An interest rate cap is a derivative contract that protects the buyer against rising interest rates. Sometimes referred to as a cap rate derivative, it is one of the most accessible hedging tools available to borrowers. The buyer pays an upfront premium and, in return, receives payments whenever a reference rate exceeds a predetermined strike rate over the life of the contract. Interest rate caps are among the most widely used hedging instruments in commercial real estate, project finance, and corporate lending.

This guide covers how interest rate caps work, when they are appropriate, how premiums are determined, and how they compare to other hedging instruments.

How an Interest Rate Cap Works

An interest rate cap is an agreement between two parties: the buyer (typically a borrower) and the seller (typically a bank or financial institution). The contract is defined by four key parameters:

- Notional amount - the principal balance on which payments are calculated

- Strike rate - the maximum interest rate the buyer is willing to bear

- Reference rate - the floating benchmark (such as SOFR, EURIBOR, or SONIA) against which the strike is measured

- Term - the duration of the cap agreement, typically aligned with the underlying loan

At each reset date, the reference rate is compared to the strike rate. If the reference rate exceeds the strike, the cap seller compensates the buyer for the difference, applied to the notional amount for that period. If the reference rate remains at or below the strike, no payment is made.

In practice, this means the borrower's effective interest rate never exceeds the strike rate plus any applicable credit spread, regardless of how high the reference rate moves.

Interest Rate Caps and Caplets

An interest rate cap is technically a series of individual options known as caplets. Each caplet corresponds to a single reset period within the cap's term.

For example, a two-year cap on three-month SOFR consists of seven caplets, each covering a consecutive quarterly period. Each caplet functions as an independent call option on the reference rate for its specific period.

This distinction matters for valuation. The price of an interest rate cap is the sum of all its constituent caplet values, each of which depends on the forward rate, volatility, and time to expiry for that particular period. Periods where forward rates are closer to or above the strike will produce more expensive caplets.

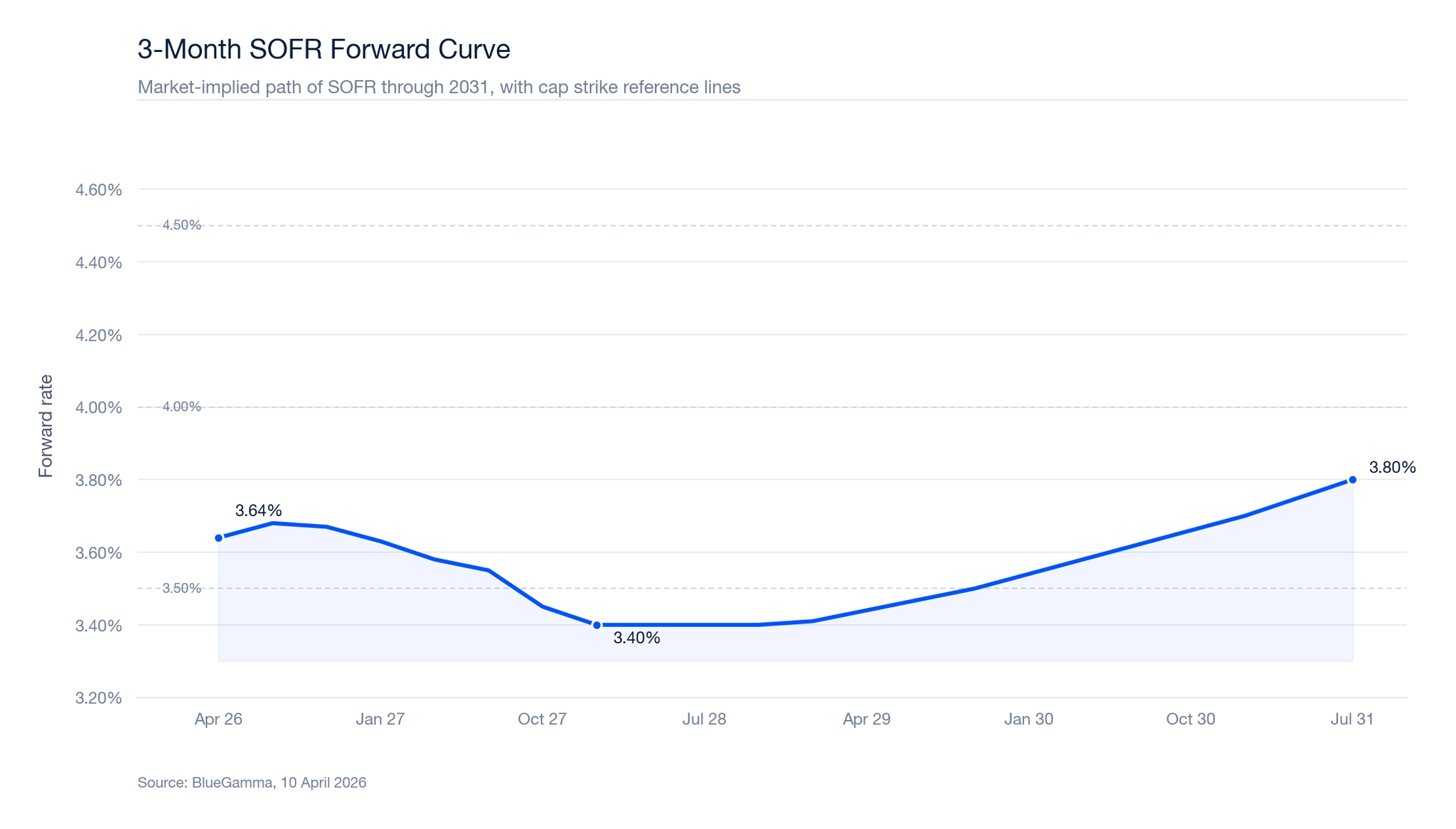

The SOFR Forward Curve: Where Markets Expect Rates to Go

Before examining cap pricing in detail, it is helpful to understand the current shape of the SOFR forward curve. The forward curve reflects the market's implied expectation of where three-month SOFR will be at each future date.

| Period Start | Period End | 3M SOFR Forward Rate |

|---|---|---|

| Apr 2026 | Jul 2026 | 3.64% |

| Jul 2026 | Oct 2026 | 3.68% |

| Oct 2026 | Jan 2027 | 3.67% |

| Jan 2027 | Apr 2027 | 3.63% |

| Apr 2027 | Jul 2027 | 3.58% |

| Jul 2027 | Oct 2027 | 3.55% |

| Oct 2027 | Jan 2028 | 3.45% |

| Jan 2028 | Apr 2028 | 3.40% |

| Apr 2028 | Jul 2028 | 3.40% |

| Jul 2028 | Oct 2028 | 3.40% |

| Oct 2028 | Jan 2029 | 3.40% |

| Jan 2029 | Apr 2029 | 3.41% |

| Apr 2029 | Jul 2029 | 3.44% |

| Jul 2029 | Oct 2029 | 3.47% |

| Oct 2029 | Jan 2030 | 3.50% |

| Jan 2030 | Apr 2030 | 3.54% |

| Apr 2030 | Jul 2030 | 3.58% |

| Jul 2030 | Oct 2030 | 3.62% |

| Oct 2030 | Jan 2031 | 3.66% |

| Jan 2031 | Apr 2031 | 3.70% |

| Apr 2031 | Jul 2031 | 3.75% |

| Jul 2031 | Oct 2031 | 3.80% |

Source: BlueGamma. Based on SOFR OIS curve construction.

The forward curve currently implies a gradual decline in three-month SOFR from approximately 3.64% today to a trough around 3.40% in late 2027, before rising steadily through the back end of the curve toward 3.80% by mid-2031. This shape has direct implications for cap pricing: caplets covering the near-term periods are more expensive because forward rates are higher and closer to typical strike levels.

When to Use an Interest Rate Cap

Interest rate caps are particularly well-suited to the following scenarios:

Floating-rate loan requirements

Many commercial real estate loans and acquisition facilities require the borrower to maintain a floating-rate hedge. Lenders frequently mandate interest rate caps as a condition of the loan agreement, particularly for bridge loans, construction loans, and transitional asset financing. In these cases, the borrower must purchase a cap with a strike rate and term that satisfy the lender's requirements.

Budget certainty with upside participation

Unlike an interest rate swap, which locks in a fixed rate, a cap allows the borrower to benefit from falling or stable rates while setting a ceiling on the worst-case scenario. This is particularly valuable when a borrower expects rates to remain stable or decline but wants protection against an adverse move.

Short-duration exposures

Caps are commonly used for exposures of one to three years, where the upfront premium is manageable relative to the protection provided. For longer-duration exposures, the premium can become significant, and a swap or collar may be more cost-effective.

Pre-sale or transitional assets

Borrowers holding assets they intend to sell or refinance within a defined window often prefer caps because they avoid the mark-to-market risk associated with unwinding a swap prior to maturity.

Interest Rate Cap Pricing: Live Example

The interest rate cap cost varies significantly based on the strike rate selected. The following table shows live pricing for a two-year SOFR cap on a $50 million notional, illustrating how the premium decreases as the strike moves further out of the money.

| Strike Rate | Premium ($) | Premium (bps) | Moneyness |

|---|---|---|---|

| 3.50% (near ATM) | $313,837 | 62.8 bps | Near the current forward rate (3.54%) |

| 4.00% | $86,927 | 17.4 bps | ~46 bps out of the money |

| 4.50% | $66,356 | 13.3 bps | ~96 bps out of the money |

| 5.00% | $63,507 | 12.7 bps | ~146 bps out of the money |

Source: BlueGamma live pricing. SOFR index, $50M notional, 3M frequency, SABR-calibrated volatility.

These prices were generated using the BlueGamma Cap Pricer, which provides indicative cap and floor pricing across tenors and strikes for any supported index. The same pricing is also available on BlueGamma for integration into internal models or automated workflows.

The relationship is non-linear. Moving from a 3.50% strike to 4.00% reduces the premium by over 72%, from $313,837 to $86,927. But moving from 4.00% to 5.00% only saves an additional $23,420. This reflects the option pricing dynamic: the first 50 basis points of out-of-the-money distance have a much larger impact on premium than subsequent moves.

For context, the current 2-year SOFR swap rate is 3.60%. A borrower choosing a cap at a 4.00% strike is paying $86,927 for the right to keep floating below 4.00% while being protected above it, rather than locking in at 3.60% via a swap.

How Term Affects Cap Premiums

Extending the cap's maturity increases the premium because longer caps contain more caplets, each carrying its own optionality value.

| Term | Premium ($) | Premium (bps) | Number of Caplets |

|---|---|---|---|

| 2 Years | $86,927 | 17.4 bps | 7 |

| 3 Years | $249,560 | 49.9 bps | 11 |

| 5 Years | $709,057 | 141.8 bps | 19 |

Source: BlueGamma live pricing. SOFR index, 4.00% strike, $50M notional.

A five-year cap at a 4.00% strike costs over eight times as much as a two-year cap at the same strike. This reflects not only the additional caplets but also the greater uncertainty over longer horizons, which increases implied volatility for the later-dated options.

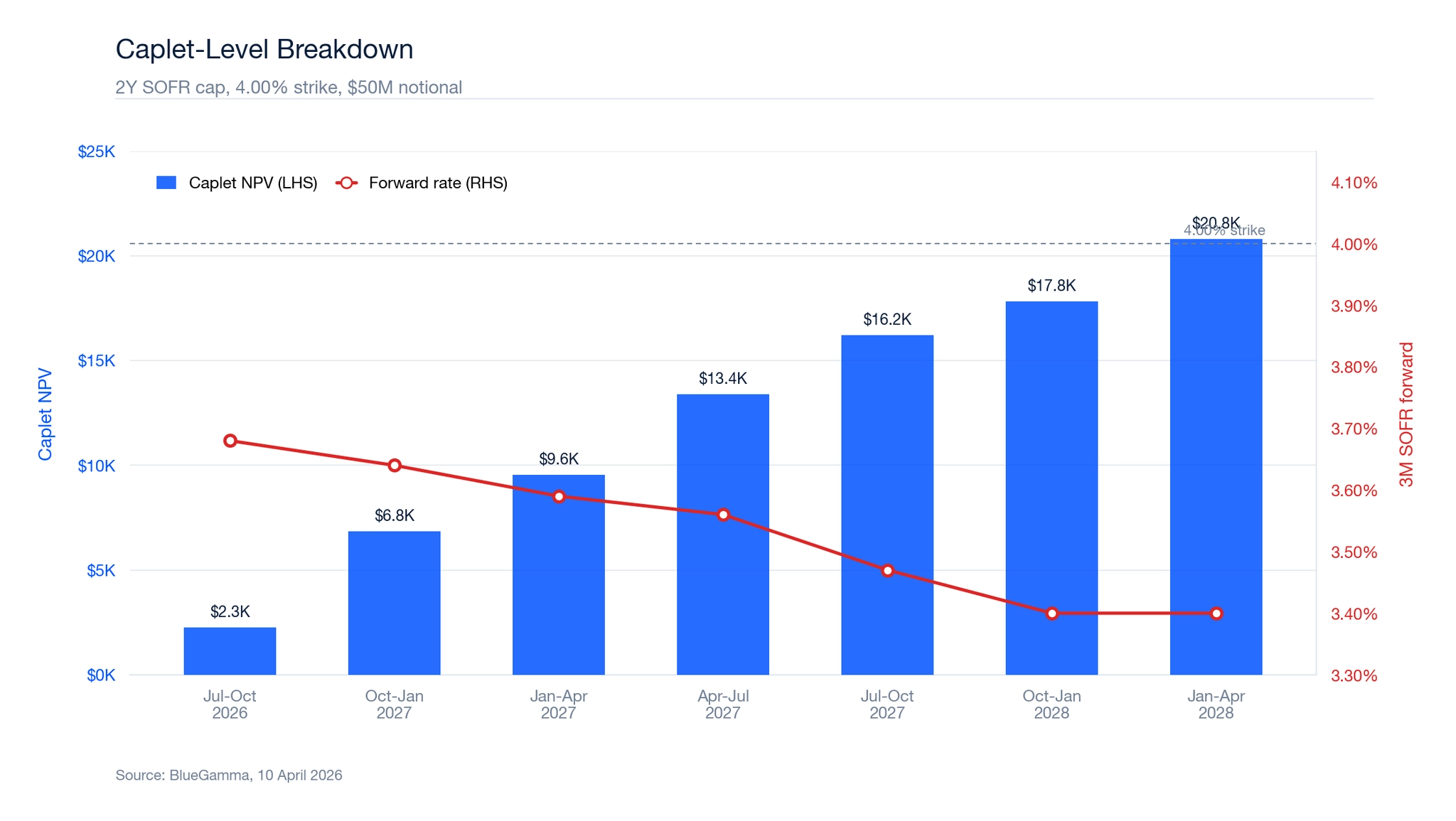

Caplet-Level Breakdown

One advantage of understanding cap pricing at the caplet level is the ability to see exactly where the cost is concentrated. The following breakdown shows the NPV contribution of each caplet in a 2-year SOFR cap struck at 4.00%:

| Caplet Period | Forward Rate | Vol (bps) | Caplet NPV |

|---|---|---|---|

| Jul - Oct 2026 | 3.68% | 56.5 | $2,263 |

| Oct 2026 - Jan 2027 | 3.64% | 62.6 | $6,843 |

| Jan - Apr 2027 | 3.59% | 66.2 | $9,553 |

| Apr - Jul 2027 | 3.56% | 69.1 | $13,401 |

| Jul - Oct 2027 | 3.47% | 73.0 | $16,227 |

| Oct 2027 - Jan 2028 | 3.40% | 76.6 | $17,827 |

| Jan - Apr 2028 | 3.40% | 76.6 | $20,814 |

Source: BlueGamma live pricing. SABR-calibrated normal volatilities.

Although the later caplets have lower forward rates (further from the 4.00% strike), they carry higher implied volatility and longer time to expiry, making them progressively more valuable. The final caplet contributes $20,814 to the total, nearly ten times the first caplet's $2,263.

Interest Rate Caps vs. Swaps

The choice between an interest rate cap and an interest rate swap depends on the borrower's risk tolerance, market outlook, and financing structure.

| Feature | Interest Rate Cap | Interest Rate Swap |

|---|---|---|

| Cost Structure | Upfront premium (e.g. $86,927 for 2Y at 4.00%) | No upfront cost (embedded in fixed rate of 3.60%) |

| Rate Protection | Ceiling only; borrower retains downside benefit | Fixed rate; no benefit from falling rates |

| Mark-to-Market Risk | Cap value can only be positive or zero for the buyer | Can be positive or negative; early termination may require a payment |

| Complexity | Simpler to unwind or let expire | Requires negotiation to terminate early |

| Best For | Short-term loans, transitional assets, lender requirements | Longer-term fixed-rate certainty |

Many borrowers also consider interest rate collars, which combine a purchased cap with a sold floor. The premium received from selling the floor offsets part or all of the cap premium, but the borrower gives up some benefit from falling rates. A zero-cost collar eliminates the upfront premium entirely but introduces a minimum rate.

Interest Rate Caps and Floors

An interest rate floor is the mirror image of a cap. While a cap protects against rising rates, a floor protects against falling rates. The floor buyer receives payments when the reference rate drops below the floor strike.

Floors are used primarily by lenders and fixed-income investors who want to ensure a minimum return on floating-rate assets. When combined with a cap, the two instruments form a collar that bounds the effective interest rate within a defined range.

The relationship between caps and floors is governed by put-call parity for interest rate options, which ensures consistent pricing between the instruments.

Valuing an Interest Rate Cap

Interest rate caps are valued using option pricing models. The standard approach applies the Black model (a variant of Black-Scholes adapted for interest rate instruments) to each individual caplet.

The key inputs to the valuation are:

- Forward rates for each reset period, derived from the relevant interest rate curve

- Implied volatility for each caplet, sourced from the swaption or cap volatility surface

- Discount factors from the relevant discount curve (typically an overnight rate curve such as SOFR OIS)

- Strike rate and day count convention

The value of the cap at any point in time is the sum of the present values of all remaining caplets. As market conditions change, the cap's mark-to-market value fluctuates accordingly. A cap purchased when rates were low will increase in value as rates rise, and vice versa.

Platforms such as BlueGamma provide real-time cap pricing and valuation through the web app, Excel add-in, and API, eliminating the need for manual model implementation. More sophisticated approaches, such as the SABR model used in the pricing examples above, account for the volatility smile, producing more accurate valuations across different strike levels. The SABR parameters calibrated from market data for the 2-year SOFR cap were rho = -0.75 and nu = 2.54, indicating a pronounced negative skew in the current volatility surface.

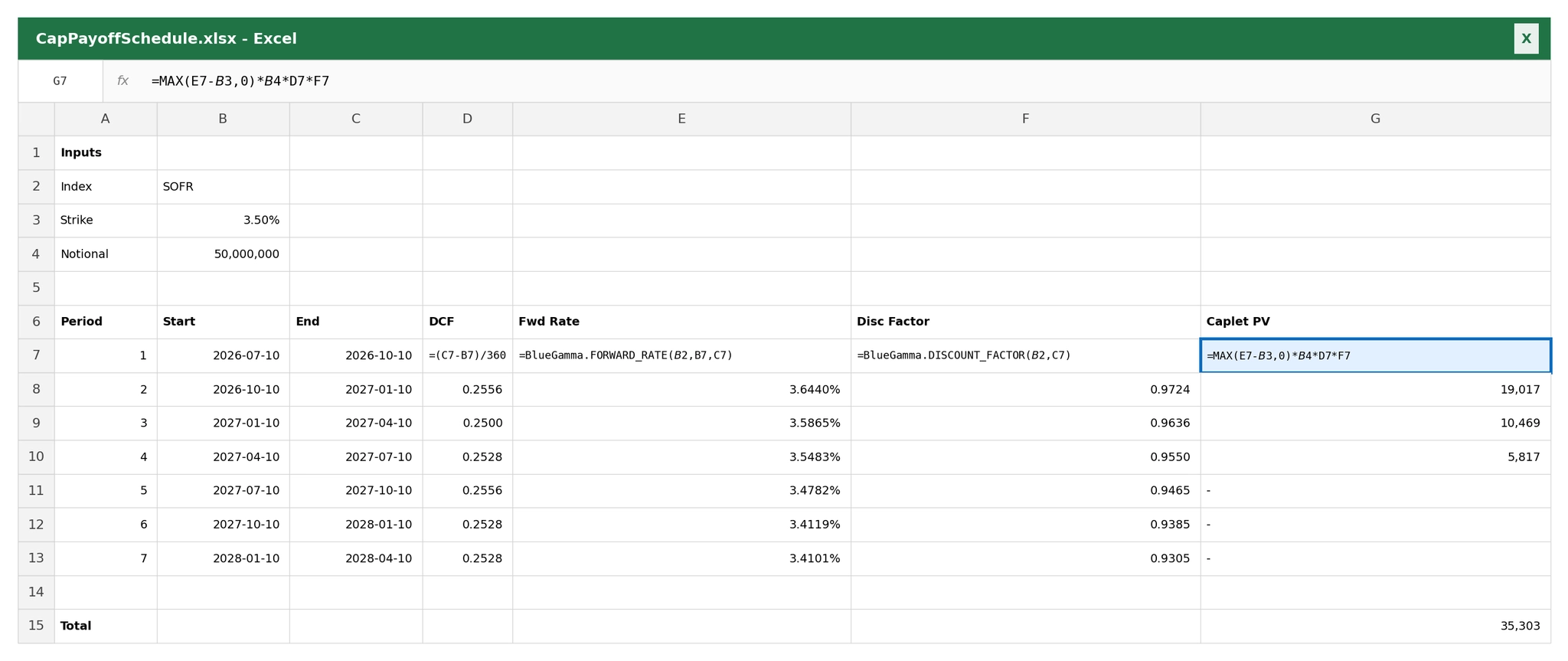

Building a Cap Payoff Schedule in Excel

For modelling cap payoffs period by period, the BlueGamma Excel add-in pulls live forward rates and discount factors directly into your spreadsheet.

This replicates the SABR-based pricing shown above to within a close approximation (ignoring the volatility component, which captures the optionality value for out-of-the-money strikes).

Accounting Treatment for Interest Rate Caps

Under both IFRS 9 and ASC 815, interest rate caps qualify for hedge accounting treatment, provided the required documentation and effectiveness testing criteria are met.

The cap premium can be accounted for in two ways:

Intrinsic value only, time value excluded as cost of hedging. Under IFRS 9, an entity may designate only the intrinsic value of the cap as the hedging instrument and exclude the time value as a "cost of hedging." Changes in intrinsic value flow through the hedging relationship (for a cash flow hedge of floating-rate debt, the effective portion is recognised in OCI). Changes in the excluded time value are deferred in OCI and accumulated in a separate component of equity, then reclassified to profit or loss either when the hedged transaction affects earnings (transaction-related hedges) or on a systematic basis over the hedge period (time-period-related hedges, which is typically the case for caps on interest payments).

Full fair value designation. Alternatively, the entire fair value change of the cap may be designated as the hedging instrument. Under a cash flow hedge of floating-rate interest, the effective portion of the cap's fair value change is recognised in OCI and recycled to profit or loss as the hedged interest payments affect earnings, while any ineffective portion is recognised in profit or loss immediately. This approach is simpler to document but can produce more P&L noise than designating intrinsic value only.

Proper hedge accounting treatment avoids unwanted profit-and-loss volatility from fair value changes in the cap. Borrowers should consult their auditors to confirm the appropriate treatment for their specific circumstances.

Key Considerations When Selecting an Interest Rate Cap

Before entering into an interest rate cap, borrowers should evaluate:

Strike rate selection. A lower strike provides more protection but costs more. As the pricing data above illustrates, moving from a 3.50% to 4.00% strike on a $50 million, 2-year cap reduces the premium from $313,837 to $86,927. The optimal strike balances the budget for the premium against the desired level of protection. Many lenders specify a maximum strike rate as part of their loan covenants.

Term alignment. The cap term should match the underlying loan maturity or the expected hold period. A cap that expires before the loan matures leaves the borrower exposed for the remaining period. As shown above, extending from 2 years to 5 years increases the cost from $86,927 to $709,057 at a 4.00% strike.

Counterparty selection. Caps are over-the-counter (OTC) instruments, meaning the buyer bears credit risk to the seller. Most borrowers purchase caps from investment-grade banks, and many lenders require that the cap counterparty meet specific credit rating thresholds.

Premium financing. Some lenders allow the cap premium to be financed as part of the loan, which preserves the borrower's cash reserves. This is common in commercial real estate transactions.

Extension and replacement. If the underlying loan is extended, the cap may need to be replaced or extended. Borrowers should plan for this eventuality and budget for the cost of a replacement cap, which will depend on prevailing market conditions at the time.

The Purchasing Process

For standard interest rate caps, the purchasing timeline is typically one to three business days from the point at which terms are agreed. The process begins with the borrower and cap dealer agreeing on the key economic terms: notional, strike rate, reference index, term, and payment frequency. Once terms are confirmed, the trade is documented under an ISDA Master Agreement between the buyer and the cap dealer, with a confirmation setting out the specific terms of the transaction. If no ISDA is in place, negotiating one can extend the timeline by several weeks. Borrowers should also anticipate know-your-customer (KYC) requirements, which the cap dealer must complete before executing the trade. In lender-mandated transactions, the cap dealer is often one of the lending banks, which can simplify both the documentation and the KYC process. The cap premium is typically payable on the trade date or settlement date.

Summary

An interest rate cap provides protection against rising interest rates while preserving the ability to benefit from favourable rate movements. The buyer pays an upfront premium in exchange for a series of caplets, each of which pays out if the reference rate exceeds the strike.

Based on market conditions, a 2-year SOFR cap on $50 million at a 4.00% strike costs approximately $86,927, compared to a swap rate of 3.60%. The premium reflects both the probability-weighted payout across seven quarterly caplets and the SABR-calibrated volatility surface.

Caps are widely used in commercial real estate, project finance, and acquisition financing, particularly where lenders require floating-rate hedging. The choice between a cap, swap, or collar depends on the borrower's risk profile, financing structure, and market outlook. For a broader comparison of instruments, see our guide to interest rate hedging strategies.

This article is for informational and educational purposes only and does not constitute financial, investment, legal, or tax advice. BlueGamma does not provide advisory services. Readers should consult qualified professional advisors before entering into any derivative transaction. Market data shown is indicative and sourced from BlueGamma as of the date stated.

Frequently Asked Questions

What is an interest rate cap?

An interest rate cap is a derivative contract that sets a maximum (ceiling) on a floating interest rate for a defined period. The buyer pays an upfront premium and receives compensation whenever the reference rate exceeds the agreed strike rate. Caps are widely used by borrowers with floating-rate loans to limit their exposure to rising interest rates.

How does an interest rate cap work?

At each reset date during the cap's term, the reference rate (such as SOFR or EURIBOR) is compared to the strike rate. If the reference rate exceeds the strike, the cap seller pays the buyer the difference, applied to the notional amount for that period. If the reference rate is at or below the strike, no payment is made and the borrower continues to benefit from the lower floating rate.

How much does an interest rate cap cost?

The cost depends on the strike rate, term, notional amount, reference index, and prevailing market volatility. As illustrated in the live pricing examples above, a 2-year SOFR cap on $50 million at a 4.00% strike currently costs approximately $86,927, while a near-at-the-money 3.50% strike costs $313,837. The interest rate cap cost decreases as the strike moves further out of the money.

How to account for an interest rate cap?

Under IFRS 9 and ASC 815, interest rate caps qualify for hedge accounting treatment when documentation and effectiveness testing requirements are met. The cap premium can be separated into intrinsic value and time value components, with intrinsic value changes recognised in other comprehensive income under a cash flow hedge designation. Borrowers should consult their auditors to confirm the appropriate treatment.

What is the difference between a cap and a swap?

An interest rate cap provides a ceiling on the floating rate while allowing the borrower to benefit from rates below the strike. An interest rate swap, by contrast, fixes the rate entirely, eliminating both upside and downside. Caps require an upfront premium but carry no mark-to-market risk for the buyer, whereas swaps have no upfront cost but can have a positive or negative mark-to-market value over their life.