By Ahmed Babikir and Ali Vohra. Originally published October 2024. Updated April 2026.

Hedge accounting might sound like a complicated term, but it helps maintain stability in financial statements. By managing financial risks in a disciplined way, companies can focus on growth without worrying about market-driven surprises showing up in their reported earnings.

Think of it like a seesaw: one side is the gains on your hedging instrument, and the other side is the losses on the item you're protecting. Hedge accounting is the set of rules that lets you report both sides in the same period so the seesaw sits level in your P&L, instead of one side tipping violently while the other side waits to catch up.

This guide walks through what hedge accounting is, the three models available under IFRS 9 and ASC 815, how cash flow hedges differ from fair value hedges, a practical seven-step implementation checklist, common pitfalls, and answers to the questions we hear most often.

What is Hedge Accounting?

Hedge accounting is a set of rules under financial reporting standards that allows companies to align the timing of gains and losses on hedging instruments with the items they are hedging. Without hedge accounting, a derivative used for hedging is marked to market through profit and loss each period, creating volatility in reported earnings even though the underlying economic exposure is effectively hedged.

The two primary frameworks are IFRS 9 (used internationally) and ASC 815 - Derivatives and Hedging (used under US GAAP). While they differ in detail, both share the same objective: to reflect the economic substance of hedging relationships in financial statements.

Key Principles and Objectives

Consider a company that enters into a 5-year interest rate swap to fix its floating-rate borrowing costs. Without hedge accounting:

- The swap is reported at fair value on the balance sheet

- Changes in fair value flow directly through profit and loss each reporting period

- If rates drop by 50 basis points, the swap might show a mark-to-market loss of several hundred thousand dollars, hitting the income statement

- The corresponding benefit (lower future borrowing costs) is not recognised until those costs are actually incurred

This creates a timing mismatch in the financial statements. The hedge is working as intended economically, but the accounting treatment makes earnings appear volatile. Hedge accounting solves this by matching gains and losses on the hedging instrument with the hedged item, either in the same P&L period or by deferring them in other comprehensive income (OCI).

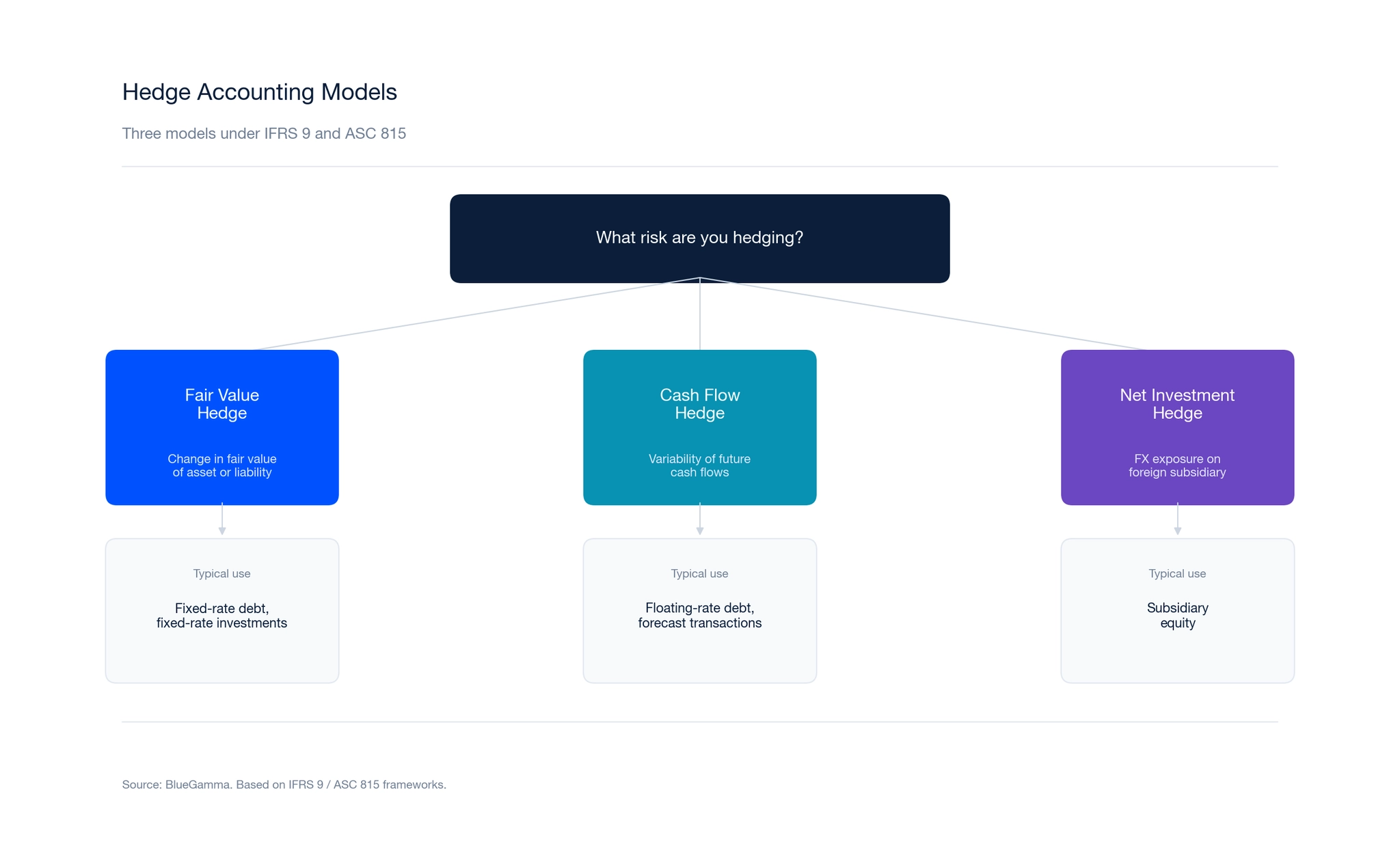

The Three Hedge Accounting Models

1. Fair Value Hedge

A fair value hedge protects against changes in the fair value of a recognised asset, liability, or firm commitment due to a particular risk.

How it works: Both the hedging instrument and the hedged item are marked to market, with changes recognised in profit and loss. Because they move in opposite directions, the net P&L impact is minimal (limited to hedge ineffectiveness).

Common example: A company with fixed-rate debt enters a receive-fixed, pay-floating swap. The swap is the hedging instrument. The hedged item is the fair value of the debt attributable to interest rate risk. When rates rise, the swap gains value and the debt loses value, approximately offsetting. For a deeper look at how these instruments are valued, see our guide to derivative valuation methods, models, and applications.

Key point: In a fair value hedge, the carrying amount of the hedged item on the balance sheet is adjusted for the hedged risk. This is sometimes called a "basis adjustment."

2. Cash Flow Hedge

A cash flow hedge protects against variability in future cash flows attributable to a particular risk. This is the most common model for corporate borrowers hedging floating-rate debt.

How it works: The effective portion of the gain or loss on the hedging instrument is recognised in other comprehensive income (OCI) and recycled to P&L when the hedged cash flow affects earnings. The ineffective portion is recognised in P&L immediately.

Common example: A company with floating-rate debt at SOFR + 200 bps enters a pay-fixed, receive-SOFR swap. Each quarter, the swap's effective gain or loss is deferred in OCI. When the hedged interest payment is made, the deferred amount is released from OCI to P&L, offsetting the variable interest expense.

Key point: Cash flow hedge accounting preserves earnings stability. The swap's mark-to-market movements are largely invisible in the income statement, appearing only in OCI. You can see how swap mark-to-market values are calculated in practice using our Swap MTM tool.

3. Net Investment Hedge

A net investment hedge protects against foreign exchange exposure arising from a net investment in a foreign operation.

How it works: The effective portion of the gain or loss on the hedging instrument is recognised in OCI (within the foreign currency translation reserve). It is recycled to P&L only when the foreign operation is disposed of.

Common example: A US parent company with a EUR-denominated subsidiary uses an FX forward or a cross-currency swap to hedge the EUR/USD translation exposure on its net investment.

Cash Flow Hedge vs Fair Value Hedge

The distinction between cash flow hedges and fair value hedges is one of the most important concepts in hedge accounting under both ASC 815 and IFRS 9. The two models address different types of risk and produce different accounting outcomes.

A cash flow hedge protects against variability in future cash flows. The most common application is a corporate borrower with floating-rate debt that enters a pay-fixed, receive-floating interest rate swap. The effective portion of the swap's mark-to-market movement is deferred in OCI and recycled to profit and loss as the hedged cash flows affect earnings. This preserves earnings stability because the swap's fair value changes do not flow through the income statement.

A fair value hedge protects against changes in the fair value of a recognised asset or liability. The most common application is a financial institution with fixed-rate assets or liabilities that enters a receive-floating, pay-fixed swap. Under fair value hedge accounting, both the hedging instrument and the hedged item are marked to market through profit and loss, producing an approximately neutral net P&L impact (limited to ineffectiveness).

| Feature | Cash Flow Hedge | Fair Value Hedge |

|---|---|---|

| Hedged risk | Variability of future cash flows | Change in fair value of asset/liability |

| Typical use | Floating-rate debt hedged with pay-fixed swap | Fixed-rate debt hedged with receive-fixed swap |

| P&L treatment | Effective portion through OCI | Both hedge and hedged item through P&L |

| Balance sheet | Hedged item at amortised cost | Hedged item adjusted for hedged risk |

| Most common for | Corporate borrowers with floating debt | Financial institutions with fixed-rate portfolios |

The choice between the two models is determined by the nature of the underlying exposure, not by preference. ASC 815 and IFRS 9 both require that the hedge designation match the actual risk being managed.

How to Implement Hedge Accounting

Steps for Getting Started

Implementing hedge accounting is a structured process. The following seven-step checklist is a practical way to move from "we have derivatives" to "we have a qualifying hedge relationship":

- Identify Hedging Relationships - Define precisely which risk on which item is being hedged (e.g. floating-rate interest risk on a specific facility).

- Determine the Hedge Type - Decide whether the exposure fits a fair value hedge, a cash flow hedge, or a net investment hedge.

- Select Financial Instruments - Choose hedging instruments (swaps, caps, forwards, cross-currency swaps) whose critical terms align with the hedged item.

- Establish and Document Hedge Objectives - Prepare the formal inception documentation covering the risk management objective, hedge ratio, hedged item, hedging instrument, and effectiveness assessment methodology. This must be in place at the start of the hedge - retrospective designation is not permitted.

- Set Up Testing Procedures - Define how effectiveness will be assessed at inception and on an ongoing basis (dollar offset, regression, hypothetical derivative, or critical terms match).

- Training and Development - Make sure the finance and treasury teams understand the designation rules, journal entries, and disclosure requirements for each model.

- Communication - Coordinate across treasury, accounting, FP&A, and auditors so that everyone agrees on how the hedge will be documented, tested, and reported.

Documentation and Disclosure Requirements

Under both ASC 815 and IFRS 9, companies must formally designate the hedging relationship at inception and document:

- The hedging instrument and the hedged item

- The nature of the risk being hedged

- The hedge effectiveness assessment methodology

- The hedge ratio

Eligible hedging instruments. Most derivatives qualify, including interest rate swaps, caps, floors, collars, FX forwards, and cross-currency swaps. Under IFRS 9, a company may designate only the intrinsic value of an option (excluding time value) or only the spot element of a forward contract.

Eligible hedged items. The hedged item must be a recognised asset or liability, a firm commitment, a highly probable forecast transaction, or a net investment in a foreign operation.

Assessing and Measuring Effectiveness

The hedging relationship must be expected to be highly effective in achieving offsetting changes in fair value or cash flows. Under IFRS 9, this is assessed through three criteria:

- Economic relationship between the hedged item and the hedging instrument

- Credit risk does not dominate the value changes

- Hedge ratio is consistent with the entity's risk management strategy

In practice under ASC 815, "highly effective" has historically been interpreted by reference to an 80-125% offset range (originating from SEC staff guidance and industry practice under the original FAS 133 regime, rather than from the codification text itself). ASU 2017-12 introduced more flexibility, permitting qualitative subsequent assessments in many cases where the initial quantitative test passes and critical terms remain unchanged.

Common effectiveness testing methods:

- Dollar offset method - Compares the change in fair value of the hedging instrument with the change in fair value of the hedged item.

- Regression analysis - Statistical method that tests the correlation between changes in the hedging instrument and the hedged item over a historical period.

- Hypothetical derivative method - Compares the hedging derivative with a "perfect" hypothetical derivative that exactly matches the hedged item. Widely used for cash flow hedges of interest rate risk.

- Critical terms match - A qualitative approach that assumes the hedge is highly effective if the critical terms (notional, currency, index, maturity, payment dates) match.

IFRS 9 vs ASC 815: Key Differences

| Feature | IFRS 9 | ASC 815 |

|---|---|---|

| Effectiveness threshold | No fixed quantitative threshold | Historically interpreted as 80-125% (via SEC staff guidance); relaxed under ASU 2017-12 |

| Option time value | Can be excluded and amortised through OCI | Can be amortised systematically under ASU 2017-12 |

| Forward element | Can be excluded as cost of hedging | Similar treatment available under ASU 2017-12 |

| Risk components | Can hedge a risk component of a non-financial item | More restrictive for non-financial items |

| Portfolio layer method | Not available | Available for fair value hedges of interest rate risk |

| Rebalancing | Required when hedge ratio drifts | Less prescriptive |

The Portfolio Layer Method (ASC 815)

The portfolio layer method was originally introduced as the "last-of-layer" method by ASU 2017-12, and was subsequently expanded and renamed by ASU 2022-01. ASU 2022-01's key changes were:

- Permitting multiple hedged layers within the same closed portfolio (rather than a single "last-of-layer")

- Expanding the scope to include closed portfolios of prepayable and non-prepayable financial assets

- Clarifying how basis adjustments must be maintained and allocated

The method allows companies to designate one or more layers of a closed portfolio of financial assets as the hedged item in a fair value hedge of interest rate risk. This is particularly useful for banks hedging interest rate risk on loan portfolios, including prepayable portfolios such as mortgages. The method designates a layer of the portfolio that is expected to remain outstanding throughout the hedge period, even after prepayments, avoiding the need for loan-level designation.

Challenges and Best Practices in Hedge Accounting

Common Pitfalls to Avoid

- Late or incomplete inception documentation. Hedge accounting cannot be applied retrospectively. If the documentation is not in place at designation, the relationship will not qualify.

- Mismatch between hedged risk and hedging instrument. Using a swap with terms that don't align with the hedged item creates ineffectiveness and may disqualify the hedge.

- Weak ongoing monitoring. Hedge accounting is not "set and forget". Effectiveness must be assessed on an ongoing basis and documentation updated as circumstances change.

- Treating de-designation as optional. If the hedged item is extinguished or the hedge no longer qualifies, de-designation is required and has specific accounting consequences.

Common Misconceptions

"Hedge accounting is optional, so it doesn't matter." While hedge accounting is elective, not applying it can create significant P&L volatility from derivative mark-to-market movements. For companies with material derivative portfolios, this volatility can confuse investors and analysts.

"The hedge must be perfectly effective." Neither IFRS 9 nor current ASC 815 guidance requires perfect effectiveness. IFRS 9 does not specify a quantitative threshold. The requirement is that the hedging relationship is expected to achieve effective offsetting.

"Once designated, the hedge accounting treatment is automatic." Hedge accounting requires ongoing monitoring, effectiveness assessment, and documentation. Failure to maintain these requirements can result in discontinuation.

"You can only hedge with vanilla instruments." While plain vanilla swaps and forwards are most common, more complex instruments can qualify, provided they meet the designation and effectiveness criteria.

"Own credit risk adjustments live in the hedge accounting standards." The requirement to reflect own credit risk in the fair value of financial liabilities designated at FVTPL sits in ASC 825-10 (not ASC 820) and IFRS 9.5.7.7 (not IFRS 13). It is related to derivative valuation but is not a hedge accounting requirement.

Strategies for Effective Management

- Centralise hedge accounting policy decisions in treasury or a specialist accounting team

- Invest in systems that produce consistent mark-to-market valuations and audit trails

- Engage auditors early on significant new hedge relationships

- Keep documentation templates standardised so new hedges can be designated quickly

Future Trends and Innovations

Regulatory updates (such as ASU 2017-12 and ASU 2022-01 in the US) have generally moved toward making hedge accounting more accessible and better aligned with risk management practice. Expect continued convergence between IFRS 9 and ASC 815 on effectiveness concepts, and growing use of the portfolio layer method for balance-sheet hedging at banks.

Summary

Hedge accounting lets companies align derivative mark-to-market movements with the underlying economic exposure, reducing P&L volatility from effective hedging relationships. The three models (fair value, cash flow, and net investment) serve different hedging objectives. Successful implementation requires formal documentation at inception, ongoing effectiveness monitoring, and alignment between the hedging instrument and the hedged item.

This article is for informational and educational purposes only and does not constitute financial, investment, legal, tax, or accounting advice. BlueGamma does not provide advisory services. Readers should consult qualified professional advisors, including their auditors, before implementing hedge accounting. Market data shown is indicative and sourced from BlueGamma as of the date stated.

Frequently Asked Questions

What is meant by hedge accounting?

Hedge accounting is an elective set of rules under IFRS 9 and ASC 815 that allows companies to match the timing of gains and losses on hedging derivatives with the items they hedge. Without it, derivative mark-to-market movements flow directly through profit and loss, creating earnings volatility even when the hedge is economically effective.

What is an example of hedge accounting?

A company with floating-rate debt at SOFR + 200 bps enters a pay-fixed, receive-SOFR interest rate swap and designates it as a cash flow hedge. Each period, the effective portion of the swap's mark-to-market is deferred in OCI and recycled to P&L when the hedged interest payment is made, stabilising the reported interest expense.

What is IFRS 9 hedge accounting?

IFRS 9 is the international accounting standard covering hedge accounting. It requires formal designation and documentation, allows three hedge models (fair value, cash flow, and net investment), and assesses effectiveness through an economic relationship test, a credit risk test, and a hedge ratio test rather than a fixed numerical threshold.

Is hedge accounting OCI or P&L?

It depends on the model. Fair value hedges flow through P&L for both the hedge and the hedged item. Cash flow hedges defer the effective portion in OCI and recycle it to P&L when the hedged cash flow affects earnings. Net investment hedges sit in OCI and are recycled only on disposal of the foreign operation.

What is the difference between ASC 815 and IFRS 9?

ASC 815 is the US GAAP standard; IFRS 9 is the international standard. Key differences: ASC 815 has been historically interpreted via an 80-125% effectiveness range (since relaxed); IFRS 9 has no fixed quantitative threshold. IFRS 9 allows hedging of risk components of non-financial items more broadly. ASC 815 offers the portfolio layer method, which IFRS 9 does not.

What is a cash flow hedge?

A cash flow hedge protects against variability in future cash flows attributable to a particular risk, such as a floating interest rate. The effective portion of the hedging instrument's gain or loss is deferred in OCI and released to P&L when the hedged cash flow affects earnings.

How do you test hedge effectiveness?

The main methods are the dollar offset method, regression analysis, the hypothetical derivative method, and critical terms match. The choice depends on the complexity of the hedge and the requirements of the applicable standard.

Is there Hedge Accounting Software?

Yes. A range of treasury and derivative valuation platforms support hedge designation, effectiveness testing, journal entry generation, and disclosure reporting. At BlueGamma we provide derivative valuation tools that support mark-to-market reporting and hedge effectiveness testing.