An interest rate collar is a hedging structure that combines a purchased cap and a sold floor to create a bounded range for your effective floating rate. The cap sets a ceiling on how high your rate can go; the floor sets a minimum rate you will pay. The premium received from selling the floor offsets some or all of the premium paid for the cap, making the overall structure cheaper than a standalone cap, or in some cases free (a zero-cost collar).

This guide covers how collars work, how they are priced in today's market, and when they make sense for floating-rate borrowers.

How an Interest Rate Collar Works

A collar is simply the combination of two option positions:

- Buy a cap at a strike rate above the current reference rate - this protects against rising rates

- Sell a floor at a strike rate below the current reference rate - this gives up benefit from falling rates

The borrower pays a premium for the cap and receives a premium for the floor. The net cost is the difference.

When the floating reference rate moves within the corridor between the floor and cap strikes, neither option is exercised and the borrower pays the prevailing floating rate. When the reference rate rises above the cap strike, the cap pays out and the borrower's effective rate is capped. When the reference rate falls below the floor strike, the borrower owes the difference to the floor counterparty, and the effective rate floors at the floor strike.

As the chart shows, the collar produces a flat effective rate outside the corridor (at the floor on the downside, at the cap on the upside) and tracks the floating rate within the corridor. Compared to a pure cap, the borrower gives up the potential savings from rates dropping significantly.

Collar Pricing: A Live Example

Let's look at concrete numbers. Consider a borrower with a $50 million, 3-year floating-rate loan at SOFR + 250 bps, looking to hedge with a collar at a 4.00% cap and 3.00% floor:

| Component | Strike | Premium | Direction |

|---|---|---|---|

| SOFR cap | 4.00% | $259,455 (52 bps) | Borrower pays |

| SOFR floor | 3.00% | $424,377 (85 bps) | Borrower receives |

| Net | $164,922 received | Net receipt |

Source: BlueGamma, 10 April 2026. $50M notional, 3Y tenor, quarterly resets, SABR-calibrated volatility.

In the current market, a 4.00% cap / 3.00% floor collar actually produces a net receipt for the borrower. That reflects two features of the current environment: the 3Y SOFR forward curve sits around 3.51%, meaning the floor at 3.00% is closer to being in-the-money than the cap at 4.00%, and the negative skew in the SOFR volatility surface makes floors more expensive than caps at equivalent distances from the forward rate.

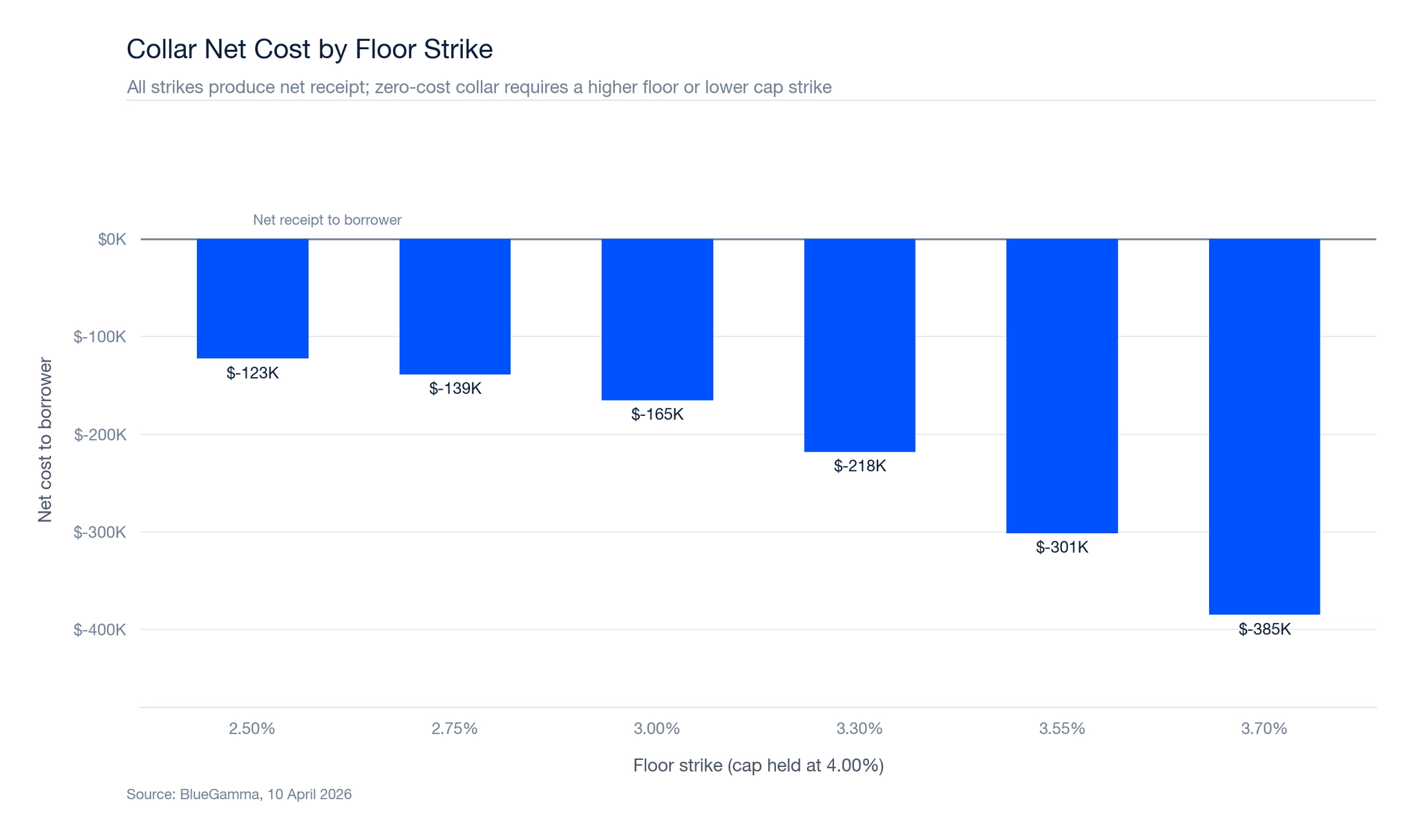

The Zero-Cost Collar

The most popular collar structure is the zero-cost collar, where the cap premium paid exactly equals the floor premium received. No cash changes hands at inception.

Building a true zero-cost collar means solving for the floor strike that produces an equal premium to the chosen cap strike (or vice versa). In today's market, with forwards around 3.51% and the cap at 4.00% costing $259,455, a zero-cost collar would require a much lower floor strike than you might expect.

Even at a floor strike of 2.50%, the floor premium ($381,974) still exceeds the 4.00% cap premium ($259,455). In the current environment, a zero-cost collar at a 4.00% cap strike requires either an even lower floor strike, or alternatively a higher cap strike that aligns the two premiums.

This is worth knowing before you request a quote. Dealers will typically calibrate the collar to your budget: tell them you want zero cost, and they will find the strike combination that delivers it. In current conditions, that often means a cap strike higher than the borrower initially expects (e.g. 5.00%) paired with a floor near the current forward rate.

Collar vs Cap vs Swap

| Feature | Swap | Cap | Collar |

|---|---|---|---|

| Upfront cost | None (rate embedded) | Cap premium (~52 bps) | Lower or zero |

| Rate certainty | Fully fixed at 3.57% | Ceiling at cap strike | Bounded range (floor - cap) |

| Benefit from falling rates | None | Full benefit | Only down to floor strike |

| Mark-to-market risk | Can be positive or negative | Always positive or zero | Can be positive or negative |

| Early termination | Requires breakage payment | Can let expire | Requires unwinding both legs |

| Best for | Full budget certainty | Short-term, lender-required | Reducing cap premium cost |

The collar sits between the cap and the swap. You give up some benefit from falling rates (everything below the floor), and in exchange you get cheaper protection than a standalone cap. Compared to a swap, you retain some benefit from rates declining (down to the floor), but you have mark-to-market exposure on the floor leg if rates fall significantly.

When to Use a Collar

The cap premium is too expensive

This is the main reason borrowers choose collars. If a lender requires a floating-rate hedge and the standalone cap premium is out of budget, a collar reduces the upfront cost. The trade-off is accepting a minimum rate.

You have a floor on your borrowing cost anyway

If the underlying loan already has a contractual floor (for example, SOFR can't go below 0% for many commercial loans, or a lender-specified SOFR floor), selling a floor at a level at or below that contractual floor costs you nothing in economic terms. The contractual floor was already bounding your upside from falling rates.

You want to retain some rate-fall benefit without paying the cap premium

Unlike a swap, a collar lets you benefit from falling rates all the way down to the floor strike. If your view is that rates may decline modestly but could also spike, a collar gives you controlled participation in both directions.

The curve environment makes zero-cost collars attractive

In a steeply upward-sloping curve environment, zero-cost collars can be built with reasonable strike widths (e.g. 3% floor, 5% cap) because forward rates are higher out in the future, making caps more expensive relative to floors. In the current environment, where the SOFR forward curve dips before rising, the economics are less favourable for borrowers seeking tight zero-cost collars.

Valuing a Collar

A collar's mark-to-market value is the sum of the cap's value (positive for the buyer) minus the floor's value (negative for the seller). Each leg is valued independently using the Black model or a more sophisticated smile-aware model like SABR, applied to each individual caplet and floorlet.

The key inputs are:

- Forward rate curve for projecting future reference rates

- Discount curve (typically SOFR OIS for USD collars)

- Volatility surface mapping implied vol across strikes and expiries

- Strike rates for the cap and floor

- Notional schedule (which may be amortising)

The collar's net value can be positive or negative at any point in its life. If rates rise sharply, the cap leg gains value and the floor leg loses value (since the sold floor becomes further out-of-the-money), producing a net positive MTM for the borrower.

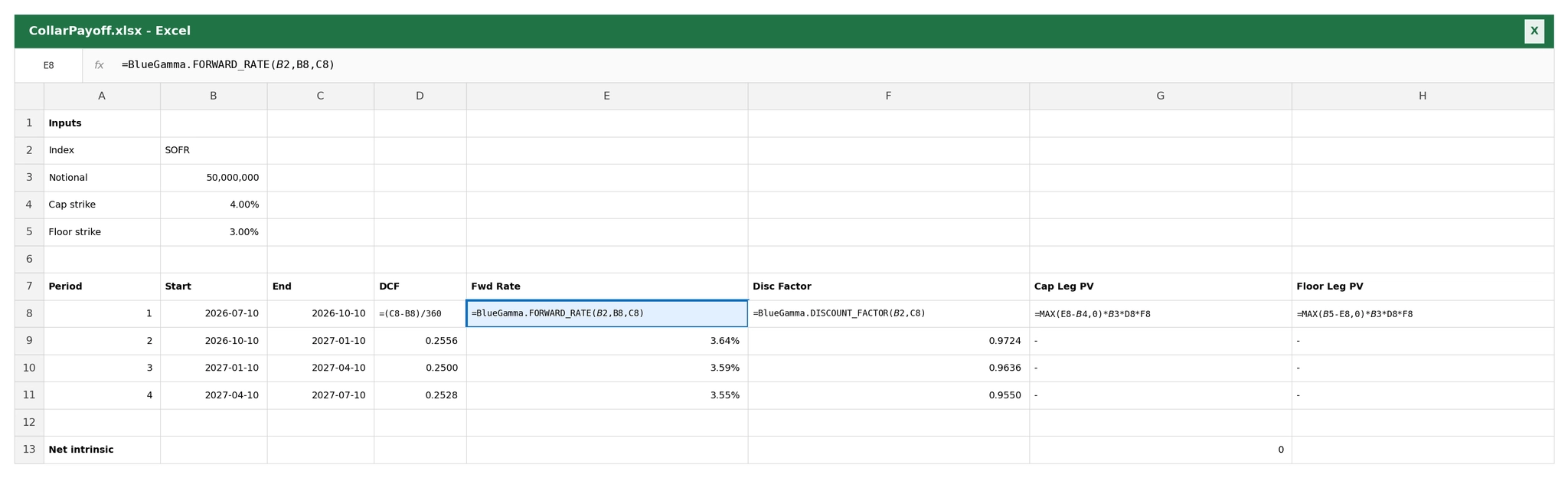

Modelling a Collar in Excel

For CRE borrowers and treasury teams building hedge models, the BlueGamma Excel add-in pulls live cap and floor pricing directly into your spreadsheet, letting you compute caplet and floorlet payoffs against the forward curve. For the full volatility-adjusted pricing, use the cap/floor pricer in the BlueGamma web app.

Accounting for Collars

Under IFRS 9 and ASC 815, an interest rate collar can qualify for hedge accounting treatment as a cash flow hedge, provided the hedge documentation and effectiveness criteria are met.

Under IFRS 9, the borrower can designate only the intrinsic value of the two options as the hedging instrument, with the time value recognised in a separate component of equity and amortised to profit or loss. Alternatively, the full fair value of the collar can be designated, with changes flowing through other comprehensive income.

One practical point: hedge effectiveness testing for collars is somewhat more involved than for swaps, because the hedge relationship is only effective within the corridor between the strikes. For rates outside the corridor, the collar provides perfect offset with the underlying floating exposure. Auditors typically accept this profile provided the testing methodology captures the behaviour across all rate scenarios.

Summary

An interest rate collar combines a cap (protection) with a sold floor (premium offset) to create a bounded rate corridor at lower upfront cost than a standalone cap. The trade-off is giving up the benefit of rates falling below the floor strike.

3-year SOFR forwards around 3.51% and floor premiums exceeding cap premiums at equivalent strikes, collar economics favour borrowers in unusual ways: a traditional 4%/3% collar can produce a net receipt rather than a net cost. Zero-cost collars in the traditional sense require higher cap strikes or lower floor strikes than in past rate environments.

This article is for informational and educational purposes only and does not constitute financial, investment, legal, or tax advice. BlueGamma does not provide advisory services. Readers should consult qualified professional advisors before entering into any derivative transaction. Market data shown is indicative and sourced from BlueGamma as of the date stated.

Frequently Asked Questions

What is an interest rate collar?

An interest rate collar is a combination of a purchased cap and a sold floor that creates a bounded range for a borrower's effective floating rate. The cap sets a ceiling; the floor sets a minimum. The premium received from the floor partially or fully offsets the cap premium.

How does a zero-cost collar work?

A zero-cost collar is a collar where the cap premium paid exactly equals the floor premium received, so no cash changes hands at inception. The floor and cap strikes are chosen to produce equal premiums based on the current forward curve and volatility surface.

Is a zero-cost collar actually free?

Not economically. The borrower gives up the benefit of rates falling below the floor strike, which is a real opportunity cost. "Zero cost" refers only to the absence of an upfront cash payment.

What happens if rates fall below the floor strike?

The borrower must pay the floor counterparty the difference between the floor strike and the lower market rate. This offsets the benefit the borrower would have received from the lower floating rate on their loan, so the effective rate is fixed at the floor strike.

How is a collar different from a swap?

A swap fixes the rate completely at a single level (typically the par swap rate). A collar keeps the rate floating within a range bounded by the floor and cap strikes. The collar provides more flexibility but less certainty than a swap.

Can a collar be terminated early?

Yes, but early termination requires unwinding both the cap and the floor with their respective counterparties, and the economics depend on where rates and volatility are at the time of termination. The sold floor leg introduces the possibility of a termination payment owed by the borrower.