What is a Forward Rate Agreement (FRA)?

A Forward Rate Agreement (FRA) is an over-the-counter (OTC) derivative contract between two parties that locks in an interest rate for a future period. It is an agreement to exchange the difference between a predetermined fixed interest rate (the FRA rate) and the market interest rate on a future date, based on a notional principal amount. The principal is not exchanged, only the interest rate differential. This makes FRAs a popular tool for companies looking to hedge against or speculate on future interest rate movements.

How Does a Forward Rate Agreement Work?

A FRA works by allowing two parties, a "buyer" and a "seller," to agree on a future interest rate. The buyer of the FRA locks in a borrowing rate, while the seller locks in a lending rate. At the contract's settlement date, the payment is calculated based on the difference between the agreed-upon FRA rate and the prevailing market reference rate. If the reference rate is higher than the FRA rate, the seller pays the difference to the buyer. Conversely, if the reference rate is lower, the buyer pays the seller.

What are Forward Rate Agreements used for?

The primary use of Forward Rate Agreements is to hedge against interest rate risk. For example, a company that plans to borrow money in the future can buy a FRA to protect itself from a potential rise in interest rates. Conversely, an investor who wants to protect the return on a future investment can sell an FRA to hedge against a fall in rates. FRAs are also used by speculators who have a view on the future direction of interest rates.

Key Parties and Terminology in a FRA

- Buyer: The party that agrees to pay a fixed rate and receive a floating rate. The buyer profits if interest rates rise.

- Seller: The party that agrees to receive a fixed rate and pay a floating rate. The seller profits if interest rates fall.

- Notional Principal: The hypothetical principal amount on which the interest payments are calculated. This amount is not exchanged between the parties.

- Contract Rate (FRA Rate): The fixed interest rate agreed upon at the start of the contract.

- Reference Rate: A benchmark interest rate, such as SOFR or Euribor, that is used to determine the settlement payment.

The Forward Rate Agreement (FRA) Formula

The payment on a Forward Rate Agreement is calculated using the following formula:

Payment = [(Reference Rate - FRA Rate) * Notional Principal * (Days in Contract Period / 360 or 365)] / [1 + Reference Rate * (Days in Contract Period / 360 or 365)]

Forward Rate Agreement Calculation Example

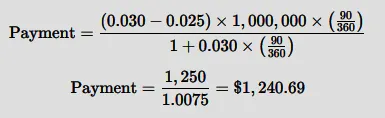

Imagine a company enters into a 3x6 FRA. This means the contract settles in three months, and the interest rate applies to a three-month period.

- Notional Principal: $1 million

- FRA Rate: 2.5%

- Reference Rate at settlement (e.g., 3-month Term SOFR): 3.0%

- Days in Contract Period: 90

Since the Reference Rate (3.0%) at settlement is higher than the agreed-upon FRA Rate (2.5%), the seller pays the difference to the buyer. The calculation is as follows:

Step 1: Calculate the interest differential.

(0.030 - 0.025) * $1,000,000 * (90/360) = $1,250

Step 2: Calculate the discount factor.

1 + (0.030 * 90/360) = 1.0075

Step 3: Calculate the final payment by discounting the interest differential.

Payment = 1,250/1.0075= 1,240.69

The buyer receives a payment of $1,240.69 from the seller. The payment is discounted because, unlike a loan, the settlement occurs at the start of the interest period, not the end.

How to Value a Forward Rate Agreement

Before maturity, the value of a FRA is the present value of the expected future settlement payment. The value of the contract changes as market interest rates fluctuate. If interest rates move in favour of one party (e.g., rates rise for the buyer), the value of their position becomes positive. The value is calculated by comparing the original FRA rate to the new FRA rate for the remaining term and discounting the difference.

The Post-LIBOR Transition: Why the USD FRA Market Vanished

For decades, the London Interbank Offered Rate (LIBOR) was the primary benchmark for FRAs. The global transition to new Risk-Free Rates (RFRs) like the Secured Overnight Financing Rate (SOFR) in the United States fundamentally reshaped the market.

While the transition was happening, FRA trading initially surged as firms hedged their final LIBOR exposures. However, afterward, the USD-denominated FRA market collapsed. Instead of creating a new FRA market based on SOFR, participants migrated their hedging activities to more efficient, exchange-traded instruments.

The primary substitutes for USD LIBOR FRAs are now:

- SOFR Futures Contracts: The vast majority of short-term hedging moved to highly liquid SOFR futures contracts traded on exchanges like the CME.

- Overnight Index Swaps (OIS): Many users also shifted to SOFR-based OIS, where a fixed rate is swapped for the compounded average of the SOFR overnight rate.

This shift occurred because the market chose instruments with distinct advantages over OTC FRAs, including higher liquidity, standardisation, and the elimination of bilateral counterparty risk through central clearing.

In stark contrast, the euro-denominated FRA market, based on the reformed Euribor, has endured. It now accounts for almost all global FRA activity.

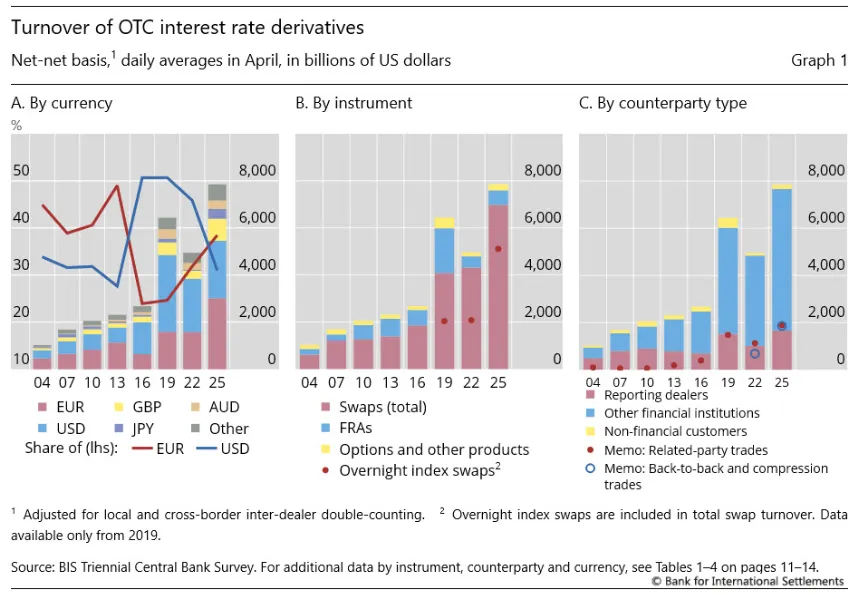

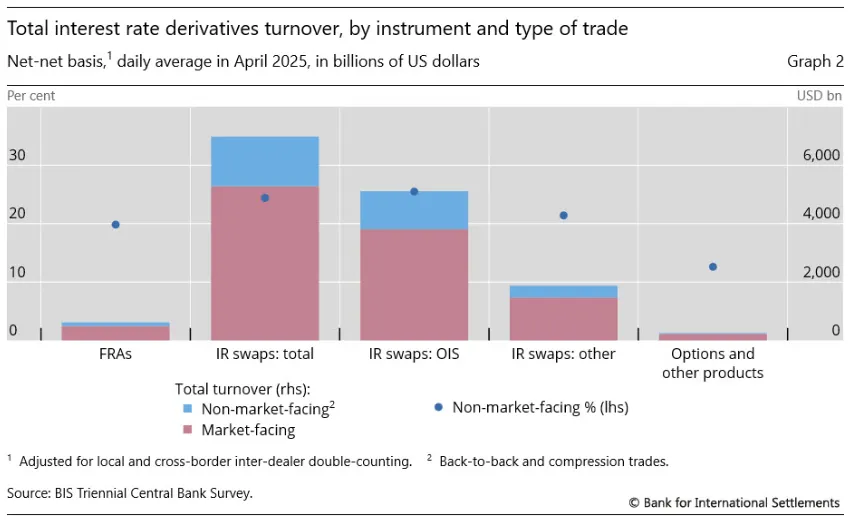

A 2025 BIS report highlighted that the overall FRA market saw a daily turnover of $617 billion in April 2025, a rebound driven almost entirely by euro-denominated contracts. According to the report, the OIS market grew to a massive daily turnover of $5.1 trillion in April 2025. While according to the CME, the SOFR Futures & Options market is estimated to have an average daily turnover of approximately $6 trillion in notional value, making it one of the deepest futures markets in the world in terms of liquidity.

This has left the global FRA landscape as a niche but important market, almost exclusively centred on the euro.

Check out our Risk-Free Rate Calculator

Forward Rate Agreement Vs STIR Futures Vs Interest Rate Swaps

It's crucial to understand that FRAs, Futures, and Swaps are types of financial products or contracts. They are not the benchmark rates themselves. All three of these products have transitioned to use new RFRs like SOFR as their underlying benchmark rate, replacing LIBOR.

The key differences between them explain why the market chose futures over FRAs for short-term USD hedging:

| Feature | Forward Rate Agreement (FRA) | Short-Term Interest Rate (STIR) Futures | Interest Rate Swap (IRS) |

|---|---|---|---|

| Trading Venue | Over-the-counter (OTC) | Exchange-traded | Over-the-counter (OTC) |

| Standardization | Customized contracts | Standardized contracts | Customized contracts |

| Counterparty Risk | Present (bilateral) | Mitigated by a clearinghouse | Present (bilateral) |

| Structure | Single future period | Multiple standardized periods | Series of payments over a longer term |

| Primary Advantage | Flexibility and customization | High liquidity, no counterparty risk | Long-term, strategic hedging |

Advantages of FRAs

- Customization: FRAs can be tailored to the specific notional amount and contract period a user needs.

- Hedging Precision: Allows for precise hedging of a specific future loan or investment period.

- Budget Certainty: Locks in a future interest rate, aiding in financial planning.

Disadvantages of FRAs

- Counterparty Risk: As an OTC product, there is a risk that the other party may default on its obligation.

- Low Liquidity: The bespoke nature of FRAs makes them illiquid and difficult to exit compared to exchange-traded instruments.

- Opportunity Cost: If interest rates move in a favourable direction, the party that hedged will not benefit from the better rate.