If you have ever watched the Bank of England cut the base rate and then wondered why your fixed mortgage quote barely moved, you have already met the gap this article explains.

Here is the short version: tracker mortgages follow the Bank of England base rate. Fixed rate mortgages follow swap rates. Most UK borrowers are on fixes, which means the number that actually sets their rate is one most people have never heard of.

This guide explains what swap rates are, how they feed into mortgage pricing, and how to read them yourself, with no derivatives background required. It draws on our analysis of five and a half years of Bank of England mortgage data against daily SONIA swap rates, so the numbers here are measured, not guessed.

What are swap rates?

A swap rate is the fixed interest rate a lender can lock in today, for a set number of years, in exchange for the floating overnight rate. It is the market price of borrowing certainty for two, three, five or ten years.

To see why that matters, imagine you run a mortgage lender. A customer wants to borrow at a fixed rate for five years. Your problem: the money you lend out is funded at rates that change every single day. If funding costs rise over those five years, you lose money on a loan whose income is locked.

So you do what any sensible business does with a risk it cannot control: you pay someone else to take it. In financial markets, that deal is called an interest rate swap. The lender agrees to pay a single fixed rate for the whole term, and in exchange receives whatever the floating overnight rate turns out to be, day after day, for five years. The floating income offsets the floating funding cost, and the lender is left paying one known, fixed rate.

That fixed rate is the swap rate. It is, quite literally, the price of certainty.

A useful way to think about it: the swap rate is the market's best guess of where overnight interest rates will average over that period, plus a little for the risk of being wrong. A 5 year swap rate of 4% roughly says "the market expects overnight rates to average about 4% over the next five years."

Once you see that, mortgage pricing stops being mysterious. A lender offering a 5 year fix simply takes the 5 year swap rate, adds a margin for costs, risk and profit, and that is your headline mortgage rate.

What is SONIA?

SONIA stands for the Sterling Overnight Index Average: the average interest rate at which banks borrow sterling overnight, published by the Bank of England every business day. It is about as close to a risk-free interest rate as sterling markets have, and it replaced LIBOR as the UK's benchmark rate.

A SONIA swap is the standard version of the deal described above: one side pays a fixed rate, the other pays compounded SONIA, over an agreed term. When brokers or journalists talk about "swap rates" moving, they almost always mean SONIA swap rates.

SONIA itself hugs the Bank of England base rate closely. But a 5 year SONIA swap rate is not today's SONIA. It is the market's view of the whole path of SONIA over the next five years. That distinction is the key to everything that follows.

What makes swap rates move?

Swap rates move whenever the market changes its mind about where interest rates are heading. The main drivers are:

- Inflation data. Higher than expected inflation makes markets price in higher rates for longer, and swap rates rise, often within minutes of the release.

- Bank of England signals. Speeches, votes and forecasts shift expectations of the future path of the base rate, which is exactly what a swap rate prices.

- The wider bond market. Swap rates move with gilt yields, so global forces that push government borrowing costs around, from US inflation surprises to geopolitical shocks, feed straight into UK swaps.

- Risk events. Moments of stress can move swaps violently. The 2022 mini-budget moved them further in days than the Bank of England moved the base rate in months.

This is why fixed mortgage pricing can change in weeks when the base rate has not moved at all. The swap market never waits for the announcement. We cover the link between data releases and swap moves in more depth in how economic events drive swap rate news.

How do swap rates affect mortgage rates?

Directly: lenders price a fixed mortgage by taking the swap rate for the matching term and adding a margin. When the 5 year swap moves, the 5 year fix follows.

This is where the base rate confusion unravels. When the Bank of England cuts the base rate, tracker mortgages reprice the same day, because that is what trackers contractually do. Fixed rates often do very little, and sometimes move the "wrong" way. Why? Because if the market already expected the cut, it was priced into swap rates weeks earlier. The swap market moves on expectations, not announcements. By the time the Bank acts, the fix has usually already repriced.

How tight is the link in practice? We compared five and a half years of Bank of England quoted mortgage rates (2 and 5 year fixes at 75% LTV, monthly advertised averages) against daily SONIA swap rates. Three findings stand out:

- Roughly 85% of any swap move eventually shows up in mortgage rates. The link is not one-for-one, but it is strong and persistent, and in the data it runs one way: swap moves lead mortgage moves, not the reverse.

- The average margin of 5 year fixes over 5 year swaps is about 0.6% (59 basis points). The margin varies with market conditions, but it is remarkably stable compared with the rates themselves.

- Swap moves are fully visible in the market average within a month. Individual lenders reprice within days of a big swap move, and the whole market's advertised average catches up as lender after lender updates its range. One caveat worth knowing: the Bank of England data is monthly, so a month is the finest lag it can measure. Treat it as a ceiling, not a stopwatch: on the way up, much of the market has typically moved within a couple of weeks.

As a worked example: if the 5 year swap rate rises by 0.50%, history says advertised 5 year fixes rise by roughly 0.40% to 0.45%, with most of that arriving within a month or two.

That margin is usually stable, but it can break in a crisis. In October 2022, after the mini-budget, swap rates spiked so fast that the margin briefly went negative: lenders were, on paper, advertising mortgages below their own funding cost. Their response was rational and dramatic. They pulled hundreds of products overnight rather than lend at a loss, and repriced the market upwards within days. It remains the clearest demonstration that swap rates, not the base rate, are the live wire under fixed mortgage pricing.

Up like a rocket, down like a feather

Anyone who drives will recognise this. When oil prices jump, petrol pump prices jump the next morning. When oil prices fall, pump prices drift down slowly, as if reluctant. Economists call it "rockets and feathers", and it is one of the most studied pricing patterns in economics.

Mortgage rates do exactly the same thing with swap rates.

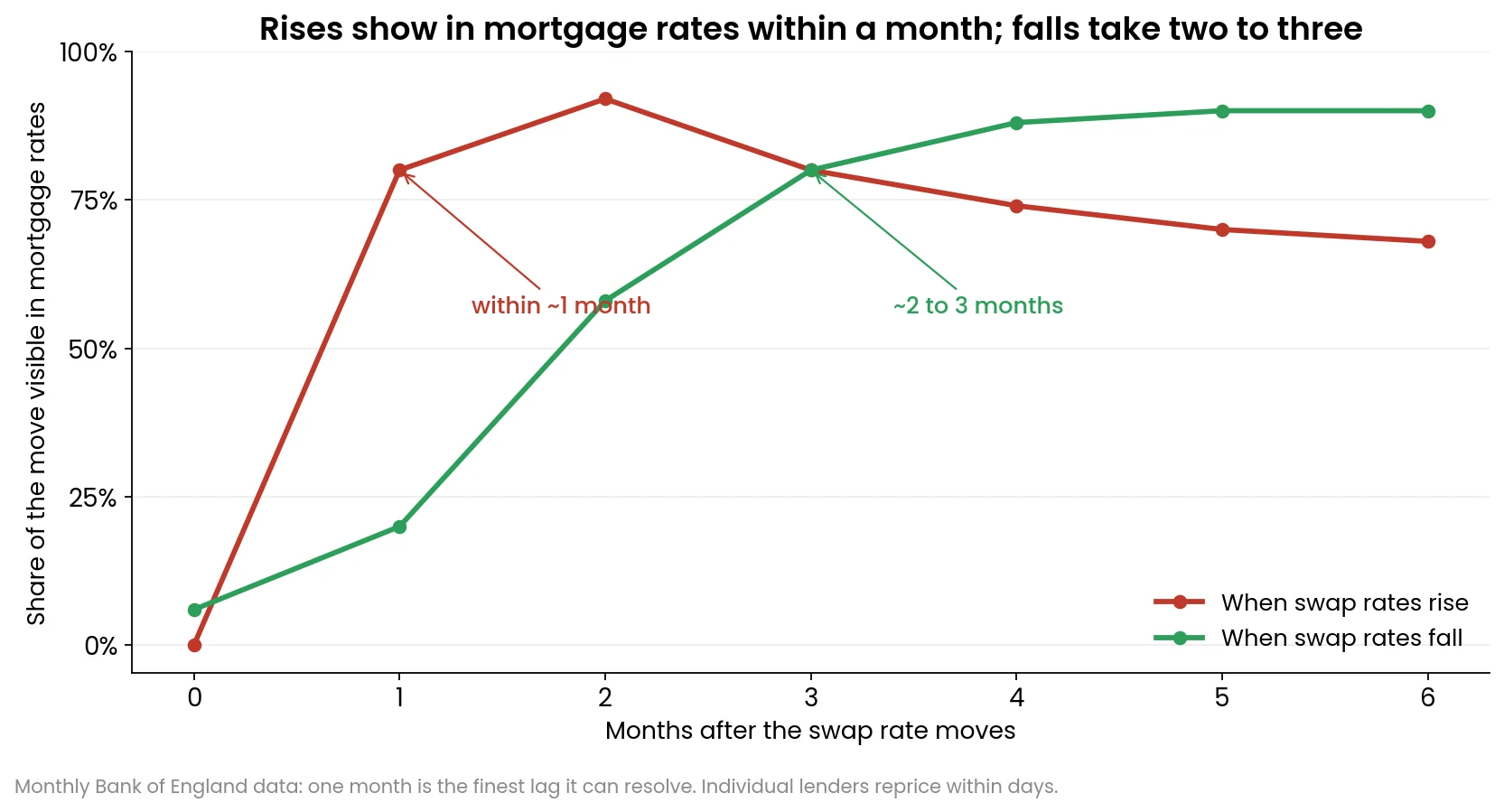

In our analysis, swap rate rises were fully reflected in advertised mortgage rates within a month. Falls took two to three months. Because the mortgage data is monthly, "within a month" is an upper bound: individual lenders often reprice rises within days. The asymmetry is statistically significant, not just an impression. When funding costs rise, lenders reprice quickly to protect margins. When funding costs fall, they let the wider margin sit for a while before competition grinds it back down.

| Months after the swap move | Rise: share visible | Fall: share visible |

|---|---|---|

| 1 month | ~80% | ~20% |

| 2 months | Fully passed through | ~60% |

| 3 months | Fully passed through | ~80% |

| 4 to 5 months | Fully passed through | Fully passed through |

For a borrower or broker, the factual takeaway: in the historical data, after swap rates fell, the market average was typically still adjusting two to three months later. The feather takes longer to land than the rocket takes to launch.

Why are fixed rates sometimes cheaper than trackers?

Because they are priced off different things.

| Tracker mortgage | Fixed rate mortgage | |

|---|---|---|

| Priced off | Bank of England base rate, today | Swap rate for the matching term |

| Moves when | The Bank announces a change | Market expectations shift, any trading day |

| Reacts to a base rate cut | Same day, automatically | Usually already priced in weeks earlier |

| What to watch | MPC announcements | SONIA swap rates |

A tracker is priced off the base rate today. A fix is priced off swap rates, which reflect where the market thinks rates are going. If the market expects rate cuts, swap rates sit below the current base rate, and a fixed mortgage can be cheaper than a tracker even though "locking in" intuitively sounds like it should cost more.

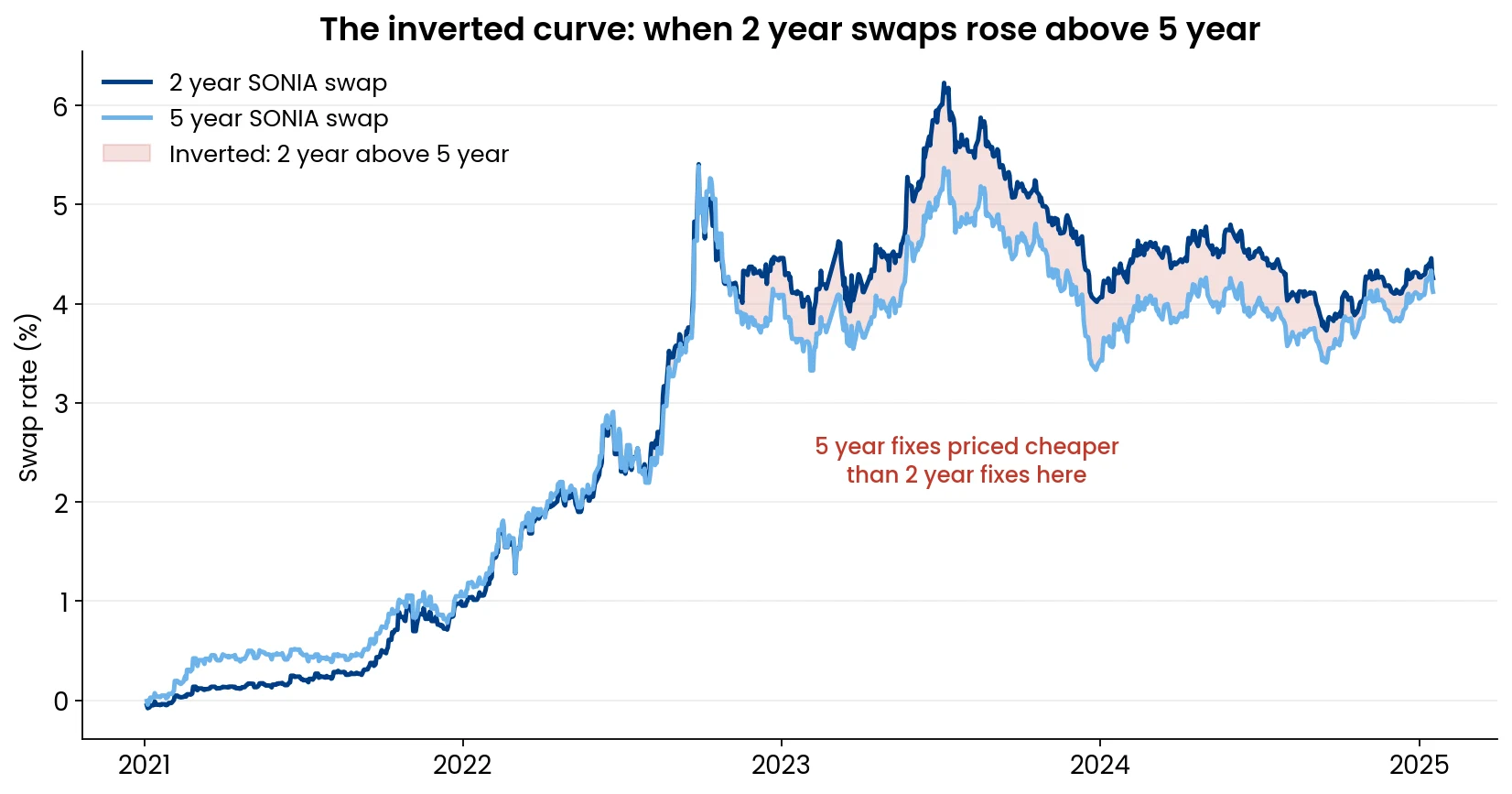

The same logic produces another oddity: 5 year fixes cheaper than 2 year fixes. For long stretches of the recent rate cycle, 2 year swap rates sat above 5 year swap rates, a so-called inverted curve, because markets expected rates to rise sharply and then come back down. Lenders priced their fixes accordingly, and borrowers found the longer lock-in was the cheaper one. Nothing was broken. The curve was simply telling you what the market expected.

Are swap rates going up or down?

The honest answer is that any direction printed here would be stale within a week, so here is how to check for yourself in under a minute:

- Live levels: current SONIA swap rates across tenors are published on BlueGamma's live SONIA swap rates page. If swaps have moved meaningfully in recent weeks, advertised fixes have historically followed within a month at most, and noticeably faster when the move was upward.

- Direction of travel: the SONIA forward curve shows the path of overnight rates the market is currently pricing in, in effect the market's implied forecast for the Bank of England. A downward-sloping forward curve means cuts are already baked into today's swap rates, which is why fixes will not necessarily fall further when those cuts are delivered. For a worked example of the forward curve versus what actually happened, see our realised SONIA vs forward curve case study.

A second useful habit: compare the 2 year swap with the 5 year swap. The slope between them has historically matched which fix tenors lenders priced lower, as the inverted-curve episode showed.

The relationship in five lines

- Fixed mortgages are priced off SONIA swap rates plus a margin; trackers follow the base rate

- About 85% of a swap move eventually passes into mortgage rates

- The 5 year fix margin over 5 year swaps has averaged about 0.6%

- Swap rises show in advertised rates within a month (often days at individual lenders); falls take two to three

- Swaps move first, every time: they lead mortgage rates, never follow them

Sources: Bank of England quoted household interest rates (2 year and 5 year fixed, 75% LTV); SONIA swap rates from BlueGamma.

Curious what swap rates are doing right now? The live SONIA swap rates are free to check, updated daily, and take about ten seconds to read. Once you have watched them for a couple of weeks, mortgage repricing announcements stop being surprises.

Do swap rates follow the Bank of England base rate?

Loosely, but they lead rather than follow. Swap rates price in expected base rate moves before they happen, which is why fixed mortgage rates often move ahead of Bank of England announcements and barely react on the day itself.

How quickly do mortgage rates respond to swap rates?

Within a month for the market's advertised average, and that month is a ceiling set by monthly data rather than a precise measurement: individual lenders reprice within days of big moves, so rises typically reach much of the market within a couple of weeks. Falls take two to three months, with roughly 85% of any move eventually passing through.

How often do swap rates change?

Continuously, through every trading day, just like bond yields. Mortgage rates change far less often because lenders reprice their ranges in discrete steps, which is exactly why swaps are worth watching between repricing rounds.

What is a typical lender margin over swap rates?

In our analysis, 5 year fixes at 75% LTV averaged about 0.6% above 5 year SONIA swaps. The margin varies with conditions, widens in volatile markets, and briefly turned negative in October 2022.

Why did 5 year fixes get cheaper than 2 year fixes?

Because the swap curve inverted: markets expected rates to fall over time, so 5 year swaps traded below 2 year swaps, and lenders' fixed rate pricing followed suit.