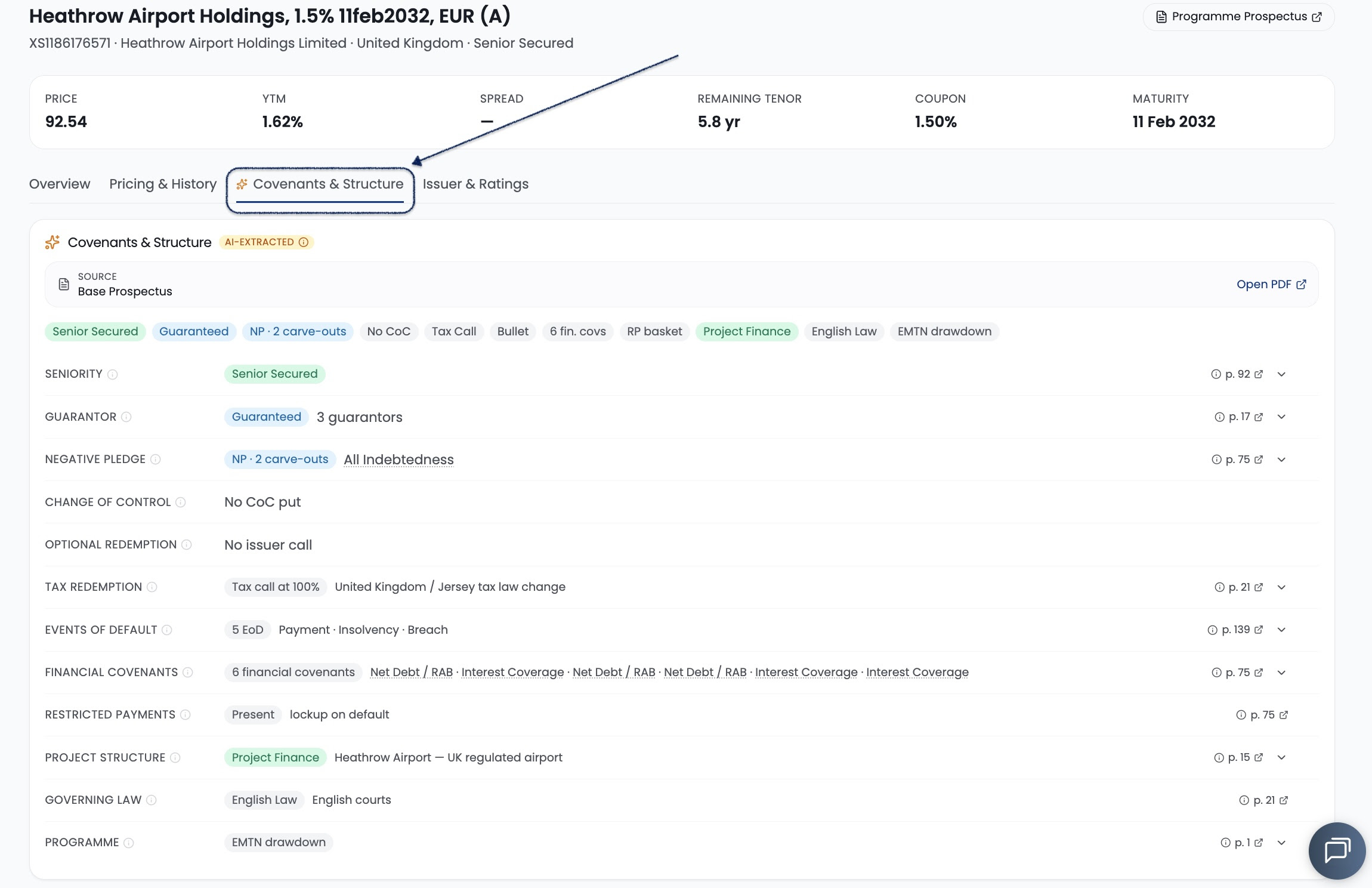

Quicker Bond Classification through covenants

Bond details now include structured covenant data pulled from the source prospectus, with links back to the exact clause and page.

This makes it easier to understand spreads based on specific covenants.

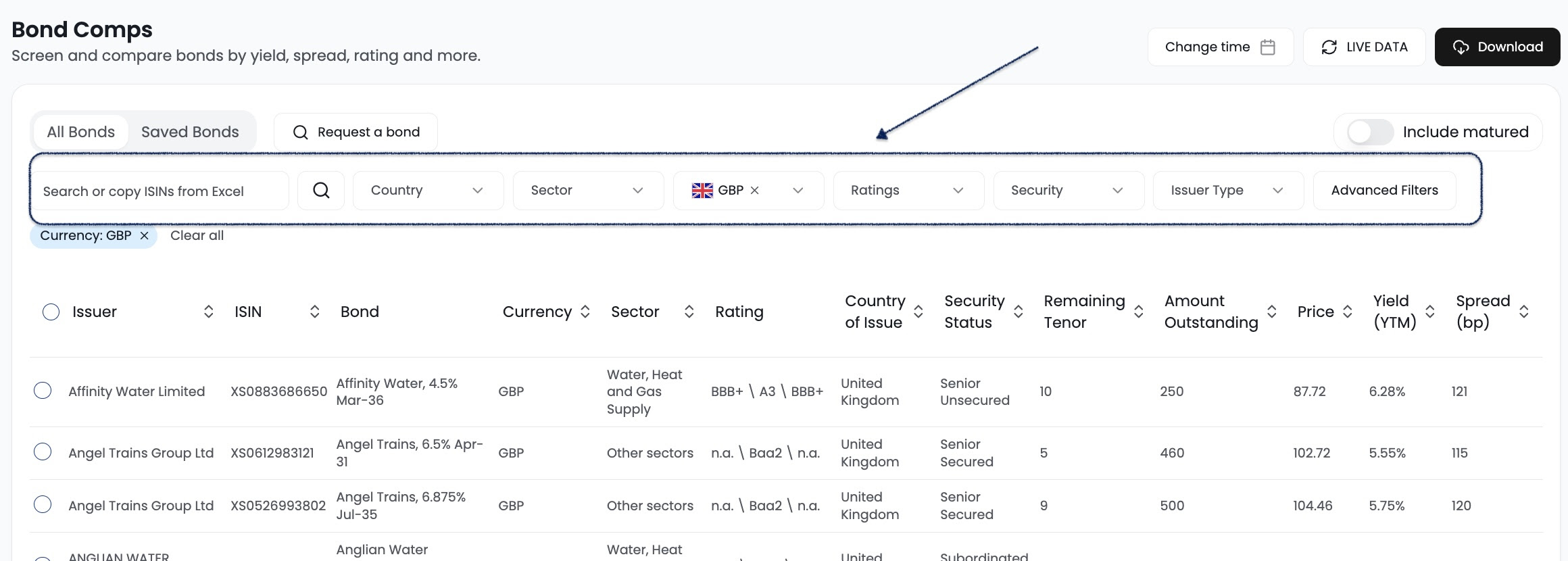

Bond Screener redesigns

The Bond Detail page now surfaces price, YTM, spread, remaining tenor, coupon, and maturity at the top.

The Bond Screener now has a clearer filter row, clickable rows, page-size controls, filter chips, and better loading states - making it easier to find and compare bonds quickly.

New API and MCP capabilities

We’ve added and expanded API and MCP support for FX forward curves, cap/floor pricing, bond lookup by ISIN, swaption pricing, and MCP server discovery.

This makes it easier to connect BlueGamma data directly into your tools, models, and AI workflows.

Improvements

Increased flexibility in swap pricing

The Swap Pricer now handles end-of-month rolling more accurately under ISDA convention.

This helps new month-end swaps line up more closely with bank confirms.

More up to date SONIA fixing rates

SONIA fixings now use a T-1 UK business day delay, instead of T-2.

This gives you more up-to-date fixing data when working with SONIA-linked instruments.

New data

Expanded bond covenant coverage

Underlying prospectus PDFs are now available in BlueGamma, enabling faster research and easier verification.

Increased Economics events coverage

Economic events coverage has been improved for major economies.

When you select a country, BlueGamma now automatically links the matching currency, making it faster to filter events relevant to your workflow.

More visible data freshness

Rates pages now show update cadence, so you can see whether data updates live, daily, weekly, or on a publication schedule.

New features & improvements added in March

If you work with rates, hedging, or market data, a lot of time gets lost in the handoff between finding data, comparing options, and turning analysis into something you can share.

This month, we shipped updates to help with exactly that.

Compare cap vs swap hedging costs in minutes

Now in early preview.

You can price caps across any tenor and strike combination, compare cap vs swap hedging costs, and download a pre-populated presentation to share internally or with clients.

This is especially useful if you are advising on floating-rate debt, refinancing, or real estate hedging decisions and need to explain which structure is cheaper, and why.

For a limited time, we're offering unlimited reports in exchange for feedback while we improve the output.

➜ Try the cap vs swap comparison

Need to present the cap pricing?

Click "Generate Presentation" to download a ready-made slide deck with your pricing already filled in.

That means less time formatting slides and more time explaining the decision.

New Features & Improvements added in March

Use BlueGamma inside OpenBB Workspace

You can now access forward curves, swap rate tables, and historical charts from BlueGamma directly inside OpenBB Workspace.

If OpenBB is already part of your workflow, this gives you a faster way to pull market context without switching tools.

More building blocks for API and Excel workflows

We added several new ways to pull rates and pricing data into your own workflows:

- Forward-starting swap curves via API — docs here

- Inflation swap rates via API — docs here

- Swaption pricing via API — docs here

- Saved swap MtM by ID in the Excel add-in — docs here

- RFR calculations now available in-app

If you use BlueGamma programmatically, these updates make it easier to automate more of your pricing and market data workflow in fewer steps.

Everyday workflows also got smoother

- Curve downloads now include a presentation-ready forward curve chart

- Historical exports now include all loaded value dates

- Swap rate downloads now support multiple currencies and indices in one export

- The Swap Pricer and Swap Mark-to-Market experience is now smoother

- UK government bond curve now supports longer-dated maturities

- You can now set lookback days in Swap Pricer

Broader coverage, with clearer benchmarks

- JPY TIBOR curves are now available

- Ceased benchmark warnings now appear for discontinued rates like LIBOR and TAIBOR, with suggested replacements

- API responses now include timestamps, so you can see data freshness directly

Questions? Get in touch.

New features & improvements added in February

Recently we've been experimenting with LLMs generating slides and reports, and Claude has worked surprisingly well with the BlueGamma MCP.

That said, we're still trying to understand the specific workflows where this is genuinely useful. If you've been experimenting with something similar, get in touch — we'd be interested to exchange notes.

CAPM Calculator

You can now quickly estimate expected returns using our CAPM calculator, making it easier to benchmark equity risk premium directly inside BlueGamma.

New Features & Improvements added in February

Swap MtM Confidence Intervals

You can now view confidence intervals when pricing swaps. This gives you a better sense of how significant your MtM can get, helping you make more informed risk decisions.

LIBOR Swap Pricing Support

You can now price LIBOR swaps directly in Swap Pricer and Swap MtM. Even though LIBOR is discontinued, many legacy instruments still reference it for valuations.

Swap Pricing via API

We're building BlueGamma's API to interact with your AI of choice and run swap pricing and MtMs, so you don't compromise on accuracy.

FRA Data API Endpoint

You can now retrieve FRA data programmatically via API, to help you better understand short-term interest rate expectations.

BlueGamma MCP via Claude or Telegram

BlueGamma MCP is now available through Claude and Telegram, expanding how you can interact with BlueGamma data. If you'd like us to integrate with your AI provider of choice, get in touch.

➜ Book a call to help set it up

Improvements

- Compounding type selection now available for the zero rate endpoint in Excel — makes it easier to retrieve the exact rate convention you need for pricing or valuation models. See Excel Add-In

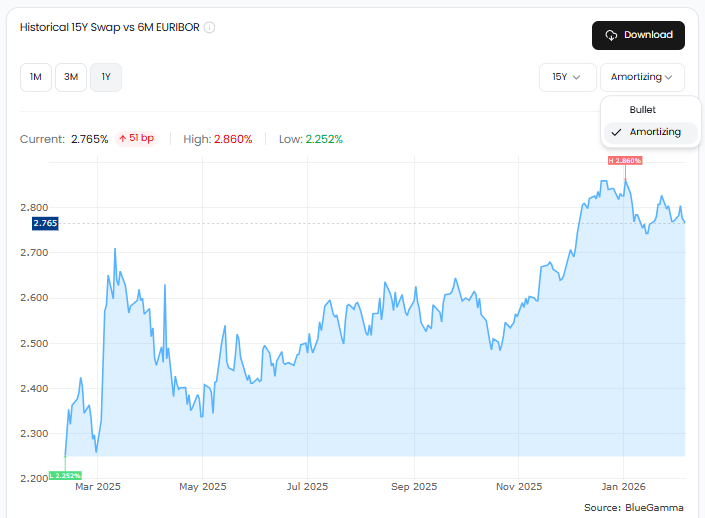

- The EUR dashboard now shows more tenors on the amortising swap historical chart, giving deeper historical visibility when analysing amortising swap markets. See Amortising Swap Tenors

Coming Soon

- Deal-contingent hedge pricing — linked to swaption pricing, this will let you estimate the cost of a DCH for a swap starting in the future, helping you understand the cost of protection.

Questions? Get in touch.

New features & improvements added in January

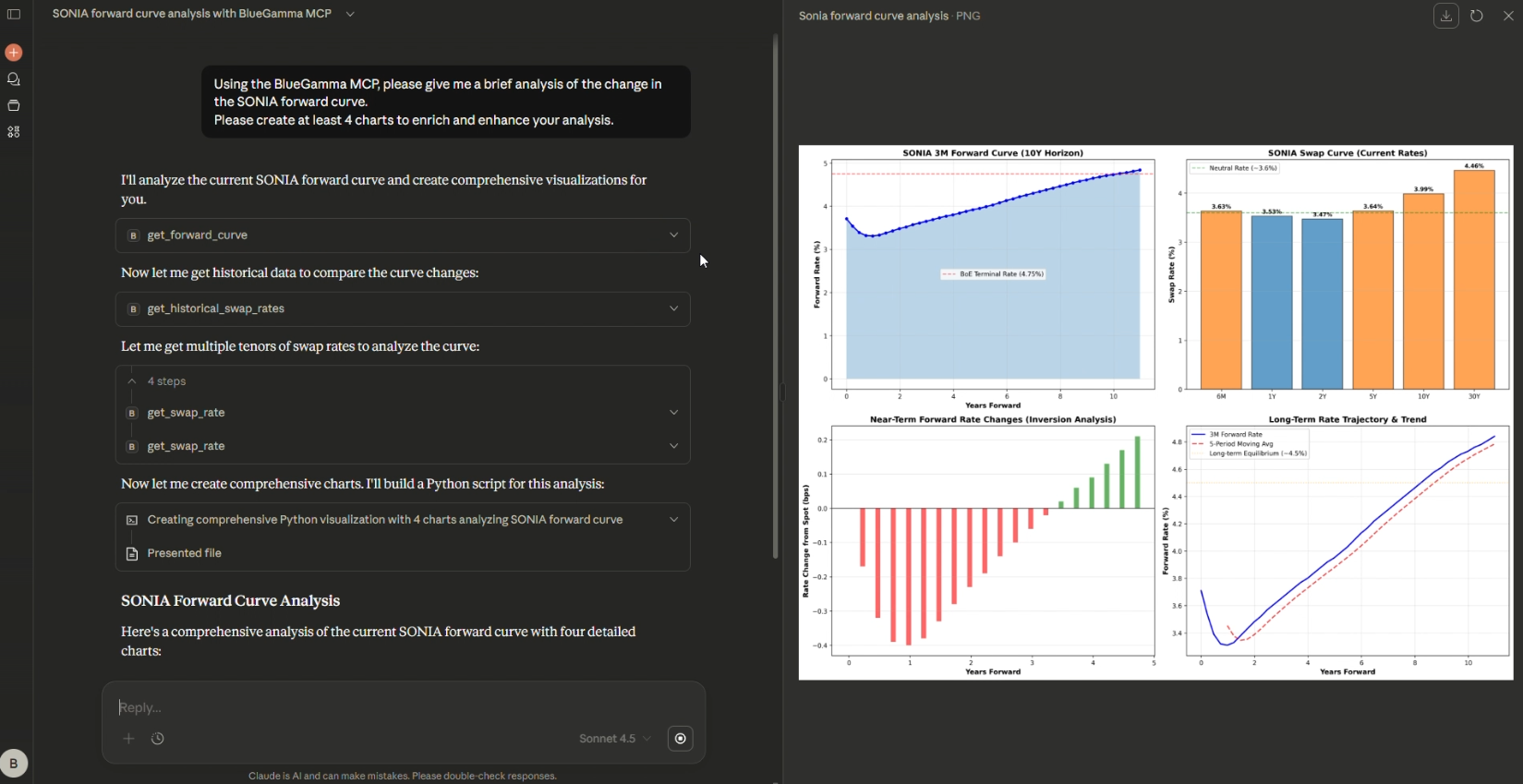

This month, we’ve launched the BlueGamma MCP (Model Context Protocol). This tool bridges the gap between our institutional-grade rates data and your AI’s analytical reasoning, allowing you to connect ChatGPT, Claude Desktop, Gemini directly to the BlueGamma MCP in under 30 seconds.

Supercharge your LLM with the BlueGamma MCP

By connecting your LLM to our real-time data, you gain:

- Visual Market Intelligence: Ask your AI to plot interactive graphs, heatmaps, and trend visualisations directly in the chat window.

- Institutional-Grade Analysis: Generate boardroom-ready market wrap-ups and market analysis grounded in today’s reality. Your LLM doesn't just fetch numbers; it spots opportunities in the curves and pricing data.

- Reduced Hallucinations: Replace "guesses" with verified, API-fetched data for Swaps, FX, Gov Bonds, and Forwards.

➜ Book a call with Ali to try it out

P.S. Already have a BlueGamma API key? See how to Install the MCP now

New Features & Improvements added in January

Beyond the MCP launch, we’ve rolled out several powerful updates to our calculators and API endpoints to help you price and analyse risk more effectively.

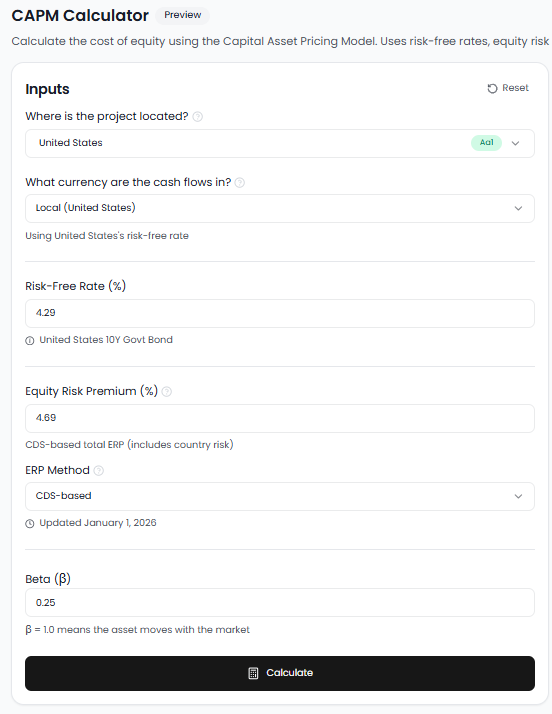

CAPM Calculator

We have launched a Capital Asset Pricing Model calculator on our website and platform for quick, high-level cost-of-equity analysis. The CAPM calculator is still in preview, so please feel free to contact us with any feedback.

MtM Confidence Intervals

You can now view confidence intervals on the Swap Pricer, providing a better view of potential value fluctuations.

Amortising Swap Tenors

We’ve expanded the historical charts for amortising swap rates to include more tenors (found via the EUR Dashboard).

Excel Add-in and Data Updates

- Excel Add-in UI: We’ve refreshed the interface of our Excel Add-in to make it more intuitive for power users managing complex workbooks - let us know if you’d like to try it out.

- Expanded Fixings: We’ve added support for SWESTR fixings, TIBOR rates, and Canada Prime rates to our data universe.

- €STR Integration: You can now add €STR rates and curves directly to your custom dashboards.

New features & improvements added in December

Platform Redesign

We’ve completely updated the platform's look and feel to provide a more modern and slick experience.

This update introduces a sleek dark-themed sidebar for improved navigation, refined graph design and a unified design language that brings the platform’s look and feel directly in line with our website.

Interactive Zoom

You can now zoom in and out on most graphs across the platform, allowing for better granularity when analysing volatile price action or a broader macro view.

➜ Try the new chart functionality

Inline Notional Editing in Swap MtM

Similar to how we've updated the Swap Pricer, you can now edit notionals directly inline within the Swap MtM interface, eliminating the need to export to Excel and edit there.

➜ Try the newly updated Swap MTM Calculator

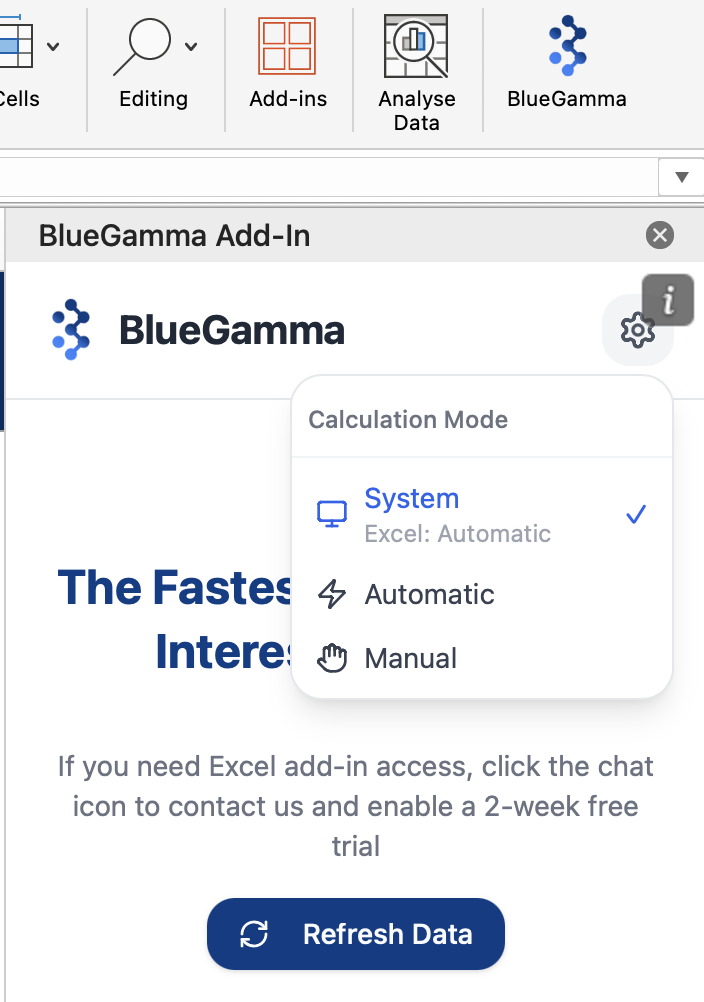

Excel Add-in Calculation Refresh Control

To help users managing larger models, you can now switch between Manual and Automatic calculation modes in our Excel add-in. This gives you full control over when your data refreshes, significantly improving performance for complex workbooks.

➜ Get the BlueGamma Excel Add-In

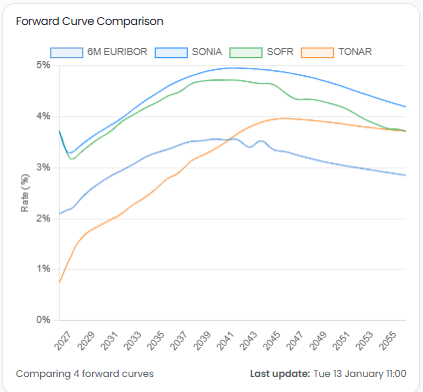

Forward Curve Comparison Widget

A new custom dashboard widget is now available, allowing you to compare forward curves across multiple indices on the same graph for easy correlation tracking and spread analysis.

➜ Add the new “Forward Curve Comparison” widget to your Custom Dashboard

New features & improvements added in November

Zero-coupon rates are now available via API + Excel Add-In

You can now directly retrieve zero-coupon rates through both the API and the Excel Add-In.

This is especially helpful for those using zero-coupon rates for discounting.

➜ Excel Add-In docs for Zero-Coupon Rates

➜ API docs for Zero-Coupon Rates

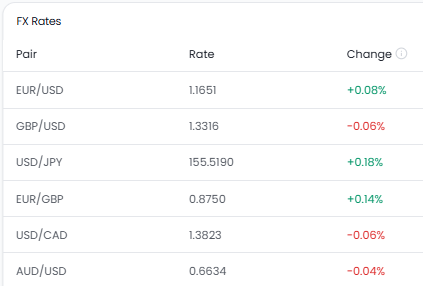

FX Widgets Can Now Be Added to Your Dashboard

FX data can now be added right alongside your rates, curves, and benchmarks in a Custom Dashboard.

➜ Add an FX widget to your Custom Dashboard

Pinned dashboards stay pinned across devices

Pinned dashboards are now saved at the account level so we do a better job of remembering your preferences when you use a new device.

➜ If you have not yet set up a dashboard, here's how to Build your personalised dashboard to show you the charts and tables you look at most often

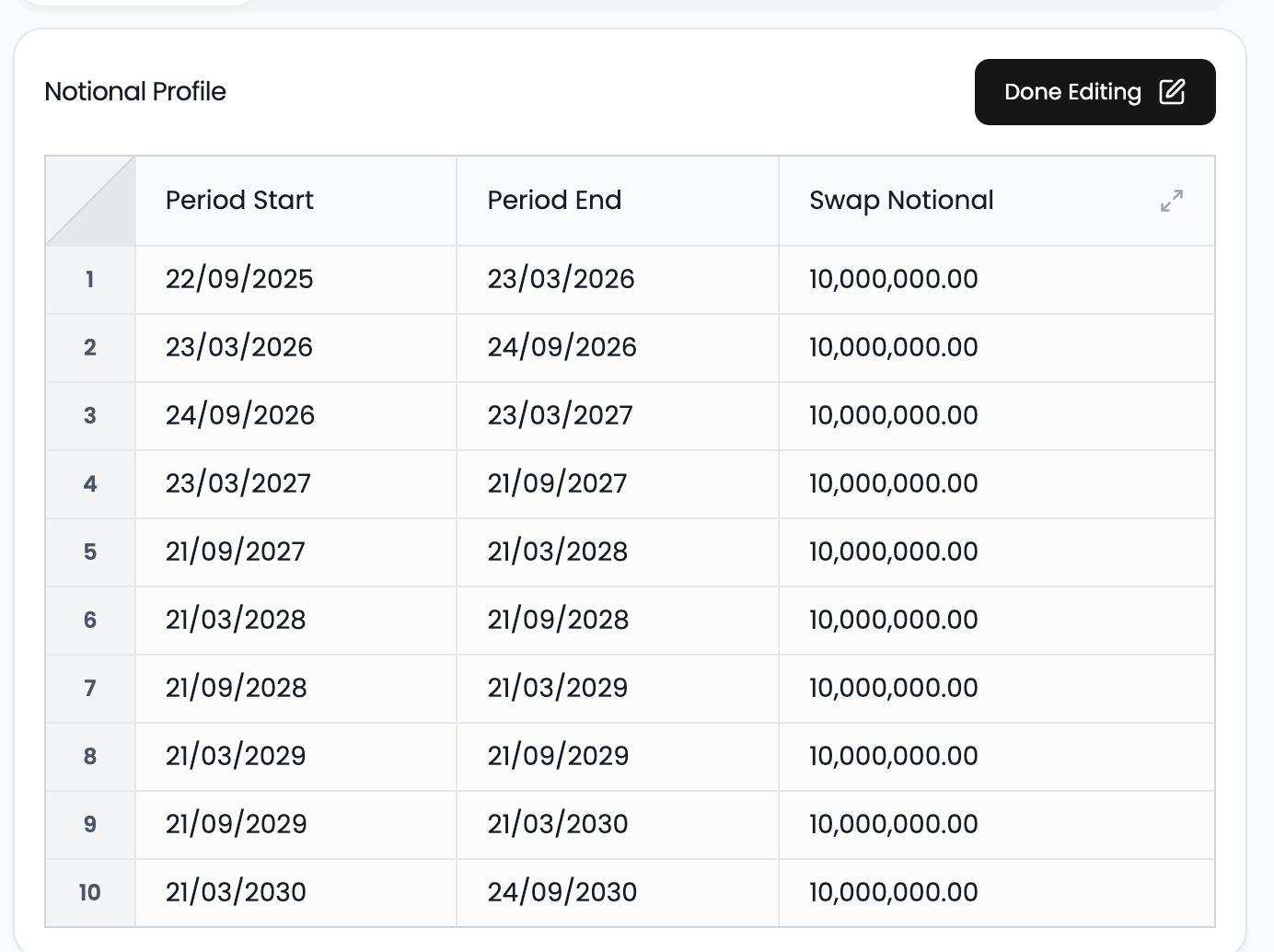

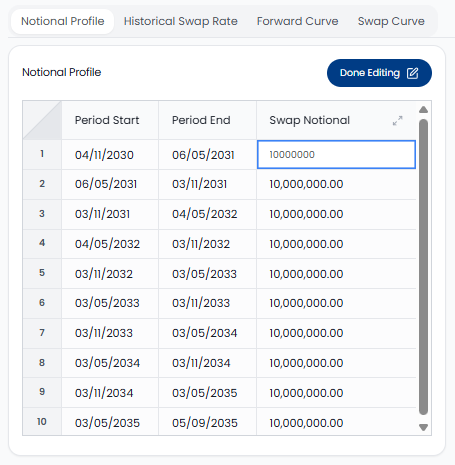

Updating Notionals in your Swap Pricer is now 10x easier

The updated Notional Profile table looks a lot similar to the tool we use most often, Excel. You can now update Notionals directly inside the Swap Pricer, removing the need to download and re-upload files. This works in a similar way to how you'd copy paste into Excel.

New data

Significant increase in FX Forwards Coverage Expanded to 1,506 Currency Pairs

FX Forwards are now available for over 1,500 currency pairs, up from roughly 180 previously. That’s a 737% increase in coverage, unlocking forward pricing for exotic, frontier, and less-traded pairs that were previously difficult to find.

This upgrade makes BlueGamma one of the widest FX Forward datasets available anywhere and dramatically broadens what you can price, model, or backtest.

➜ View our FX forwards with the new expanded universe

12M EURIBOR Curve Now Available

We’ve added the 12M EURIBOR curve to the platform, expanding our EUR curve coverage and giving you access to a key maturity used across swaps, curve analysis, and pricing workflows.

New Daily-Updated Indices Added to the App

More indices are now available in the app and refresh every 24 hours:

HONIA, DESTR, IBR, NOWA, NZONIA, SHIR, ZARONIA, SWESTR, STINA, THOR, TIIEON, 1M BBSW, 1M BBSY, 3M PRIBOR, 6M HIBOR, 3M BUBOR, 1M BKBM, 3M WIBOR, 6M STIBOR, POLONIA, CITA

➜ Check out our catalogue of Benchmark Rates

More Historical €STR Data on Graphs

Charts now include deeper historical €STR data, ideal for back-testing and longer-term analysis.

➜ Check out our €STR Swaps data

New Government Bond Coverage: Romania

Romanian government bonds have been added, expanding fixed-income coverage even further.

Cleaner, Easier-to-Navigate App Layout

We have redesigned key areas of the platform to create a structured experience, making the process of finding the data you need simpler and faster.

- The navigation bar is more intuitive, helping you to find what you need quickly.

- The swap rates and interest rate curve pages now feature a cleaner layout with better spacing and visual hierarchy.

- Graphs now show High, Low and Change since the Start of Period.

➜ Check out our new and improved dashboard layout

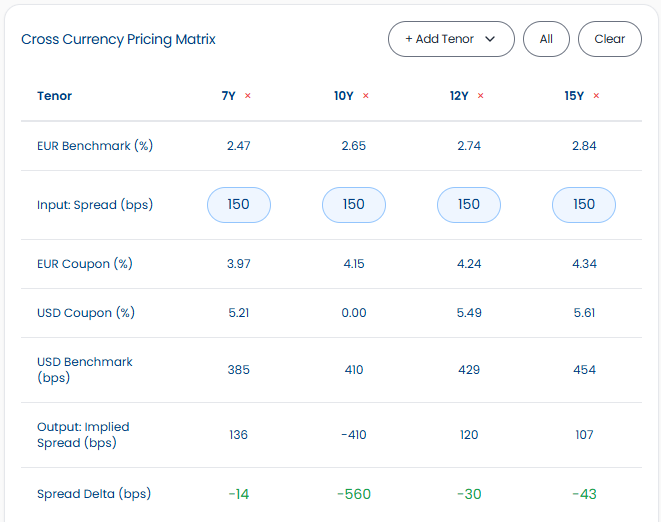

Download the Cross-Currency Pricing Table

To help save you from copy-pasting, you can now instantly download the entire Cross-Currency (XCCY) Pricing Matrix directly from the platform into a convenient CSV format.

➜ Try our Cross-Currency Pricing Matrix

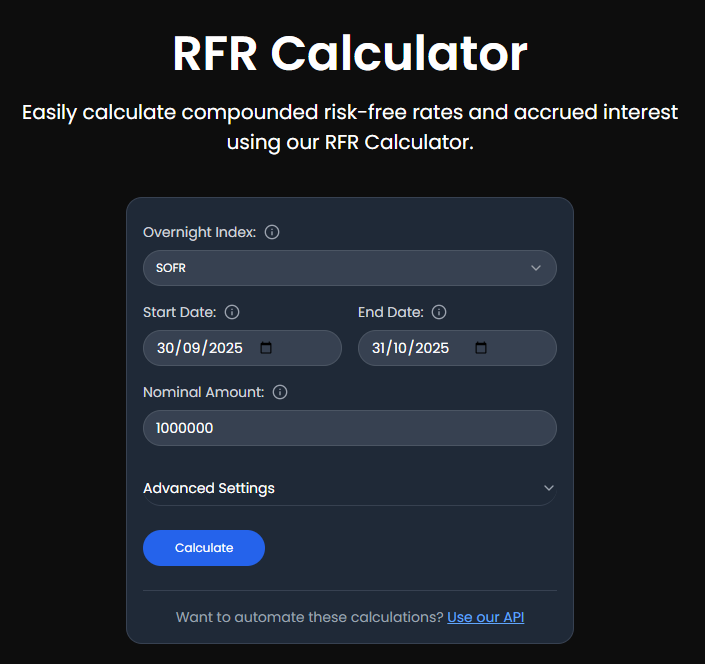

New RFR Calculator

We’ve launched a powerful and user-friendly Risk-Free Rate (RFR) calculator, which simplifies the process of performing compounded rate calculations for loan pricing and derivatives valuation.

Instead of manually compounding daily rates for a specific period—a process that is often time-consuming and prone to error—our tool provides instant and accurate results.

➜ Try our new Risk-Free Rate (RFR) calculator

Swap Curve Chart in the Swap Pricer tool

To provide greater market context while pricing trades, you can now see the relevant swap rates within the Swap Pricer page, so if you have a discrepancy between the in-app rate and the quoted rate, you can compare input rates easily.

➜ Give the Swap Pricer a spin to see the new Swap Curve chart

API Docs Upgrade

Our Interest Rate API documentation has been refreshed and is now hosted at www.bluegamma.io/interest-rate-api. With this upgrade, the BlueGamma API becomes easier to integrate, getting closer to our goal of a "plug and play" API.

New Data

We are continuously committed to expanding our global data coverage so that you have all the critical market information you need, consolidated conveniently in one place.

Here’s what we’ve added this month:

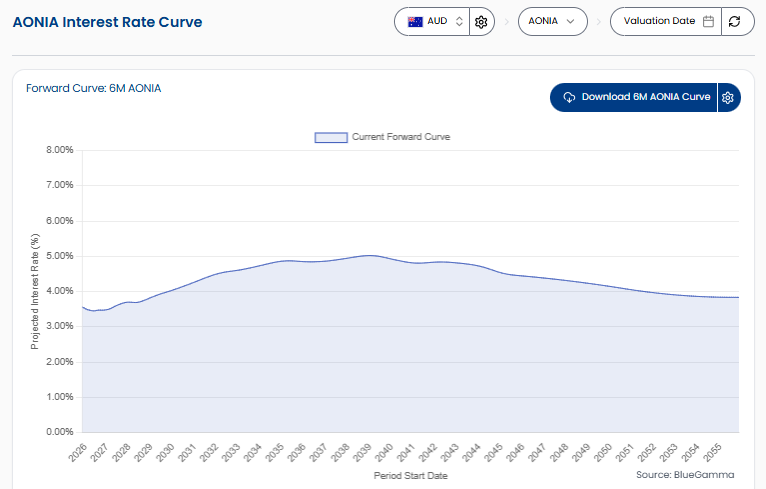

- AONIA (Australia Overnight Index Average)

- DESTR (Danish Short-Term Rate)

- RBNZ OCR (Reserve Bank of New Zealand Official Cash Rate)

All three are now live and available on the platform.

➜ See these new datapoints in the platform

Historical Forwards Now Available (Excel Add-In + API)

You can now fetch historical forward rates directly through both the Excel Add-In and API. Previously, historical requests would return errors - now, you’ll get accurate data for past periods instantly.

➜ Try the Excel Add-In and API.

New features & improvements added in September

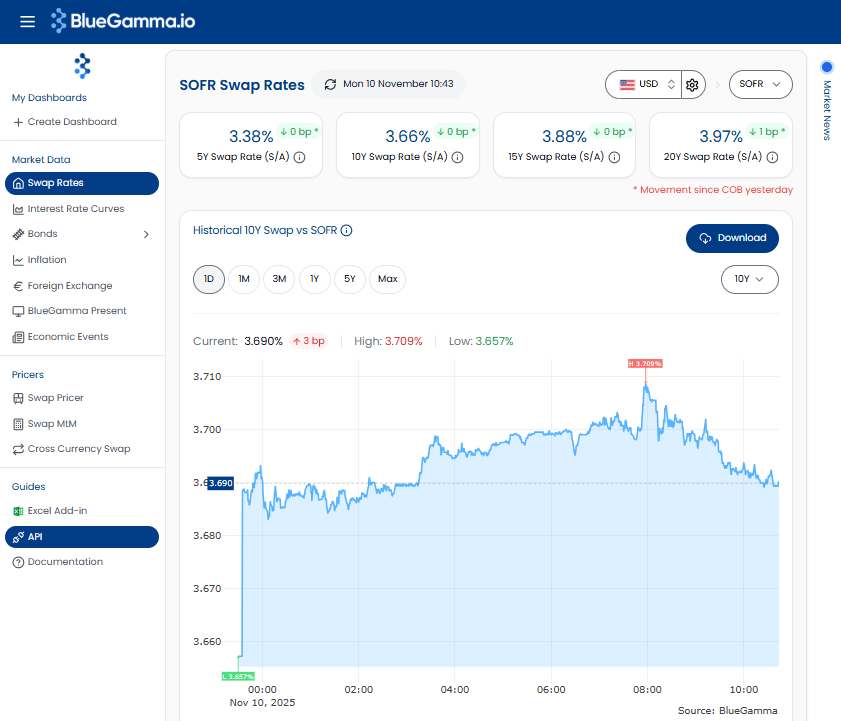

Web app: Underlying interest rate data in now updated every 30 seconds

Swaps now refresh every 30 seconds, giving you near real-time visibility so you can react faster to market movements and stay in sync with changing conditions.

➜ Have a look at the latest Swap Rates Here

API: Forward curve data now includes a ‘timestamp’ 🕒

To improve transparency and auditability, the API now returns the exact timestamp showing when forward curve data was created. You’ll always know how current your data is, giving you a clearer context for every calculation. If you'd like a link to the tutorial on getting this - do let us know.

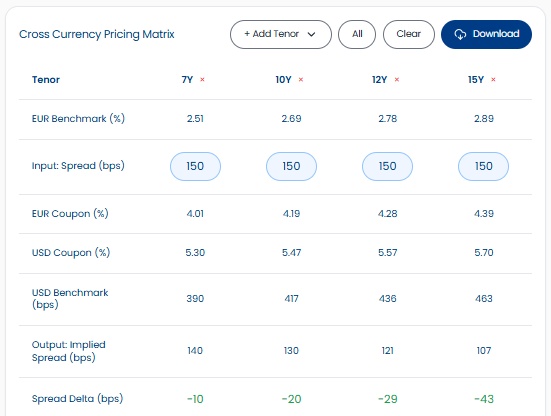

Price multiple cross-currency swap maturities simultaneously

Price several cross-currency swap maturities at once instead of running them one by one, saving time and streamlining your workflow. You'll soon be able to download this table as well.

➜ Try our Cross-Currency Pricing Matrix

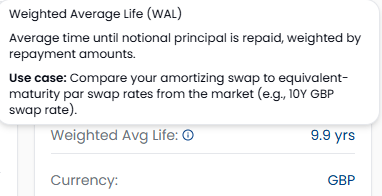

See Weighted Average Life (WAL) in the Swap Pricer feature

One of the best sense checks when pricing a swap, look at the WAL and compare it to the swap rate with the same maturity. WAL calculation is now automatic and updates with the notional profile and soon you'll be able to compare this to a market swap rate side-by-side.

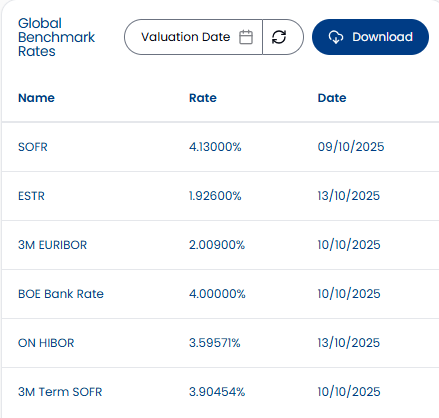

You can now download data from the Global Benchmark Rates Widget in your Custom Dashboard

The Global Benchmark Rates Widget now includes download functionality, so you can easily pull and analyse benchmark data offline or integrate it into your models.

➜ Try building a Custom Dashboard

New data

We’ve expanded coverage across FX and Inflation markets:

FX:

- Mauritius: Mauritian Rupee (MUR)

- Burkina Faso: West African CFA franc (XOF)

- Tunisia: Tunisian Dinar (TND)

- Morocco: Moroccan Dirham (MAD)

Inflation:

- Mauritius

- Seychelles

- Burkina Faso

- Chad

- Tunisia

- Morocco

Plus, two new datapoints are now live:

- "91-day Certificate of Deposit

- "Mumbai Interbank Offered Rate"

If you only try one thing today, I'd recommend setting up a custom dashboard with the specific graphs and tables you like to see.

➜ Here's a link to our custom dashboard page, click "New Dashboard", then "+" sign to add a widget