Rising rates can catch borrowers off guard. Understanding the tools available to manage that risk, and choosing the right one, is one of the most important decisions a treasury team makes.

Interest rate hedging is the practice of using financial instruments to reduce or eliminate exposure to movements in interest rates. Effective interest rate risk management is essential for any organisation with floating-rate debt or rate-sensitive cash flows. Borrowers with floating-rate debt, investors with fixed-income portfolios, and corporations with rate-sensitive cash flows all use hedging strategies to manage uncertainty and protect financial outcomes.

This guide compares the main interest rate hedging instruments, explains when each is appropriate, and provides a decision framework for selecting the right strategy.

Why Hedge Interest Rate Risk

Floating-rate borrowers are exposed to the risk that reference rates rise, increasing their debt service costs. A 100 basis point increase in SOFR on $50 million of floating-rate debt adds $500,000 to annual interest expense.

Managing interest rate risk through hedging addresses this by establishing certainty over future interest costs. The specific level of certainty depends on the instrument chosen:

- A swap provides complete certainty by fixing the rate

- A cap provides a ceiling while preserving downside benefit

- A collar provides a bounded range

- A swaption provides the right, but not the obligation, to enter a swap

The Four Main Hedging Instruments

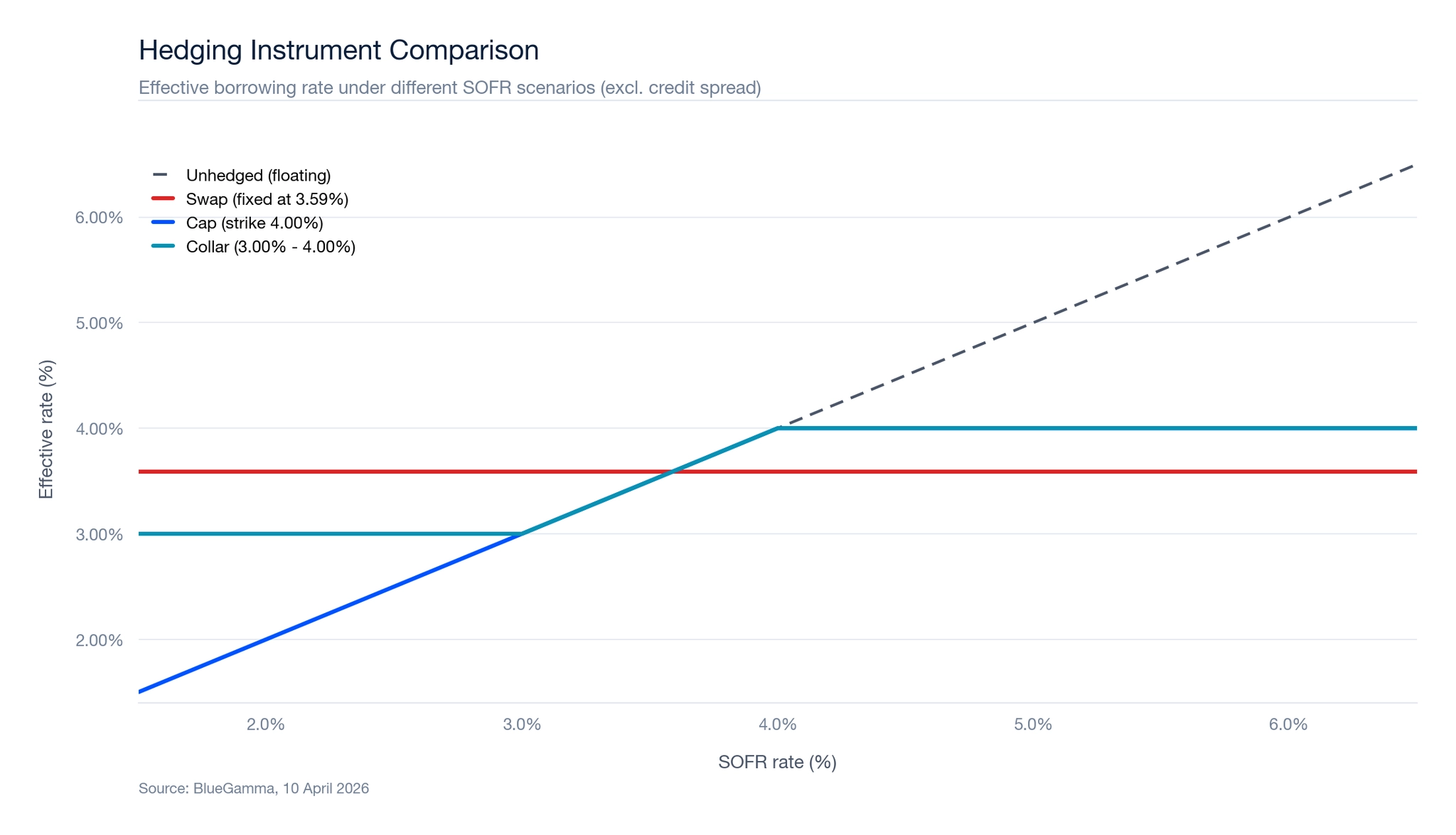

1. Interest Rate Swap

The borrower pays a fixed rate and receives the floating rate. The floating rate received offsets the floating rate on the loan, converting the obligation to fixed.

Current pricing: A 5-year SOFR swap fixes the rate at approximately 3.59%. On a $50 million loan at SOFR + 200 bps, the all-in fixed cost would be 5.59%.

Advantages: No upfront cost. Complete rate certainty. Simple to understand.

Disadvantages: No benefit if rates fall below the fixed rate. Mark-to-market can be negative, potentially requiring collateral. Early termination may involve a breakage cost.

2. Interest Rate Cap

The borrower purchases a cap that pays out when the reference rate exceeds a specified strike. The borrower retains the floating rate below the strike.

Current pricing: A 2-year SOFR cap struck at 4.00% on $50 million costs approximately $86,927 (17 bps). A 3-year cap at the same strike costs $249,744 (50 bps).

Advantages: Preserves benefit from falling rates. Mark-to-market is always positive or zero. Simple to unwind. Often required by lenders on floating-rate commercial real estate loans.

Disadvantages: Requires an upfront premium. The premium can be significant for longer tenors or lower strike rates.

3. Interest Rate Collar

The borrower buys a cap (ceiling) and simultaneously sells a floor (minimum rate). The premium from the sold floor offsets some or all of the cap premium. In a zero-cost collar, the two premiums are equal.

Current pricing: A 2-year collar on $50 million with a 4.00% cap and 3.00% floor would result in a net premium received of approximately $192,000, since the floor premium (~$279,000) exceeds the cap cost (~$87,000). For a true zero-cost collar, where no net premium changes hands, the floor strike would need to be set higher, likely around 3.40-3.50% in current market conditions. The exact zero-cost floor strike depends on the volatility surface and can be solved for using option pricing models.

Advantages: Reduced or zero upfront cost compared to a standalone cap. Provides a defined range for the effective rate.

Disadvantages: The borrower gives up benefit from rates falling below the floor. The effective range may be narrower than desired in some market environments.

4. Swaption

A swaption gives the holder the right, but not the obligation, to enter into an interest rate swap at a specified fixed rate on a future date. Swaptions are used when the borrower wants optionality around the hedging decision.

Advantages: Flexibility to decide later whether to fix. Useful for conditional exposures (e.g. planned financings that may not materialise).

Disadvantages: Requires an upfront premium. If not exercised, the premium is lost.

Comparing the Cost of Hedging

The total cost of hedging depends on both the explicit cost (premium) and the implicit cost (the rate locked in or the range established).

| Instrument | Upfront Cost | Worst-Case Rate | Best-Case Rate | Rate Certainty |

|---|---|---|---|---|

| Swap (5Y) | $0 | 3.59% | 3.59% | Fully fixed |

| Cap (2Y, 4.00%) | $86,927 | 4.00% | Market SOFR | Ceiling only |

| Collar (2Y, 3.00-4.00%) | Net ~$192K received (zero-cost collar would use a higher floor strike, around 3.40-3.50%) | 4.00% | 3.00% | Bounded range |

| Cap (3Y, 4.00%) | $249,744 | 4.00% | Market SOFR | Ceiling only |

Source: BlueGamma. Rates exclude credit spread. $50M notional.

All pricing shown is indicative and sourced from BlueGamma. The Cap Pricer provides instant cap and floor pricing across tenors and strikes, while the Swap Pricer delivers live swap rates for any currency and tenor. Both tools are available through the BlueGamma platform.

Decision Framework: Choosing the Right Hedge

The choice of hedging instrument depends on the borrower's specific circumstances:

Budget certainty is the priority

Use a swap. It eliminates all rate uncertainty and has no upfront cost. The trade-off is that the borrower cannot benefit if rates fall.

Lender requires a hedge on floating-rate debt

Use a cap. Many commercial real estate lenders mandate caps on bridge loans and transitional financing. The cap satisfies the requirement while preserving upside from rate declines.

Premium budget is limited

Use a collar. Selling a floor to offset the cap premium reduces or eliminates the upfront cost. The borrower accepts a minimum rate in exchange.

The exposure is conditional or uncertain

Use a swaption or deal-contingent hedge. If the borrower is not certain the financing will proceed (e.g. pending an acquisition), a swaption provides the right to hedge without the obligation.

The exposure is short-term (under 2 years)

A cap is often most efficient for short-duration exposures, where the premium is manageable relative to the protection.

The exposure is long-term (5+ years)

A swap is typically more cost-effective for longer tenors. Cap premiums scale significantly with duration (a 5-year cap at 4.00% costs $709,057 compared to $86,927 for 2 years), making swaps the more practical choice.

Interest Rate Hedging for Commercial Real Estate

Commercial real estate borrowers face specific hedging requirements driven by both lender mandates and the nature of transitional property assets. Bridge loans and transitional facilities, which typically carry floating rates tied to SOFR, almost universally require the borrower to purchase an interest rate cap as a condition of closing. The cap ensures that debt service coverage ratios remain within acceptable thresholds even if rates rise significantly during the business plan period.

BlueGamma's Cap Pricer is particularly relevant for CRE borrowers who need to obtain cap quotes quickly during the financing process. The tool provides indicative pricing that can be used for budgeting and comparison before approaching dealers for executable quotes.

Construction loans present a different hedging challenge. Because the loan balance increases over time as funds are drawn, borrowers may use forward-starting swaps or stepped-notional caps that align with the expected draw schedule. For stabilised assets with permanent financing, a fixed-rate swap is often the preferred instrument, as it provides the certainty lenders and investors require for long-duration hold periods.

A critical principle in CRE hedging is that the hedge term should align with the business plan hold period, not simply the loan maturity. A bridge loan borrower planning a 24-month renovation and sale should hedge for 24 months, while a core investor with a 10-year hold should consider longer-dated protection. Misalignment between the hedge tenor and the expected hold period can result in either unhedged exposure or unnecessary breakage costs at exit.

Factors That Affect Hedging Costs

The level of interest rates. Higher rates generally increase hedging costs. When the forward curve prices in rate declines (as it does currently, with SOFR expected to dip from 3.64% to 3.40% by late 2027), short-term hedges may appear cheaper because the expected floating payments are lower.

Volatility. Higher implied volatility increases option premiums (caps, floors, swaptions). During periods of monetary policy uncertainty, hedging costs tend to rise.

Tenor. Longer hedges cost more because they contain more risk. This applies to both the fixed rate in swaps (the swap curve is upward-sloping) and the premium for caps.

Strike selection. For caps, the strike rate is the single largest driver of premium. Moving the strike from 3.50% to 4.00% on a 2-year cap reduces the premium from $313,837 to $86,927.

Notional profile. Amortising structures reduce the effective notional over time, lowering the cost compared to a bullet hedge.

Common Hedging Mistakes

Over-hedging. Hedging more than the actual floating-rate exposure creates speculative risk. If a loan is prepaid or refinanced early, the excess hedge must be unwound, potentially at a loss.

Ignoring basis risk. If the loan references Term SOFR but the hedge references overnight SOFR compounded in arrears, a small but persistent basis difference may exist.

Focusing only on upfront cost. A zero-cost collar eliminates the premium but introduces a floor that may prove costly in a falling-rate environment. The cheapest hedge is not always the best hedge for the borrower's risk profile.

Failing to align payment dates. Mismatched payment dates between the loan and the hedge can create cash flow timing differences that reduce hedge effectiveness.

Hedge Accounting Considerations

Under IFRS 9 and ASC 815, hedging instruments can qualify for hedge accounting treatment, which aligns the timing of gains and losses on the hedge with the hedged item. This avoids unwanted profit-and-loss volatility.

Key requirements include formal hedge documentation at inception, ongoing effectiveness testing, and alignment between the hedge and the hedged exposure. See our hedge accounting guide for a detailed treatment of this topic.

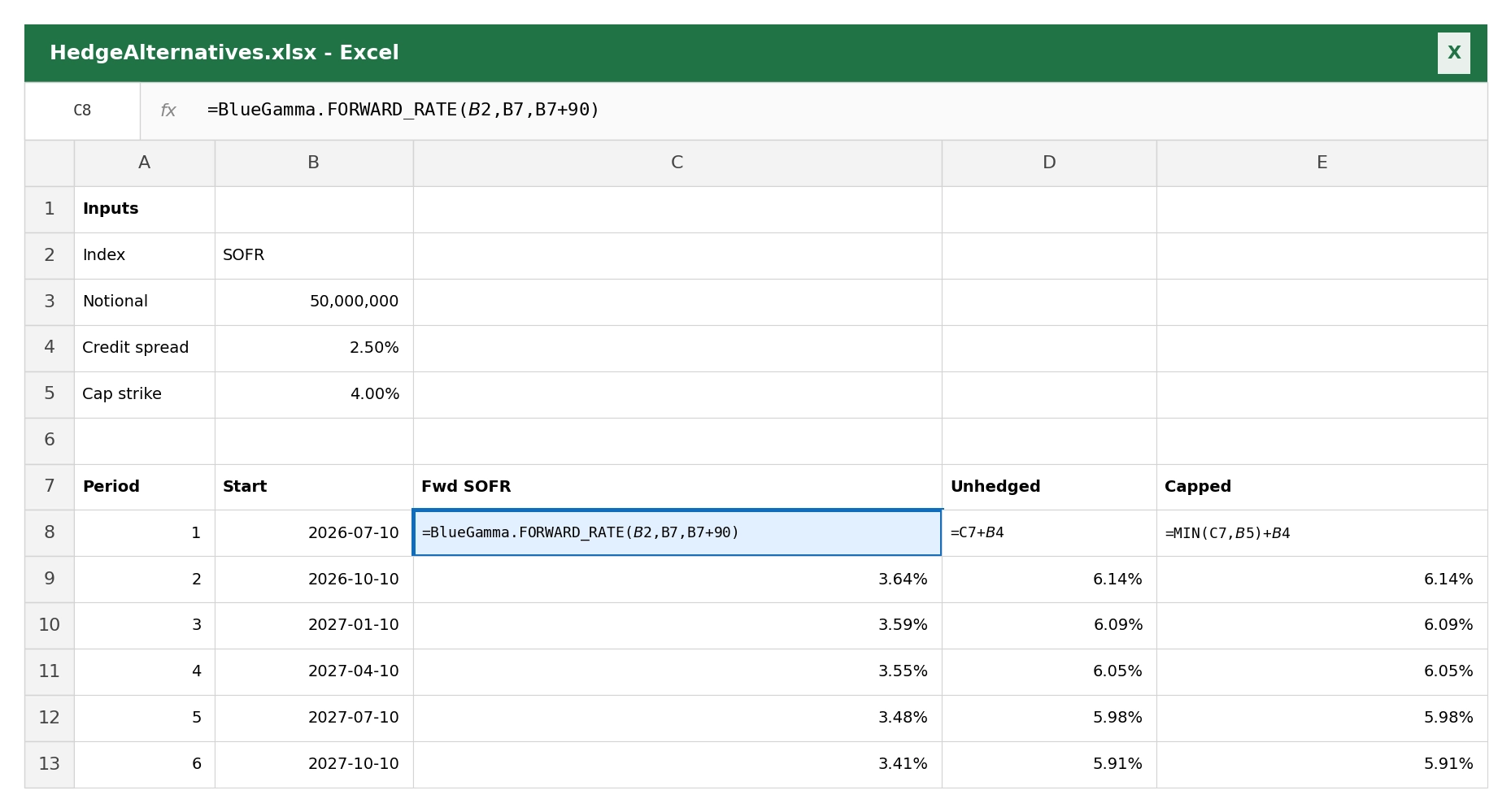

Modelling Hedge Alternatives in Excel

To compare hedging strategies in your own model, the BlueGamma Excel add-in lets you pull live swap rates, forward rates, and discount factors alongside your debt schedule.

Summary

Interest rate hedging provides certainty over future borrowing costs. The four main instruments (swaps, caps, collars, and swaptions) offer different trade-offs between cost, certainty, and flexibility.

In the current market environment, the 5-year SOFR swap rate is 3.59%, a 2-year cap at 4.00% costs 17 bps ($86,927 on $50M), and a zero-cost collar can bound the effective rate between approximately 3.00% and 4.00%. The right choice depends on the borrower's risk tolerance, budget constraints, financing structure, and market outlook.

This article is for informational and educational purposes only and does not constitute financial, investment, legal, or tax advice. BlueGamma does not provide advisory services. Readers should consult qualified professional advisors before entering into any derivative transaction. Market data shown is indicative and sourced from BlueGamma as of the date stated.

Frequently Asked Questions

How to hedge interest rate risk?

Interest rate risk can be hedged using derivative instruments that offset the impact of rate movements on an existing exposure. The most common approach for floating-rate borrowers is to enter an interest rate swap, which converts the floating obligation to a fixed rate. Alternatively, borrowers can purchase an interest rate cap to establish a ceiling on their effective rate while retaining the benefit of rate declines. The choice depends on the borrower's risk tolerance, financing structure, and cost constraints.

What is an interest rate hedge?

An interest rate hedge is a financial instrument or strategy used to reduce or eliminate exposure to changes in interest rates. Common hedging instruments include interest rate swaps, caps, collars, and swaptions. Each provides a different degree of rate certainty and carries different cost characteristics. The hedge is typically structured to mirror the terms of the underlying loan or exposure it is intended to protect.

How do banks hedge interest rate risk?

Banks hedge interest rate risk arising from the mismatch between their asset and liability profiles. A bank holding long-duration fixed-rate loans funded by short-term floating-rate deposits is exposed to rising rates. Banks use interest rate swaps to adjust the effective duration of their balance sheet, receiving fixed rates on longer-dated swaps to offset the fixed-rate assets and paying floating rates that align with their funding costs. Banks also use portfolio-level hedging strategies, managing net interest rate exposure across their entire book rather than hedging each position individually.

What is the best way to hedge against rising interest rates?

The most direct hedge against rising rates is an interest rate swap, which fully fixes the borrower's rate and eliminates exposure to further increases. For borrowers who want protection against rate spikes but prefer to retain some floating-rate benefit, an interest rate cap provides a ceiling on the effective rate. The optimal approach depends on the borrower's view on rates, the duration of the exposure, and whether the lender has specific hedging requirements.