If your business operates across borders, FX risk is unavoidable. The question isn't whether to manage it, but how.

Foreign exchange risk is one of the most significant financial exposures facing multinational corporations. A 10% move in a major currency pair can materially affect revenue, margins, and reported earnings. Yet many companies either under-hedge (leaving material exposure unmanaged) or hedge reactively without a structured framework.

This guide covers the three types of corporate FX exposure, the main hedging instruments, and a practical decision framework for treasury teams.

What is FX risk management?

FX risk management is the process of identifying, measuring, and mitigating the financial impact of exchange rate movements on a company's cash flows, earnings, and balance sheet. It encompasses defining which exposures to hedge, selecting appropriate instruments (forwards, options, cross-currency swaps), setting hedge ratios, and implementing a consistent policy framework.

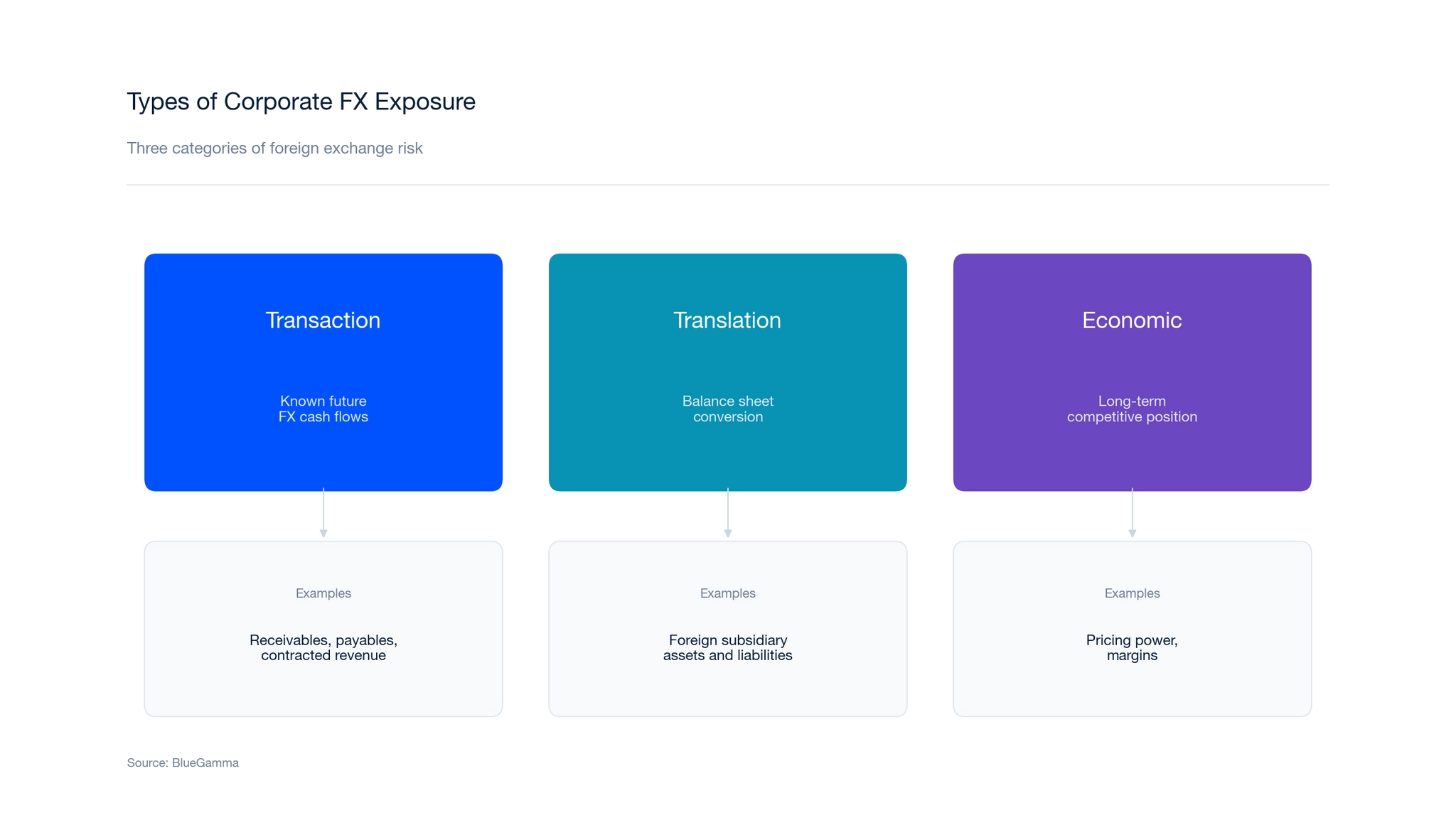

Types of Corporate FX Exposure

Transaction exposure

Arises from known or expected future cash flows in foreign currencies. This includes foreign-denominated receivables, payables, contracted revenue, intercompany loans, and planned capital expenditure.

Transaction exposure is the most directly hedgeable form of FX risk because the cash flows are specific, quantifiable, and have defined timing.

Example: A UK manufacturer sells products to the US and invoices in USD. A $5 million receivable due in 90 days is exposed to GBP/USD movements between the invoice date and the collection date.

Translation exposure

Arises when a company consolidates the financial statements of foreign subsidiaries into its reporting currency. Assets, liabilities, revenue, and expenses denominated in foreign currencies must be translated at the relevant exchange rates.

Translation exposure affects reported figures but does not involve a direct cash flow until the subsidiary is sold or liquidated. For this reason, many companies choose not to hedge translation exposure, though some do to reduce balance sheet and earnings volatility.

Economic exposure

The broadest form of FX risk, economic exposure reflects how exchange rate movements affect a company's long-term competitive position, pricing power, and profitability. This includes indirect effects such as a foreign competitor gaining a cost advantage from a weaker currency.

Economic exposure is difficult to quantify and hedge with financial instruments. It is typically managed through operational strategies such as geographic diversification of production, local-currency pricing, and natural hedging (matching revenues and costs in the same currency).

The P&L Impact of FX Movements

The FX impact on corporate earnings is one of the most frequently cited items in multinational earnings reports. When a company generates revenue or incurs costs in foreign currencies, exchange rate movements directly affect reported results in the functional currency.

Companies typically report both "as reported" results (at actual exchange rates) and "constant currency" results (translating foreign results at the prior period's exchange rates). The difference between the two is the FX impact. Analysts strip out FX impact to assess underlying business performance independent of currency movements.

The magnitude of FX impact can be substantial. A US company with EUR 10 million in European revenue would report $11.7M at EUR/USD 1.17 but only $10.9M if EUR weakened to 1.09, a $800K FX impact on revenue with no change in the underlying business. For companies with significant foreign revenue, aggregate FX impact can represent hundreds of millions of dollars in reported earnings variation.

FX impact flows through two channels in the income statement: transactional FX gains and losses (from settling foreign-currency receivables and payables at different rates than booked) and translational FX effects (from consolidating foreign subsidiary results). Foreign exchange risk management through hedging programmes can reduce transactional FX impact but does not eliminate translational effects unless net investment hedges are in place.

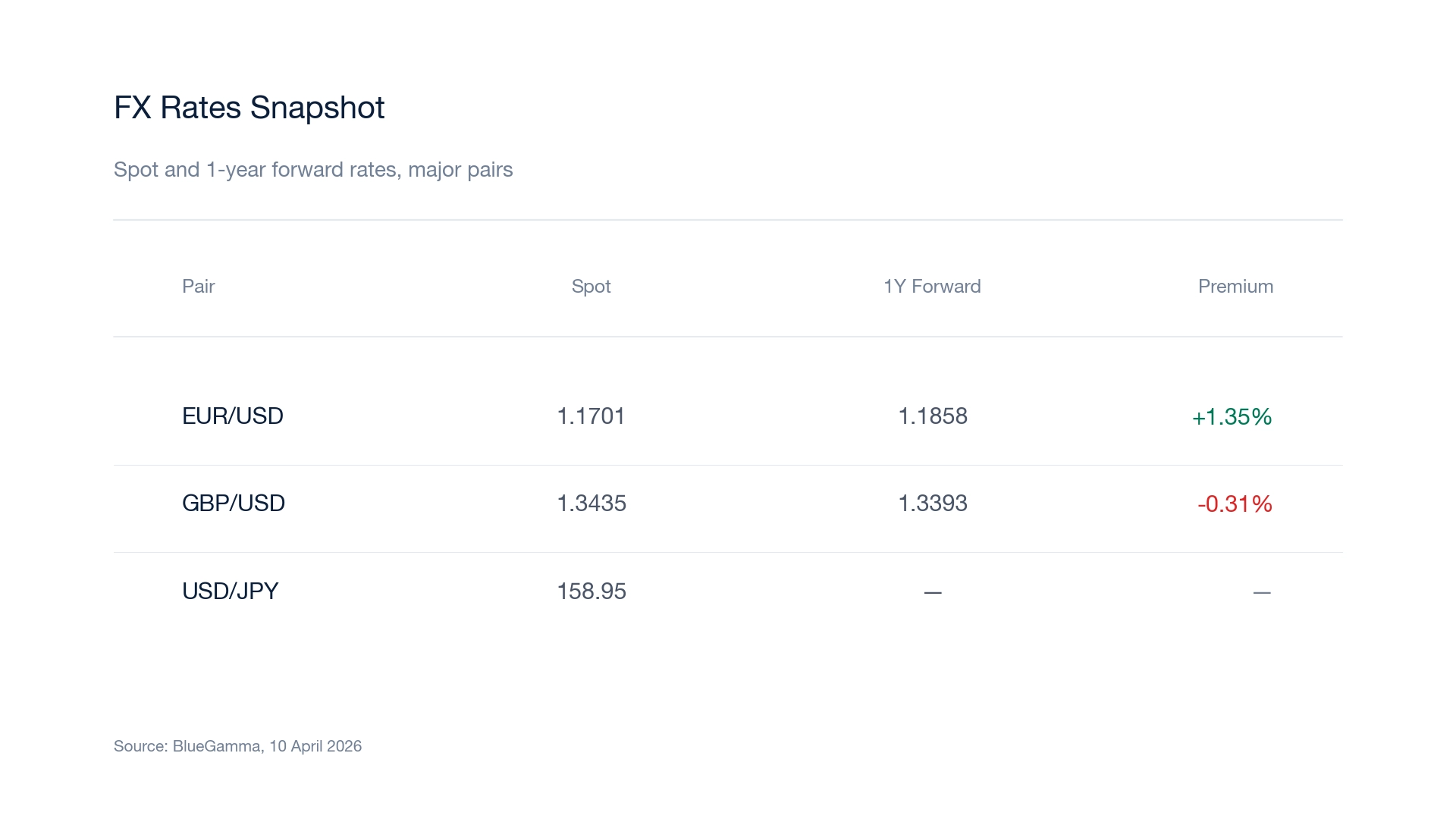

Current FX Market Snapshot

| Currency Pair | Spot Rate | 1Y Forward | Forward Premium/Discount |

|---|---|---|---|

| EUR/USD | 1.1701 | 1.1858 | +1.35% (EUR trades at forward premium) |

| GBP/USD | 1.3435 | 1.3393 | -0.31% (GBP trades at forward discount) |

| USD/JPY | 158.95 | - | - |

Source: BlueGamma.

BlueGamma's Foreign Exchange module provides live spot rates, forward rates, and forward curves for 100+ currency pairs, available through the web app, Excel add-in, and API.

The forward premium or discount reflects the interest rate differential between the two currencies. EUR trades at a forward premium to USD because EUR interest rates (EURIBOR ~2.63%) are lower than USD rates (SOFR ~3.70%). This means a European company hedging USD receivables with a forward contract will receive a slightly better rate than spot.

FX Hedging Instruments

FX Forwards

An FX forward locks in an exchange rate for a future date. The forward rate incorporates the interest rate differential between the two currencies.

Best for: Known, specific cash flows with defined timing. Receivables, payables, dividend repatriation.

Advantages: No upfront cost. Simple to execute. Customisable to any amount and date.

Disadvantages: No benefit from favourable rate movements. Early termination may involve a cost.

Example: The UK manufacturer can lock in a GBP/USD rate of 1.3393 for the $5 million receivable due in one year, guaranteeing GBP 3,732,302 regardless of where spot moves.

Forward rates for any currency pair and settlement date are available on BlueGamma in real time.

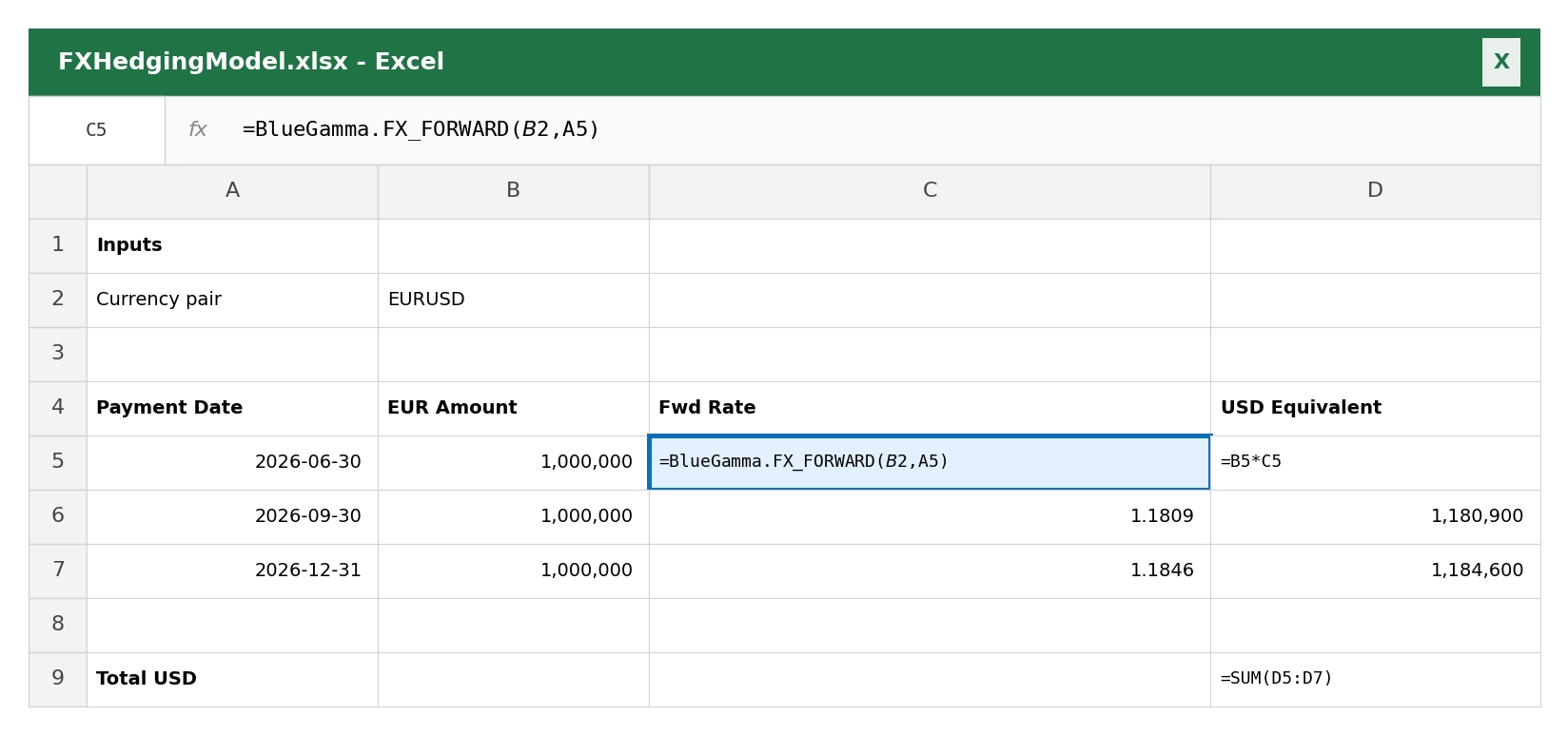

Building an FX Hedging Model in Excel

For treasury teams building FX forecasts and hedging models, the BlueGamma Excel add-in provides live spot and forward rates so you can project the USD value of future EUR cash flows using the market's current forward curve.

FX Options

An FX option gives the buyer the right, but not the obligation, to exchange currencies at a specified rate (the strike) on a future date.

Best for: Exposures where the timing or amount is uncertain. Competitive bids in foreign currencies. Protection with upside participation.

Advantages: Preserves benefit from favourable rate movements. Flexible strike selection.

Disadvantages: Requires an upfront premium. More complex than forwards.

FX Collars

An FX collar combines a purchased option (protection) with a sold option (to offset the premium). The result is a bounded range within which the effective exchange rate will fall.

Best for: Reducing or eliminating the option premium while accepting a limited range.

Cross-Currency Swaps

For long-dated FX exposures (typically over two years), cross-currency swaps provide hedging of both principal and interest cash flows across currencies.

Best for: Foreign-currency debt, subsidiary funding, long-dated project finance.

For a detailed treatment, see our cross-currency swaps guide.

Natural Hedging

Matching revenues and costs in the same currency eliminates the need for financial hedging. This can involve sourcing materials locally, invoicing in the functional currency, or locating production facilities in key markets.

Best for: Structural, long-term reduction of FX exposure.

Currency Hedging Strategies

Beyond the choice of instrument, the structure of a forex risk management programme determines its effectiveness. Four main currency hedging strategies are used by corporate treasury teams.

Layered hedging involves hedging increasing percentages of forecast cash flows as they become more certain. A company might hedge 25% of exposure at 12 months, 50% at 6 months, and 75-100% at 3 months. This approach reduces the risk of over-hedging uncertain exposures while progressively locking in rates as cash flows firm up.

Rolling hedging maintains a constant hedge horizon regardless of the budget cycle. For example, a company might always maintain 12 months of forward cover, rolling maturing contracts and adding new ones each month. This produces a blended average rate that smooths FX impact over time.

Budget rate hedging locks in the exchange rate used in the annual budget at the start of the fiscal year, typically through a single tranche of forwards or options. This provides certainty that reported results will match the budget, simplifying financial planning and performance measurement.

Dynamic hedging adjusts hedge ratios based on changes in exposure, market conditions, or predefined triggers. For example, a company might increase its hedge ratio when volatility rises or when rates breach a threshold. Dynamic currency risk management requires more active monitoring but can be more capital-efficient.

The choice among these strategies depends on the predictability of cash flows, the company's risk tolerance, and the resources available for ongoing management.

Choosing the Right Instrument

| Exposure Type | Timing | Certainty | Recommended Instrument |

|---|---|---|---|

| Receivable / payable | Known date | Certain amount | FX forward |

| Forecast revenue | Approximate | Probable but uncertain | FX option or layered forwards |

| Competitive bid | Known | Contingent on winning | FX option |

| Foreign-currency debt | Multi-year | Certain | Cross-currency swap |

| Dividend repatriation | Periodic | Probable | Rolling FX forwards |

| Net investment in subsidiary | Ongoing | Structural | FX forward / cross-currency swap / foreign-currency borrowing |

Building an FX Hedging Policy

A structured FX hedging policy provides consistency and removes ad hoc decision-making. Key components include:

Exposure identification. Define which exposures are hedged (transaction, translation, economic) and which are not. Most policies focus on transaction exposure.

Hedge ratios. Specify the percentage of forecast exposure to hedge, typically on a rolling basis. A common approach is to hedge 75-100% of committed exposures and 25-50% of forecast exposures.

Tenor limits. Define the maximum hedge horizon. Most corporate policies hedge 6-24 months of transaction exposure, with longer tenors for debt-related hedging.

Instrument selection. Specify which instruments are permitted. Many policies limit hedging to vanilla forwards and options, prohibiting speculative or leveraged structures.

Benchmark rates. Define the reference rates used for internal transfer pricing and performance measurement. This avoids confusion between budget rates, spot rates, and hedge rates.

Governance. Establish approval authorities, reporting requirements, and escalation procedures for exceptions.

Common FX Hedging Mistakes

Hedging selectively based on a market view. Skipping hedges when the rate looks favourable and hedging only when it looks unfavourable introduces speculative risk. A systematic policy produces more consistent outcomes.

Over-hedging uncertain exposures. Hedging 100% of forecast revenue that may not materialise creates a speculative position if the revenue falls short. Graduated hedge ratios (lower for less certain exposures) mitigate this risk.

Ignoring the cost of carry. The forward rate includes the interest rate differential. Hedging into a high-interest-rate currency from a low-interest-rate currency involves a carry cost that should be factored into the economics.

Treating FX hedging as a profit centre. The purpose of hedging is to reduce uncertainty, not to generate returns. Measuring hedge "performance" against spot encourages speculative behaviour.

Summary

Corporate FX risk management requires identifying the types of exposure (transaction, translation, economic), selecting appropriate instruments, and implementing a consistent hedging policy.

With EUR/USD at 1.1701, GBP/USD at 1.3435, and USD/JPY at 158.95 (9 April 2026), exchange rate volatility remains a material risk for multinational corporations. FX forwards are the workhorse instrument for most transaction hedging, while cross-currency swaps serve longer-dated debt exposures. A structured hedging policy ensures consistency and removes the temptation to speculate.

This article is for informational and educational purposes only and does not constitute financial, investment, legal, or tax advice. BlueGamma does not provide advisory services. Readers should consult qualified professional advisors before entering into any derivative transaction. Market data shown is indicative and sourced from BlueGamma as of the date stated.

Frequently Asked Questions

How do you hedge foreign exchange risk?

The most common approach is to use FX forward contracts to lock in exchange rates for known future cash flows such as receivables, payables, and intercompany settlements. For uncertain or contingent exposures, FX options provide protection while preserving upside. Cross-currency swaps are used for long-dated debt exposures. The choice of instrument depends on the certainty, timing, and size of the exposure.

What is the best way to manage currency risk?

The most effective approach to currency risk management combines a formal hedging policy with systematic execution. This means defining which exposures to hedge, setting minimum hedge ratios, using layered or rolling hedging programmes rather than ad hoc decisions, and separating the hedging function from speculative views on exchange rates. Consistency over time produces better outcomes than attempting to time the market.

What is the difference between transaction and translation exposure?

Transaction exposure arises from known or expected future cash flows in foreign currencies (such as receivables, payables, or contracted revenue) and results in realised FX gains or losses when settled. Translation exposure arises from converting a foreign subsidiary's financial statements into the parent company's reporting currency and affects reported figures without a direct cash flow impact. Transaction exposure is typically hedged with forwards or options; translation exposure is often left unhedged or managed through net investment hedges.