By Ahmed Babikir and Ali Vohra. Originally published 20 June 2023.

1. Introduction

Given how intertwined global financial markets have become, understanding the mechanics of cross currency swaps has become quite important. A cross-currency swap (also known as an xccy swap) is a derivative contract in which two parties exchange interest payments and principal amounts denominated in different currencies. These instruments are central to international finance, enabling corporations, financial institutions, and investors to manage foreign exchange risk, access cheaper funding in foreign markets, and hedge multi-currency balance sheet exposures.

According to the Bank for International Settlements, the notional amount of outstanding OTC foreign exchange derivatives stood at approximately $155 trillion at end-June 2025. FX swaps and outright forwards make up the largest share of this market, while cross-currency swaps remain a smaller but material segment used primarily for long-dated hedging.

This guide covers how cross-currency swaps work, the three main types, how they are priced in five steps, and when they make sense for corporate treasury teams. If you are new to the mechanics of vanilla interest rate swaps, start with our guide to interest rate swaps before continuing.

2. Understanding Cross-Currency Swaps

A cross-currency swap involves three stages of cash flows between the two counterparties:

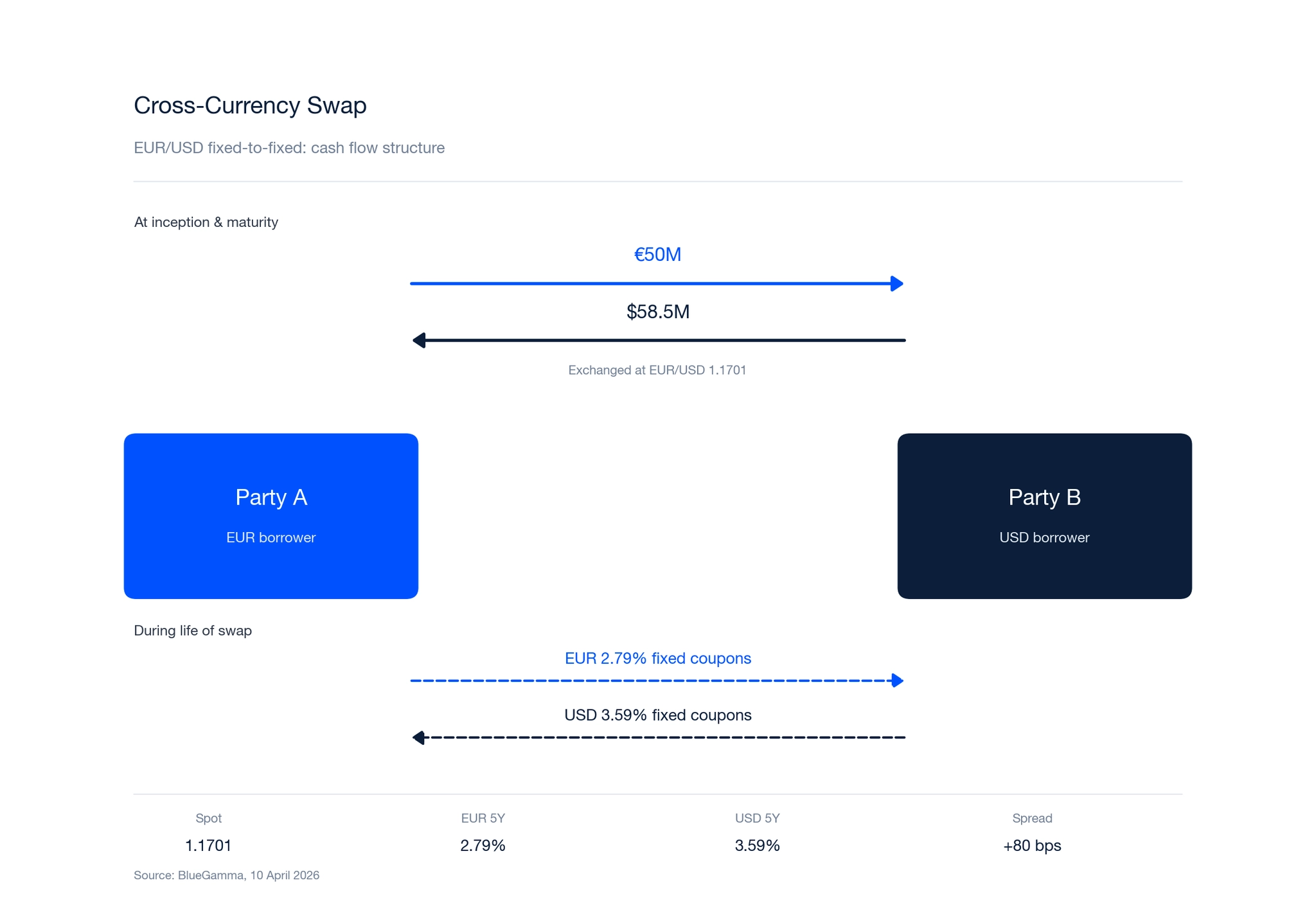

1. Initial exchange of principal. At inception, the two parties exchange principal amounts in their respective currencies at the prevailing spot exchange rate. For example, with EUR/USD at 1.1701, a EUR 50 million principal corresponds to approximately USD 58.5 million.

2. Periodic interest payments. During the life of the swap, each party makes interest payments to the other in the currency they received. These payments can be fixed or floating, depending on the swap structure.

3. Re-exchange of principal at maturity. At the end of the swap, the original principal amounts are exchanged back at the same exchange rate used at inception, regardless of where the spot rate has moved in the meantime.

This final feature is critical: it is the re-exchange of principal at the original rate that provides the foreign exchange hedge. The borrower knows exactly how much they will pay or receive in their home currency at maturity.

3. Types of Cross-Currency Swaps

Cross-currency swaps come in three primary structures, each suited to different hedging and funding objectives.

Fixed-to-Fixed Rate Cross-Currency Swaps

Both parties pay fixed interest rates in their respective currencies. This is the simplest structure and is commonly used when a corporate wants to convert fixed-rate debt from one currency to another.

Using current market rates, a 5-year fixed-to-fixed EUR/USD cross-currency swap would involve Party A paying approximately 2.79% fixed in EUR (the 5-year EURIBOR swap rate) and Party B paying approximately 3.59% fixed in USD (the 5-year SOFR swap rate), plus or minus the cross-currency basis.

Floating-to-Floating Rate Cross-Currency Swaps

Both parties pay floating rates, typically referencing overnight or term rates in their respective currencies. The floating-to-floating structure is often called a cross-currency basis swap. One leg typically includes a spread over the reference rate (the cross-currency basis) to account for the relative supply and demand for borrowing in each currency.

For example, a EUR/USD basis swap might involve one party paying SOFR flat and receiving ESTR (the euro short-term rate) plus or minus a basis spread. Prior to the transition from IBOR rates, the equivalent structure referenced USD LIBOR against EURIBOR.

Fixed-to-Floating Rate Cross-Currency Swaps

One party pays a fixed rate in one currency while the other pays a floating rate in the other currency. This structure is used when one party has fixed-rate funding and wants exposure to floating rates in another currency, or vice versa.

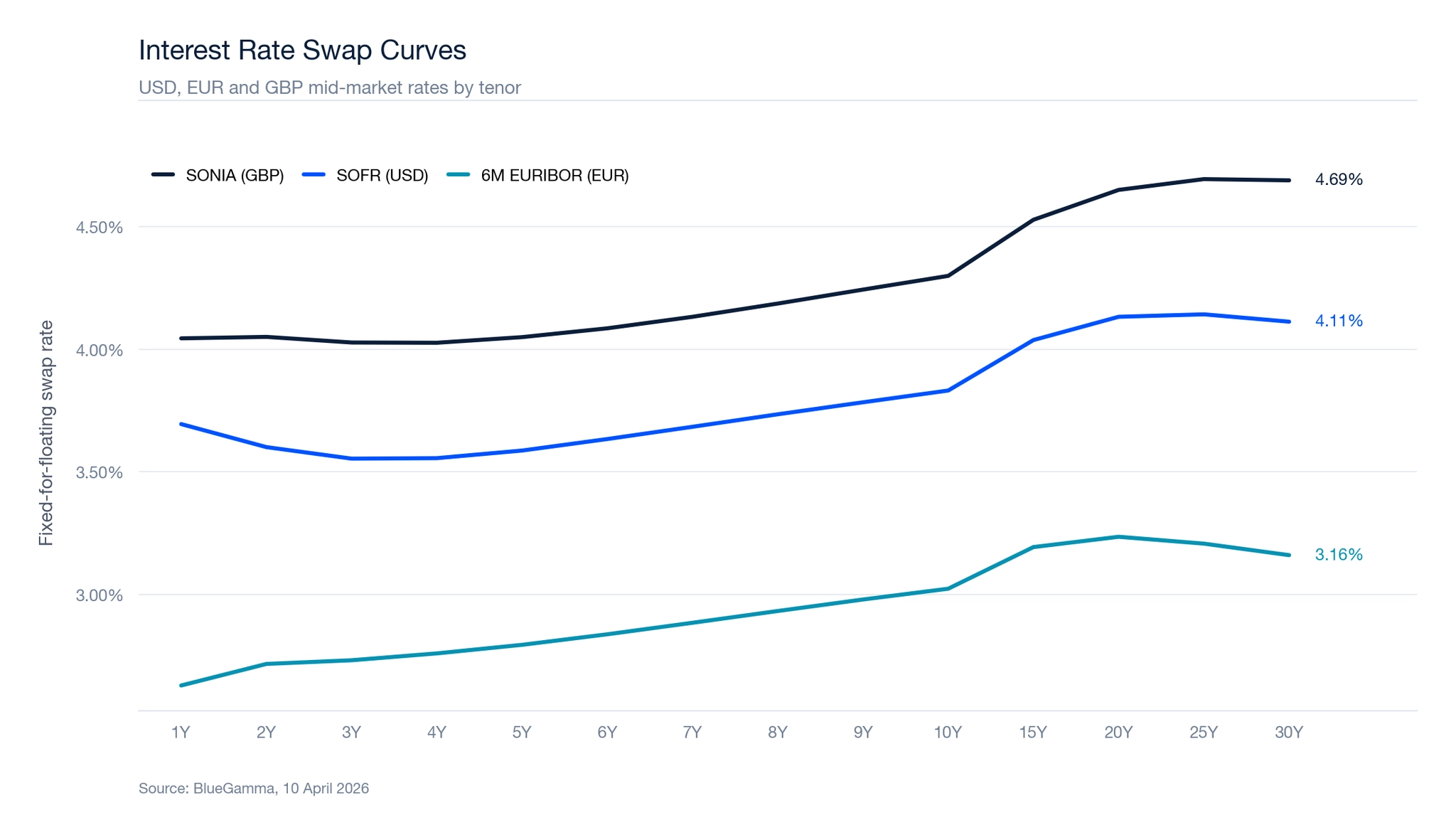

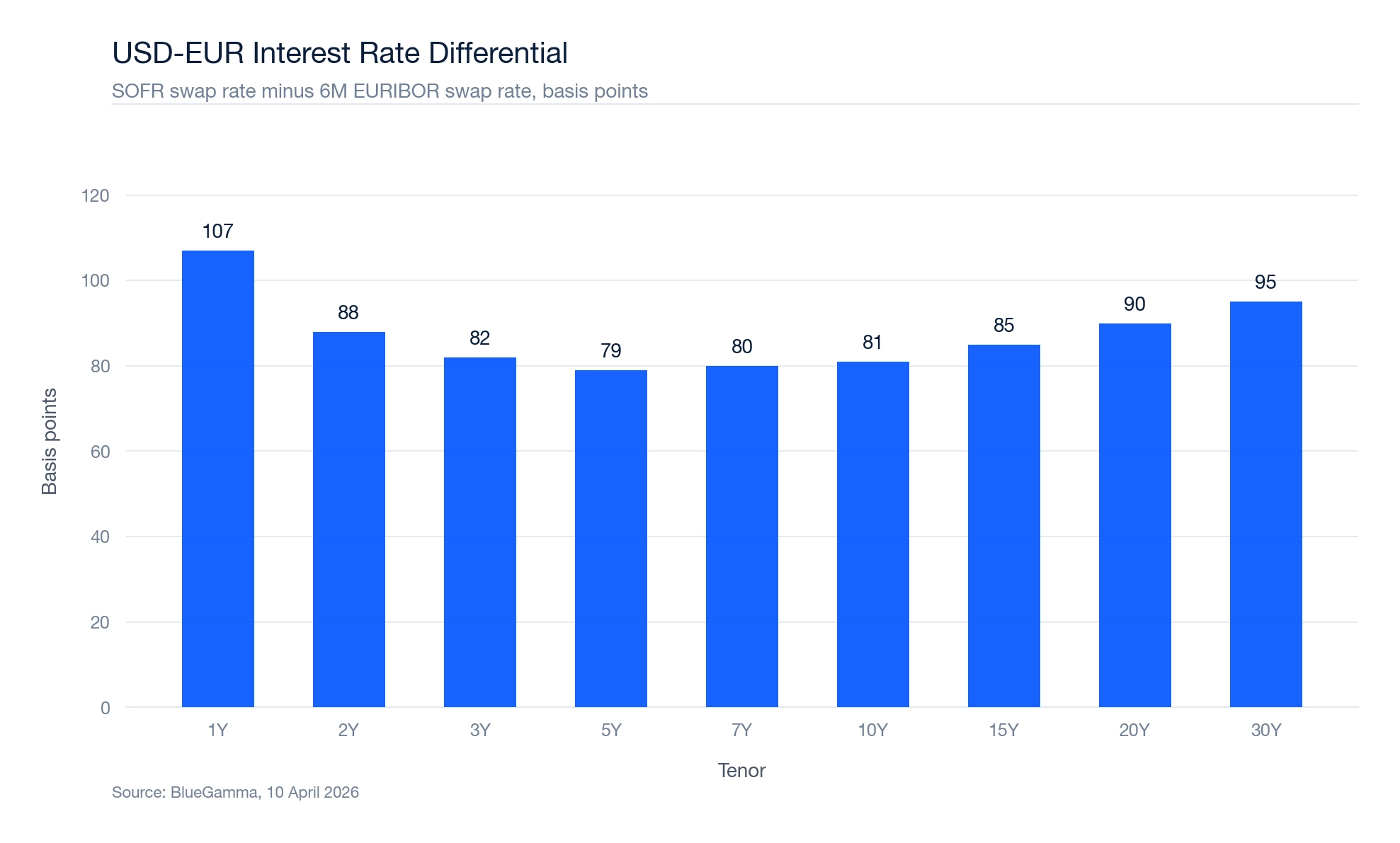

4. The Interest Rate Differential: Why Cross-Currency Swaps Exist

The economic rationale for cross-currency swaps stems from differences in interest rate levels across currencies. A company that can borrow cheaply in its home currency may use a cross-currency swap to synthetically convert that borrowing into a foreign currency, often at a lower all-in cost than borrowing directly in the foreign market.

| Tenor | SOFR (USD) | 6M EURIBOR (EUR) | SONIA (GBP) | USD-EUR Spread |

|---|---|---|---|---|

| 1Y | 3.70% | 2.63% | 4.04% | 107 bps |

| 2Y | 3.60% | 2.72% | 4.05% | 89 bps |

| 5Y | 3.59% | 2.79% | 4.05% | 79 bps |

| 10Y | 3.83% | 3.02% | 4.30% | 81 bps |

| 20Y | 4.13% | 3.23% | 4.65% | 90 bps |

| 30Y | 4.11% | 3.16% | 4.69% | 95 bps |

Source: BlueGamma, 9 April 2026.

These swap curves are available in real time on the BlueGamma platform, updated continuously throughout the trading day. Treasury teams can price structures directly in our cross-currency swap pricer or pull matching FX forward rates for short-dated hedges.

As of 9 April 2026, the USD-EUR interest rate differential ranges from approximately 79 to 107 basis points across the curve. This differential is a key driver of cross-currency swap pricing: a European corporate borrowing in EUR and swapping into USD will pay a higher interest rate on the USD leg, reflecting the higher prevailing rates in the United States.

5. How to Price a Cross-Currency Swap

Pricing a cross-currency swap involves five key steps.

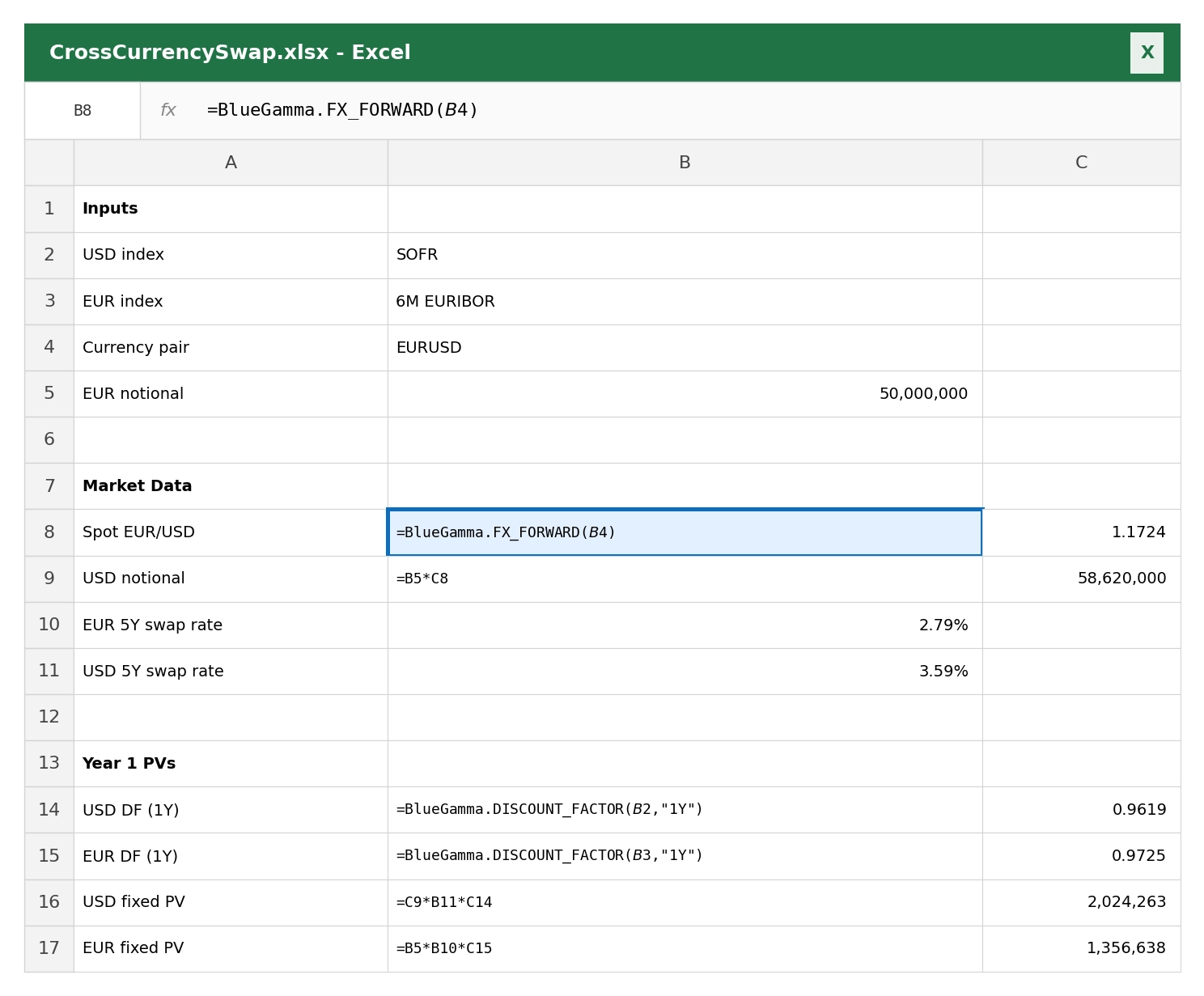

Step 1: Determine the principal amounts in each currency

Convert the notional amount at the current spot exchange rate. With EUR/USD at 1.1701, a EUR 50 million swap corresponds to USD 58,505,000. These principal amounts are exchanged at inception and re-exchanged at maturity at this same rate.

Step 2: Calculate the periodic interest payments

The fixed rate on each currency leg is derived from the respective interest rate swap curve. For a 5-year EUR/USD cross-currency swap:

- EUR fixed leg: 2.79% (5-year 6M EURIBOR swap rate)

- USD fixed leg: 3.59% (5-year SOFR swap rate)

Periodic coupons are calculated by applying these rates to the respective principal amounts on the agreed payment frequency (typically semi-annual or annual).

Step 3: Consider the basis adjustment

The cross-currency basis reflects the supply-demand imbalance for borrowing in each currency via swap markets. A negative basis on the EUR leg means the EUR payer receives slightly less than the standard swap rate, or the USD payer pays slightly less. The basis is additive to one of the legs and must be incorporated before computing present values.

Step 4: Calculate the present value of future cash flows

Each leg's future cash flows (both interest and principal) are discounted using the appropriate discount curve for that currency:

- USD cash flows are discounted using the SOFR OIS curve

- EUR cash flows are discounted using the ESTR OIS curve

The NPV of each leg is then converted to a common currency using the spot rate.

Step 5: The price of the swap is the net present value of all future cash flows

The fair cross-currency swap rate is the rate on one leg (typically the foreign currency leg) that makes the NPV of both legs equal at inception. At fair value, the swap has zero cost to enter, and any subsequent change in rates, FX, or basis drives the swap's mark-to-market value. You can run this calculation live in the BlueGamma cross-currency swap pricer.

Building a Cross-Currency Swap in Excel

Treasury teams can model cross-currency swap cash flows directly in Excel using the BlueGamma add-in, which provides live forward rates and discount factors for each currency.

Using forward rates from the add-in, you can value each leg of the swap and compute the net present value of the overall structure.

6. Worked Example: EUR 50M Cross-Currency Swap

Consider a European manufacturing company that has issued a EUR 50 million bond at a fixed rate of 3.00% but needs USD funding for a U.S. acquisition. Rather than issuing new USD debt, the company enters a 5-year fixed-to-fixed cross-currency swap.

| Parameter | Value |

|---|---|

| Notional | EUR 50,000,000 |

| Direction | Company receives EUR fixed, pays USD fixed |

| EUR Fixed Rate | 2.79% |

| USD Fixed Rate | 3.59% |

| Frequency | Annual |

| Spot Rate at Inception | EUR/USD 1.1701 |

At inception: The company delivers EUR 50M to the counterparty and receives USD 58.5M. The company uses the USD to fund the acquisition.

During the swap (annually): The company pays USD 2.10M in fixed interest (3.59% on USD 58.5M) and receives EUR 1.40M in fixed interest (2.79% on EUR 50M). The EUR received offsets the company's EUR bond coupon payments.

At maturity: The company returns USD 58.5M and receives EUR 50M back, at the original exchange rate of 1.1701, regardless of where EUR/USD has moved. The company uses the EUR 50M to repay the maturing bond.

The result is that the company has effectively converted its EUR fixed-rate debt into USD fixed-rate debt at a known cost, fully hedging the FX risk on both the principal and the interest flows.

7. When Corporates Use Cross-Currency Swaps

Accessing cheaper foreign currency funding

A corporation with strong credit in its home market may find it cheaper to borrow domestically and swap into the foreign currency rather than issuing directly in the foreign debt market. This is particularly relevant for corporates with strong domestic bond programmes but limited access to foreign capital markets.

Hedging foreign currency debt

Companies that have issued bonds or taken loans in a foreign currency use cross-currency swaps to convert those obligations back to their functional currency. This eliminates FX risk on both the debt service and the principal repayment.

Managing subsidiary funding

Multinational corporations often use cross-currency swaps to fund foreign subsidiaries efficiently. The parent raises debt in its home currency and swaps the proceeds into the subsidiary's operating currency.

Asset-liability matching

Insurance companies, pension funds, and other institutional investors use cross-currency swaps to match the currency of their assets with their liabilities, reducing balance sheet currency mismatch.

8. Cross-Currency Swaps vs. FX Forwards

Both cross-currency swaps and FX forwards provide hedging against foreign exchange risk, but they serve different purposes.

| Feature | Cross-Currency Swap | FX Forward |

|---|---|---|

| Principal Exchange | Yes, at inception and maturity | Yes, at maturity only |

| Interest Payments | Yes, periodic exchange of coupons | No (embedded in forward rate) |

| Typical Tenor | 1 - 30 years | Spot - 2 years (liquid) |

| Interest Rate Risk | Hedges both FX and interest rate risk | Hedges FX risk only |

| Best For | Long-dated debt hedging, multi-year funding | Short-term transaction hedging, receivables/payables |

For short-dated exposures (under two years), FX forwards are typically simpler and more cost-effective. For longer-dated exposures involving periodic cash flows, cross-currency swaps are the standard instrument.

9. Risks in Cross-Currency Swaps

Counterparty credit risk. Because cross-currency swaps involve exchange of principal amounts, the credit exposure between the counterparties is substantially larger than in a plain-vanilla interest rate swap. Most swaps are now cleared through central counterparties or collateralised under bilateral CSA agreements to mitigate this risk.

Mark-to-market volatility. Cross-currency swap valuations are sensitive to movements in both interest rates and the exchange rate. Large currency moves can create significant mark-to-market swings, which may trigger collateral calls under CSA agreements.

Cross-currency basis risk. The cross-currency basis can widen or tighten due to changes in supply-demand dynamics for dollar funding, central bank policies, or market stress. This affects the pricing and mark-to-market of existing swaps.

Liquidity risk. While major currency pairs (EUR/USD, GBP/USD, USD/JPY) are highly liquid, some emerging market cross-currency swaps may have limited liquidity, particularly for longer tenors.

10. Accounting for Cross-Currency Swaps

Under IFRS 9 and ASC 815, cross-currency swaps can qualify for hedge accounting treatment as either cash flow hedges or fair value hedges, depending on the hedged item and the hedge designation.

For hedges of foreign currency debt, the most common designation is a cash flow hedge of the foreign currency risk on both the principal and interest cash flows. Under IFRS 9, an entity may exclude the cross-currency basis spread from the designated hedging instrument and treat it as a cost of hedging. The excluded amount is recognised in OCI and accumulated in a separate component of equity, then reclassified to profit or loss either when the hedged transaction affects earnings (transaction-related hedges) or on a systematic basis over the hedge period (time-period-related hedges, which covers most hedges of foreign-currency debt).

11. Conclusion

Cross-currency swaps are a fundamental instrument for managing foreign exchange and interest rate risk across currencies. They involve the exchange of principal at inception and maturity, plus periodic interest payments during the life of the swap.

With the current USD-EUR interest rate differential ranging from 79 to 107 basis points across the curve (as of 9 April 2026), cross-currency swaps continue to play a central role in corporate funding strategies, particularly for European and UK corporates accessing the USD debt market.

The choice of swap structure (fixed-to-fixed, floating-to-floating, or fixed-to-floating) depends on the underlying exposure and the borrower's risk management objectives.

This article is for informational and educational purposes only and does not constitute financial, investment, legal, or tax advice. BlueGamma does not provide advisory services. Readers should consult qualified professional advisors before entering into any derivative transaction. Market data shown is indicative and sourced from BlueGamma as of the date stated.

Frequently Asked Questions

What is a cross currency swap?

A cross-currency swap is a derivative contract in which two parties exchange principal and interest payments denominated in different currencies. The principal is exchanged at inception and re-exchanged at maturity at the original spot rate, providing a hedge against foreign exchange risk on both the principal and the periodic interest cash flows.

How does a cross currency swap work?

At inception, the two counterparties exchange principal amounts at the prevailing spot rate. During the life of the swap, each party makes periodic interest payments in the currency it received. At maturity, the original principal amounts are returned at the same exchange rate used at inception, regardless of where the spot rate has moved. This structure hedges both interest rate and FX risk simultaneously.

What is a cross currency basis swap?

A cross currency basis swap is a floating-to-floating cross-currency swap in which both legs reference overnight or term rates in their respective currencies. One leg typically includes a spread (the cross-currency basis) over the reference rate, reflecting supply and demand imbalances for funding in each currency. The basis can be positive or negative and fluctuates with market conditions.

How to value a cross currency swap?

Valuation involves discounting each leg's future cash flows (both interest and principal) using the appropriate currency-specific discount curve. USD cash flows are discounted using the SOFR OIS curve and EUR cash flows using the ESTR OIS curve, for example. The net present value of each leg is converted to a common currency at the spot rate, and the difference represents the swap's mark-to-market value.

What is the difference between an FX swap and a cross currency swap?

An FX swap involves two exchanges of principal at different dates (typically spot and a forward date) with no periodic interest payments during the term. A cross-currency swap involves principal exchange at inception and maturity plus periodic interest payments throughout the life of the contract. FX swaps are generally used for short-term funding and liquidity management, while cross-currency swaps are used for longer-dated exposures where periodic coupon flows need to be hedged.