By Ahmed Babikir and Ali Vohra. Originally published August 31, 2023. Updated 9 April 2026 with live SOFR swap curve data and a worked example.

What are interest rate swaps, and how do they work?

Interest rate swaps are contracts in which two counterparties agree to swap periodic interest payments, usually for a fixed time period. Also known as vanilla swaps, these represent the most basic and commonly-traded variety of interest rate swaps. Organisations utilise them to hedge against rate changes, speculate on future movements, or accomplish both objectives simultaneously.

The mechanism involves exchanging floating rates for fixed rates, or vice versa, to take advantage of differentials in interest rates. Companies pursue swaps when seeking to convert variable-rate debt to a fixed rate or secure a lower interest rate. No principal is exchanged - only the net difference in interest payments changes hands on each payment date.

Interest rate swaps are the largest segment of the global derivatives market. They are used by corporations, banks, institutional investors, and governments to manage interest rate exposure, reduce borrowing costs, and align asset and liability profiles.

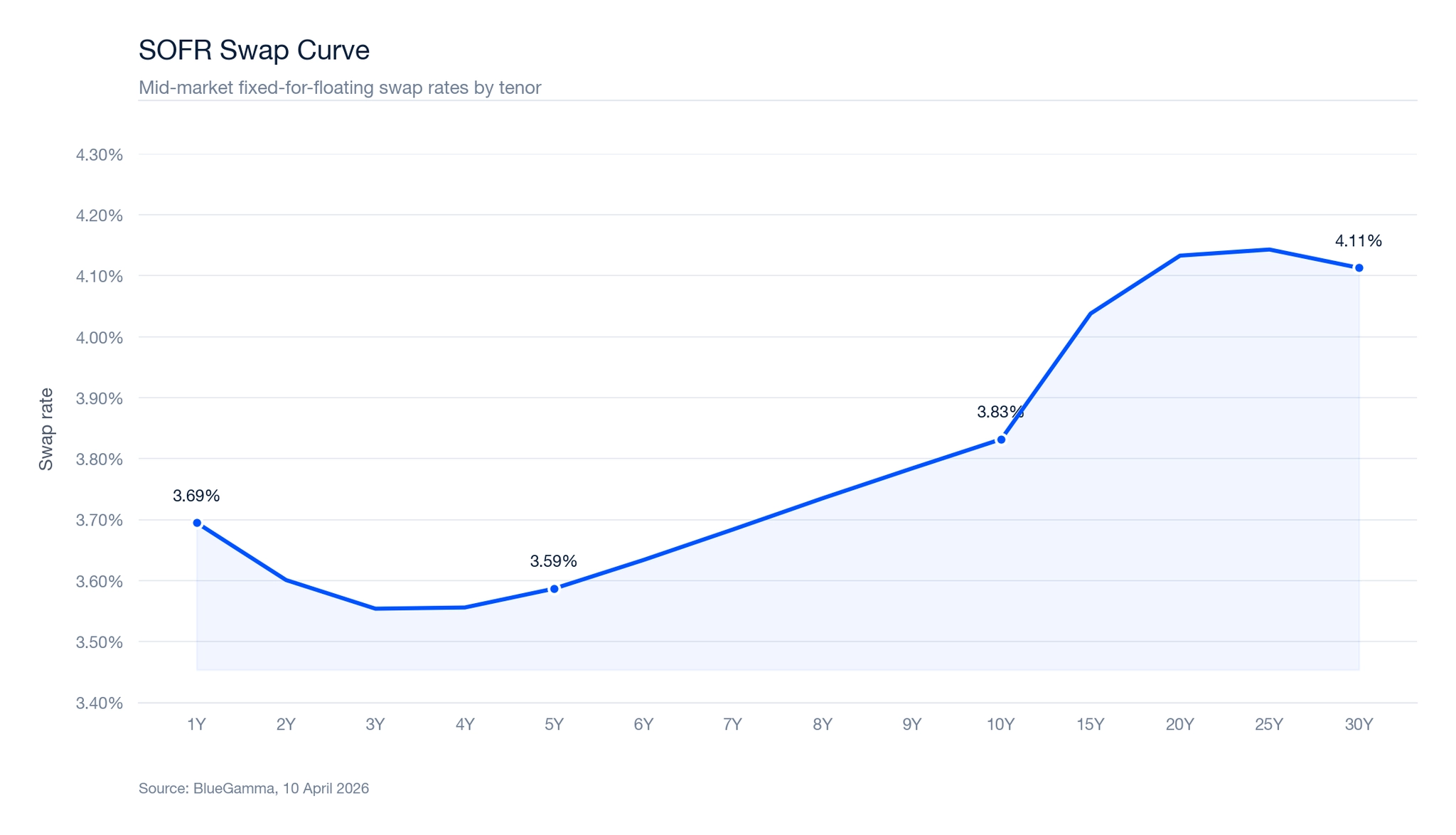

The SOFR Swap Curve (Live Market Data)

The swap curve shows the fixed rate that the market is willing to exchange for the floating rate at each tenor. It is one of the most important reference points in fixed-income markets, and the numbers below are what banks, corporates, and investors see on their screens today.

| Tenor | 1Y | 2Y | 3Y | 5Y | 7Y | 10Y | 15Y | 20Y | 30Y |

|---|---|---|---|---|---|---|---|---|---|

| SOFR Swap Rate | 3.70% | 3.60% | 3.55% | 3.59% | 3.68% | 3.83% | 4.04% | 4.13% | 4.11% |

Source: BlueGamma. Mid-market rates, annual fixed vs SOFR floating.

The current 5-year SOFR swap rate is 3.59%, while SOFR swap rates across the curve range from 3.55% at three years to 4.13% at 20 years. The current SOFR swap curve shows a slight dip in the 3-year tenor (3.55%) before rising steadily through the long end. This upward-sloping shape indicates the market is pricing in gradually higher rates over the medium to long term.

What are the types of interest rate swaps?

Fixed-to-Floating

In this structure, one party makes payments based on a fixed interest rate (typically the borrower), while the counterparty pays based on a floating rate (typically the hedge counterparty). In the US, floating rates typically reference SOFR (the Secured Overnight Financing Rate), which replaced USD LIBOR as the benchmark. In the UK, SONIA plays the same role. Companies employ this swap type when they want to exchange the risk of rising interest rates for the certainty of a fixed rate.

Example: RCG, a company with floating-rate borrowing, expects rate increases and enters a fixed-to-floating swap, exchanging floating payments for fixed ones. If rates rise as anticipated, RCG benefits by paying the contractual fixed rate rather than higher floating rates.

Floating-to-Fixed

This structure reverses the fixed-to-floating arrangement. One party pays floating rates while the other pays fixed rates. Companies unable to issue floating-rate bonds often use these swaps to replicate that structure.

Example: ABC, a company issuing fixed-rate bonds, can enter a floating-to-fixed swap with a commercial or investment bank, where it pays the floating rate and receives fixed-rate payments, synthetically converting its fixed-rate liability into a floating-rate one.

Float-to-Float

In this arrangement, companies exchange periodic payments on two different floating rates, commonly called basis swaps. The most common form of this swap is the 6-month EURIBOR for 1 or 3-month EURIBOR, which changes the interest payments from every six months to either one or three months. In USD markets, basis swaps between Term SOFR and overnight SOFR, or SOFR and the Fed Funds rate, are actively traded.

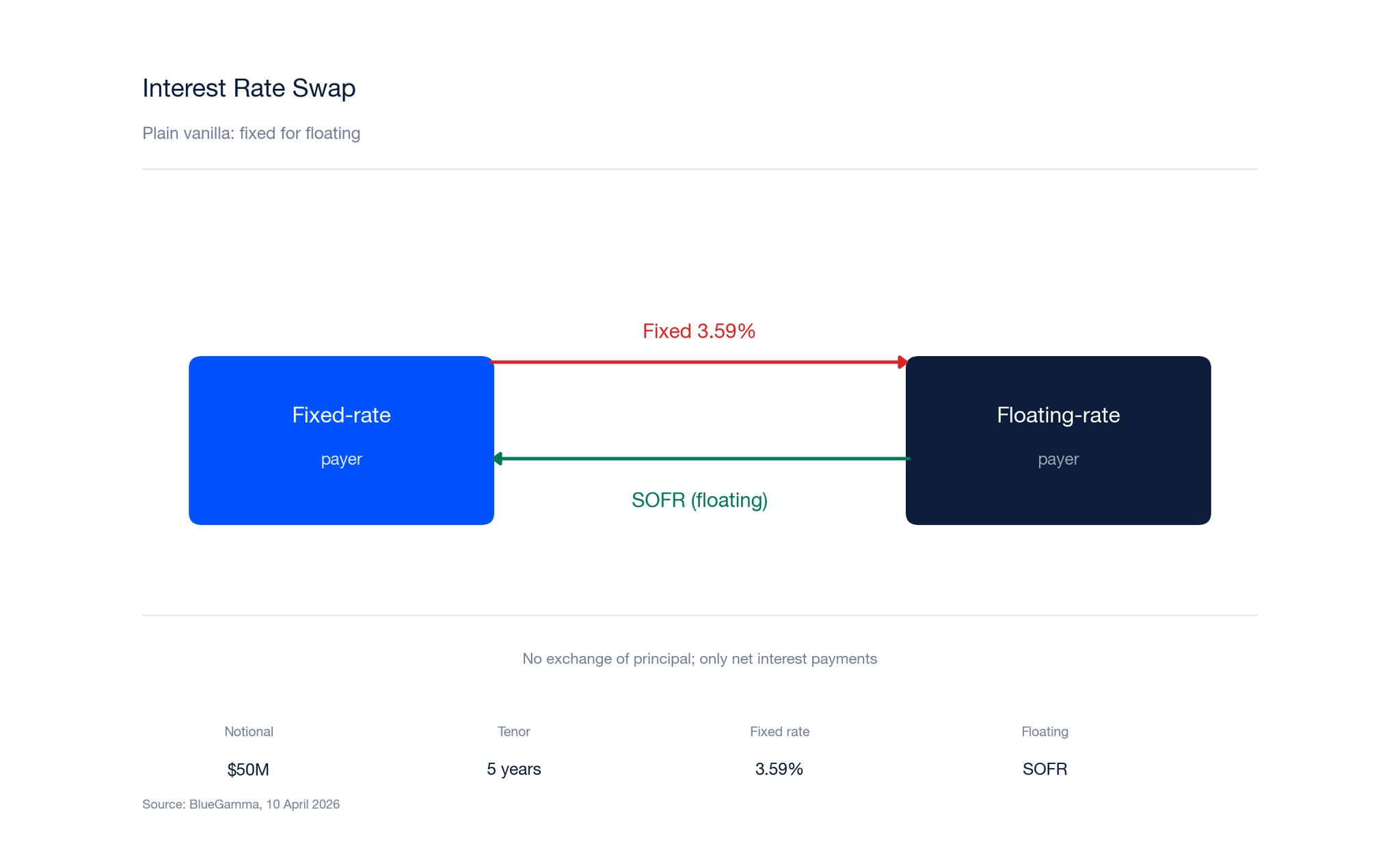

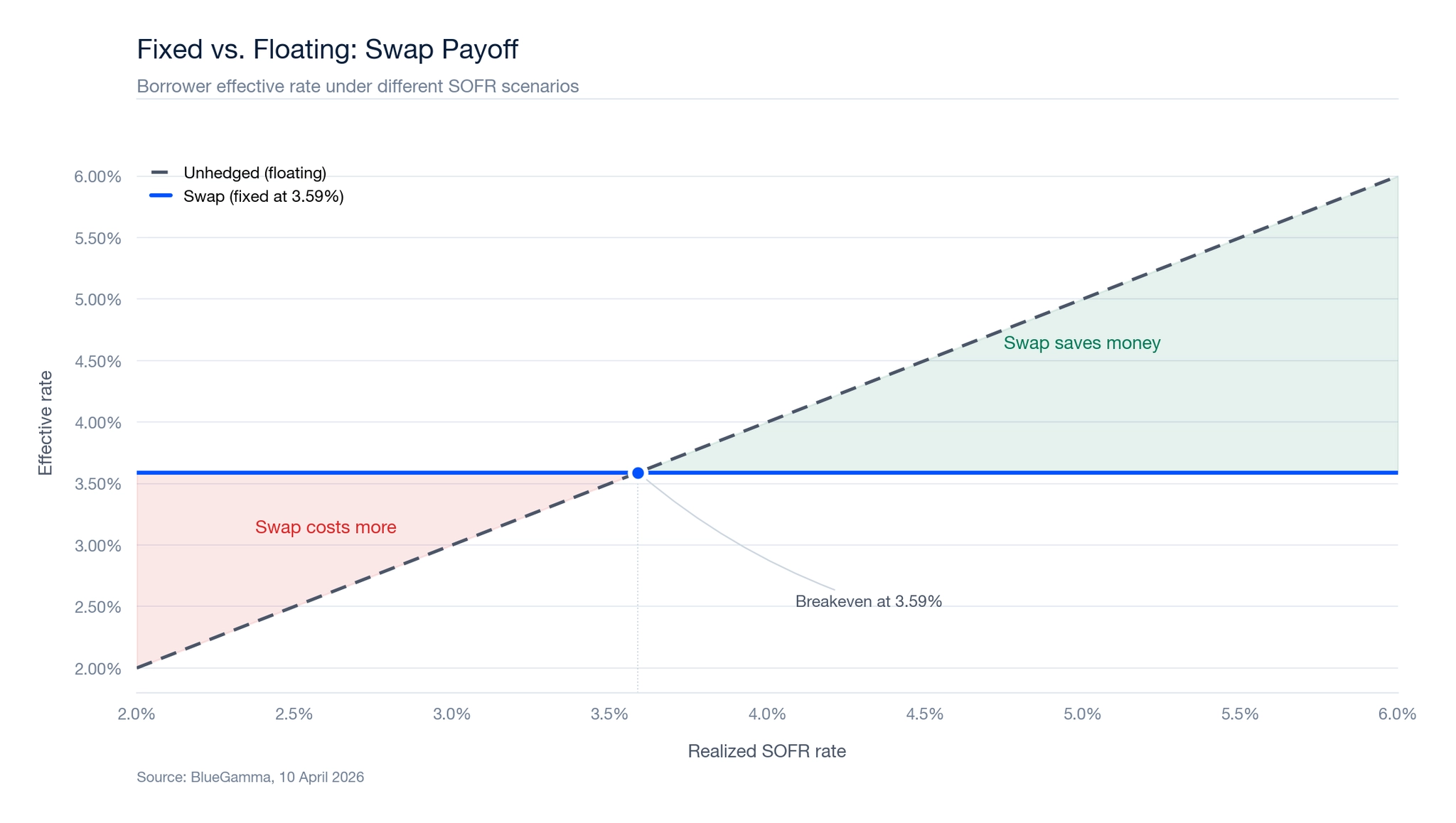

A Worked Example: $50M Floating-Rate Loan Hedged with a Swap

Consider a corporate borrower with a $50 million, 5-year floating-rate term loan at SOFR + 200 basis points. The borrower is concerned that rising rates will increase its debt service costs and wants to lock in a fixed rate.

Using the live 5-year SOFR swap rate of 3.59%, the borrower enters into the following swap:

| Parameter | Value |

|---|---|

| Notional | $50,000,000 |

| Borrower pays (fixed) | 3.59% |

| Borrower receives (floating) | SOFR |

| Tenor | 5 years |

| Payment frequency | Annual (fixed), Annual (floating) |

The borrower's effective cost:

- Loan: pays SOFR + 200 bps to lender

- Swap: pays 3.59% fixed, receives SOFR

- SOFR cancels out

- Net: 3.59% + 2.00% = 5.59% all-in fixed

The borrower has converted a floating-rate exposure into a fixed 5.59% obligation for five years, regardless of where SOFR moves.

If SOFR averages above 3.59% over the life of the swap, the borrower benefits from having locked in. If SOFR averages below 3.59%, the borrower has paid more than it would have under the floating rate. The swap eliminates uncertainty in either direction.

What are the benefits of interest rate swaps?

Risk Management

To manage the floating interest rate risk brought about by borrowing money from banks, public markets or debt funds, companies enter into interest rate swaps. They stabilise borrowing costs for a specified period. Financial institutions managing loans, bonds, and assets leverage swaps to reduce exposure to rate fluctuations, benefiting both borrowers and counterparties.

Flexibility

Fixed-rate loan holders face locked rates for the loan duration, but swaps offer customisation. For example, a company might want to swap from a fixed interest rate to a floating one after two years, allowing it to take advantage of lower rates without refinancing costs.

Adjusting Interest Rate Exposure

Interest rate swaps can help companies adjust their exposure to interest rates and manage their volatility. Organisations can speculate on future rate directions to maximise profits or reduce debt costs during anticipated rate increases.

How can you use interest rate swaps?

Trading

Trading involves trying to predict the future direction of interest rates and entering a swap accordingly for economic gain. Some investors buy swaps, then sell them before maturity for profit - though this strategy carries significant risks with potentially unlimited downside.

Hedging

Hedging is the act of limiting risks through investment. Swaps protect against rising or falling rate risks, offsetting value changes when properly structured. This is by far the most common use of swaps among corporate borrowers, banks, and institutional investors.

Pre-Hedging

Organisations planning future bond issuances or swap agreements can use swaps to protect against rising rates beforehand. This can give certainty about future interest rates early on. However, these companies would need to understand the associated risks, including the mark-to-market volatility of the pre-hedge position.

How Interest Rate Swaps Are Priced

The fixed rate in a swap is set so that the present value of all fixed payments equals the present value of all expected floating payments at inception. This means the swap has zero value to both parties at the start.

The pricing relies on:

The forward curve

Expected future floating rates are derived from the current yield curve. Each floating payment is estimated using the forward rate for that period.

Discount factors

All future cash flows (both fixed and floating) are discounted to present value using the appropriate discount curve, typically the overnight rate curve (e.g. SOFR OIS for USD swaps).

The par swap rate

The fixed rate that equates the present value of both legs is the par swap rate. This is the rate quoted in the swap market and shown on the swap curve above.

For a 5-year SOFR swap, the current par rate of 3.59% means that 3.59% fixed annual payments have the same present value as the expected SOFR floating payments over the next five years.

Valuing an Existing Swap

Once a swap is in force, its market value changes as interest rates move. The mark-to-market value of a swap at any point is the difference between the present value of remaining fixed payments and the present value of remaining floating payments.

If rates have risen since inception, the fixed-rate payer holds a positive-value swap: they are paying below-market fixed rates and receiving higher floating rates. The floating-rate payer holds an equivalent negative-value position. If rates have fallen, the reverse applies.

The mark-to-market value matters for collateral requirements under CSA agreements, early termination payments, hedge accounting effectiveness testing, and financial statement reporting.

What are the risks of interest rate swaps?

Counterparty Risk

When entering swap agreements, the other party might default on its payment obligations. The guidance is to transact only with reputable financial institutions. Central clearing through clearinghouses (mandatory for standardised swaps under most jurisdictions) and bilateral collateral agreements mitigate this risk.

Mark to Market Risk

Interest rate swaps trade in the market, so the value of the trade can change all the time. Unfavourable rate movements reduce swap values. Organisations can manage this through collateral agreements where parties post security if values shift.

Basis Risk

If the floating rate on the swap does not perfectly match the floating rate on the underlying exposure (e.g. the loan references Term SOFR while the swap references overnight SOFR), a residual mismatch may exist. For most corporate hedges this is small, but it should be understood before executing.

How Do Banks Make Money on Interest Rate Swaps?

Banks generate revenue from interest rate swaps primarily through the bid-offer spread. When a bank executes a swap with a borrower, the fixed rate charged to the client is slightly above the mid-market rate, while the rate at which the bank offsets its risk in the interbank market is at or near mid-market. This difference, typically 2 to 10 basis points, represents the bank's transaction margin. In back-to-back swap structures, the bank earns this intermediation spread with no residual interest rate risk, as the client-facing swap and the offsetting market swap cancel each other out. Banks may also earn additional fees for structuring, amending, or restructuring swap positions.

Why are interest rate swaps beneficial for hedging?

Interest rate swaps can protect you from the risk of rising or falling interest rates. They serve as valuable tools for hedging against rate risk on loans, bonds, or other assets. Swaps can be a valuable tool for hedging, trading, and pre-hedging when risks are properly managed.

With the current 5-year SOFR swap rate at 3.59%, a borrower with a floating-rate loan at SOFR + 200 bps can lock in an all-in fixed cost of 5.59% for five years. The swap curve ranges from 3.55% at the 3-year point to 4.13% at 20 years, reflecting market expectations for gradually higher rates over the longer term.

This article is for informational and educational purposes only and does not constitute financial, investment, legal, or tax advice. BlueGamma does not provide advisory services. Readers should consult qualified professional advisors before entering into any derivative transaction. Market data shown is indicative and sourced from BlueGamma as of the date stated.

Frequently Asked Questions

How do interest rate swaps work?

In an interest rate swap, two parties agree to exchange interest payment streams on a specified notional amount for a defined period. One party pays a fixed rate while the other pays a floating rate tied to a benchmark such as SOFR. At each payment date, only the net difference between the two rates is exchanged. The notional amount (the reference principal on which payments are calculated) is never transferred between the parties.

How are interest rate swaps priced?

The fixed rate in a swap is determined so that the present value of all fixed payments equals the present value of all expected floating payments at inception, giving the swap a net value of zero at the start. Pricing relies on the forward rate curve (which estimates future floating-rate fixings) and discount factors derived from the overnight rate curve. The resulting par swap rate is the fixed rate quoted in the market for each tenor.

What is a notional amount?

The notional amount is the reference principal used to calculate interest payments in a swap. It is not exchanged between the parties. For example, on a $50 million notional swap at 3.59% fixed, the annual fixed payment is $50 million multiplied by 3.59%. Swap rates quoted in the market apply to this notional amount to determine actual cash flows.

What is the SOFR swap rate?

The SOFR swap rate is the fixed rate exchanged for SOFR floating payments in a standard interest rate swap. It varies by tenor and reflects market expectations for future SOFR levels. Say the 5-year SOFR swap rate is 3.59%, the 10-year rate is 3.83%, and the 30-year rate is 4.11%. These rates are published in real time and serve as key benchmarks for loan pricing and hedging decisions.

Can you lose money on an interest rate swap?

A swap can result in a financial loss relative to what the borrower would have paid without the hedge. If a borrower enters a swap to pay 3.59% fixed and SOFR subsequently averages 2.50% over the life of the swap, the borrower pays more than they would have under the floating rate. The swap's mark-to-market value can also become negative, meaning the borrower would owe a termination payment if they needed to exit the position early.