SONIA Swap Rates Today: Current & Historic UK Swap Rates

Current swap rates UK treasurers and lenders track daily: GBP SONIA interest rate swaps from 1 year to 50 years, annual vs compounded. Also covers current mortgage swap rates UK and mid swap rates.

Last update:

| Tenor | Live | 3 days ago24 Jul 2026 | 1 week ago16 Jul 2026 | 1 month ago23 Jun 2026 | 1 year ago23 Jul 2025 |

|---|---|---|---|---|---|

| 1 Year | |||||

| 2 Year | 4.25% | 4.16% | 4.00% | 3.51% | |

| 3 Year | 4.34% | 4.25% | 4.05% | 3.64% | |

| 4 Year | 4.36% | 4.27% | 4.07% | 3.68% | |

| 5 Year | 4.38% | 4.31% | 4.10% | 3.74% | |

| 7 Year | 4.46% | 4.40% | 4.19% | 3.88% | |

| 10 Year | 4.61% | 4.57% | 4.35% | 4.11% | |

| 20 Year | 4.95% | 4.94% | 4.73% | 4.55% | |

| 30 Year | 4.99% | 4.99% | 4.78% | 4.62% | |

| 50 Year | 4.82% | 4.83% | 4.63% | 4.45% | |

Rates built from interdealer broker and exchange quotes. Read how we build these rates.

Unlock the live curve

See today's live SONIA rates & the full forward curve

- Live intraday mids for every tenor

- Full forward curve for your model

- Excel Add-in & API access

- Price swaps, caps & get MtM

No card needed, cancels automatically

“We stopped chasing the bank for a mid. BlueGamma is our curve of record now.”

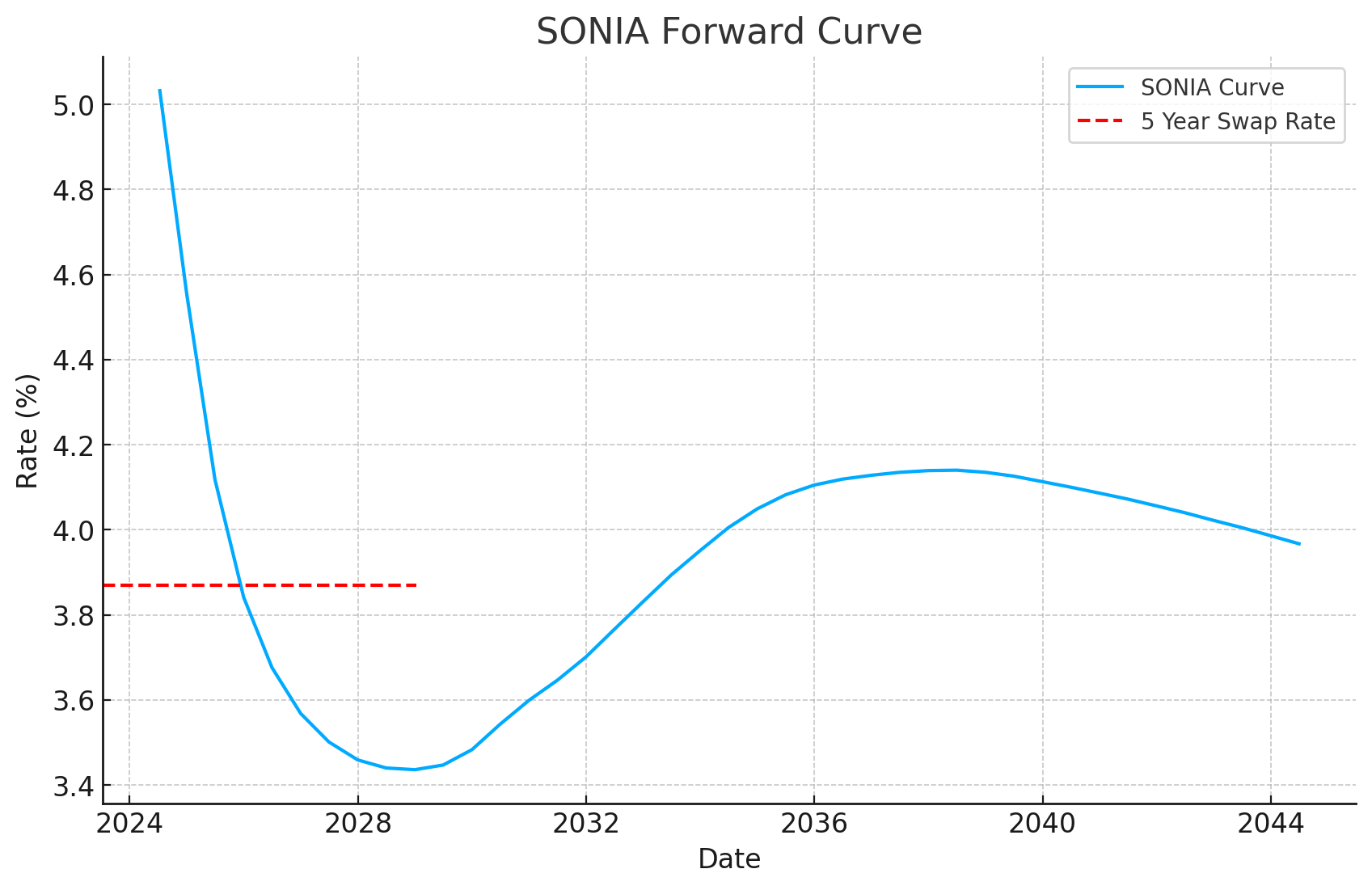

Spot is today. Deals price off the forward curve.

Hard-coding today's rate into a multi-year model quietly mis-states your debt service. The forward curve tells you what SONIA is expected to do each year: the number your credit committee actually wants.

Get the full forward curveLive SONIA rates in Excel & API

If you're on this page more than once a month, you don't need a rate, you need a feed. One function, always-live curves, straight in your model.

// Excel: live SONIA swap rate in a cell =BlueGamma.SWAP_RATE("SONIA", start_date, maturity_date, "1Y") # API: the same rate, one GET away GET api.bluegamma.io/v1/swap_rate ?index=SONIA&start_date=2D&maturity_date=5Y x-api-key: your_api_key

trusted by

SONIA rate today

Access the current SONIA rate. Wondering where it goes next? See the SONIA forecast and the Bank of England rate forecast.

| Index | Rate |

|---|---|

| BOE Bank Rate | 3.75000% |

| SONIA | 3.73100% |

FAQs

SONIA stands for the Sterling Overnight Index Average. It's the effective overnight interest rate paid by banks for unsecured transactions in the UK. SONIA is an overnight rate and not a term rate. Unlike traditional interest rates, SONIA is based on actual transactions, providing a more accurate reflection of the cost of borrowing. Swap rates, on the other hand, are forward looking fixed interest rates exchangeable for floating rates over an agreed period, typically longer than overnight. Essentially, they are contracts between two parties swapping future interest payments based on SONIA rates. Putting the two together, a SONIA swap rate is the market interest rate to lend or borrow over the agreed period.

Tip: SONIA swap rates are a replacement for UK LIBOR swap rates which were phased out in 2021/2022.

Here’s where Sonia swap rates come from:

- Market Trading: SONIA swap rates are determined in the market where they are traded based on the expectations of future compounded SONIA rates.

- Interpretation: A SONIA swap rate reflects the fixed interest rate agreed upon in the swap contract, which will be exchanged for floating payments based on the compounded SONIA rates over the specified period.

Example: Consider the 5-year SONIA swap rate. This rate represents the fixed interest rate that one would receive or pay in exchange for floating payments based on the compounded daily SONIA over the next five years. If the 5-year SONIA swap rate is quoted at 3.75%, it means that market participants expect the average compounded SONIA rate over the next five years to be close to 3.75%. Thus, entering into a 5-year SONIA swap at this rate means agreeing to pay or receive a fixed 3.75% interest rate while the counterparty pays or receives floating payments based on the actual compounded SONIA rates.

Not to be confused with SONIA rates

The daily SONIA rate is a fixing and not a swap rate. Sonia fixings are calculated as the weighted average rate of all unsecured overnight sterling transactions brokered in London by Wholesale Markets Brokers’ Association (WMBA) members between 12am and 3.15pm London time in a minimum deal size of £25m. Sonia fixings are generally used to settle swaps rather than to price them.

SONIA rates are published by the Bank of England.

Interest rates are a tool used by the Bank of England to help meet the UK’s 2% inflation target. Factors that influence inflation will therefore impact SONIA swap rates. Here are the key factors:

- Economic Conditions: Fluctuations in the UK economy, such as GDP growth or slowdown, can affect borrowing rates and subsequently, SONIA. For example, strong economic growth may lead to higher interest rates as demand for credit increases.

- Monetary Policy: Actions by the Bank of England, particularly changes to the base interest rate, directly impact SONIA rates. For instance, if inflation is above the 2% target, the Monetary Policy Committee (MPC) may increase the Bank of England rate, which is likely to push up SONIA swap rates.

- Market Liquidity: Higher liquidity in the overnight money markets tends to lower the SONIA rate, reducing swap rates. Conversely, reduced liquidity can increase rates.

- Inflation Expectations: Rising inflation expectations typically lead to higher interest rates, including SONIA. If the market anticipates higher inflation in the future, this will be reflected in higher SONIA swap rates.

By keeping an eye on these factors, you can better forecast SONIA rates and make more informed decisions in your financial models.

Example

When inflation is above the 2% target, the MPC might increase the base rate to cool down the economy. This increase would likely push up the SONIA swap rates as the cost of borrowing rises in response.

Pro-tip: As swap rates are constantly traded and volatile, regularly update your financial models with live SONIA swap rate data to ensure accuracy. You can pull data from platforms like BlueGamma to pull in real-time data seamlessly.

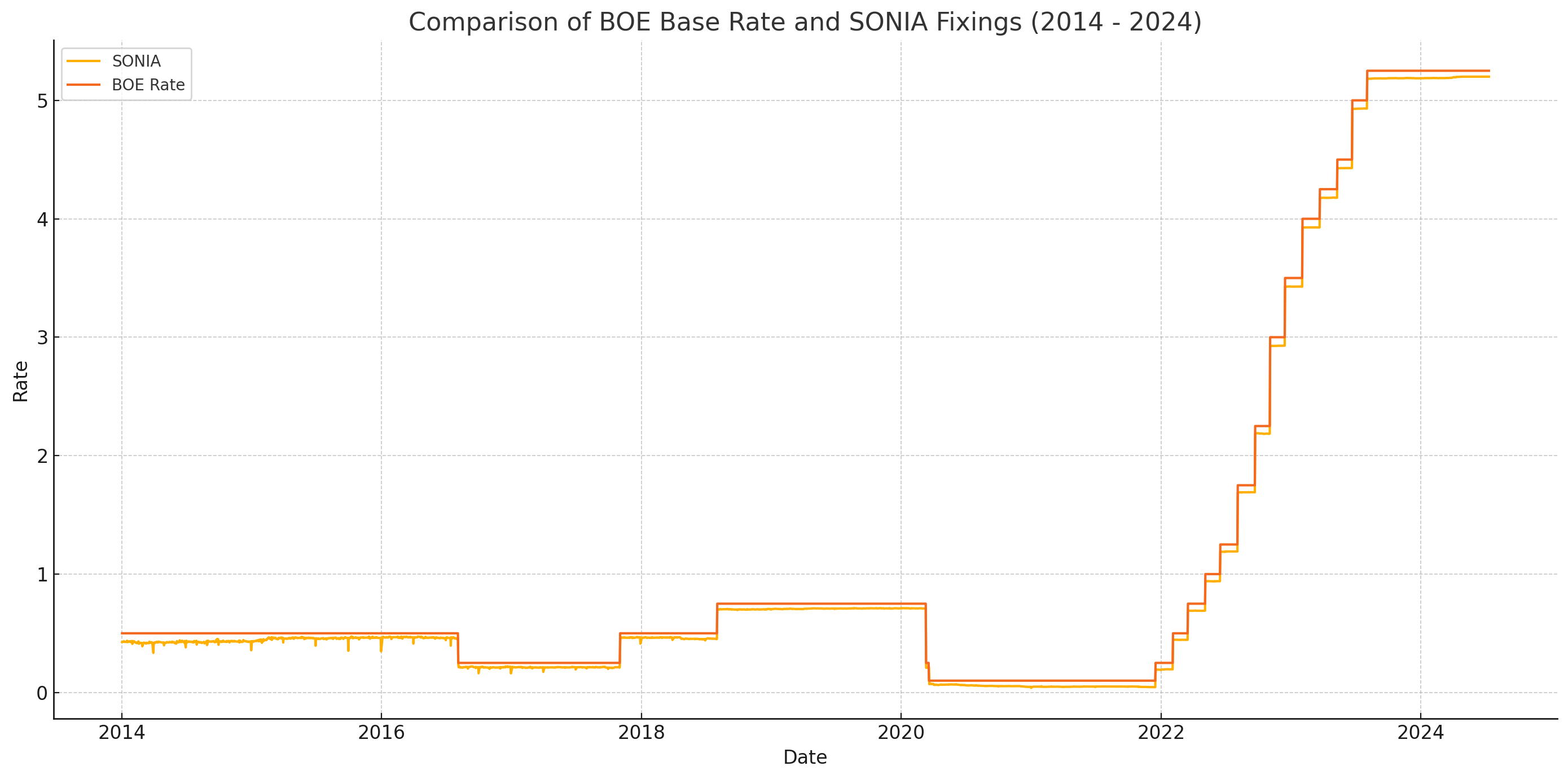

The BoE base rate is a policy rate set by the central bank, while SONIA is a market-driven rate based on actual transactions.

- Purpose: The base rate aims to influence economic activity and inflation, whereas SONIA provides a benchmark for financial instruments.

- Frequency of Change: The base rate changes through MPC decisions, whereas SONIA fluctuates daily based on market activity.

- Impact: The base rate directly affects consumer interest rates, while SONIA impacts financial contracts and the interbank lending market.

As can be seen from the graph - there is a high correlation but there is a difference in the 2 rates.

Simple Weighted Average Life Approach is straightforward and suitable for quick estimation of the fixed rate applicable.

- Identify the Appropriate Swap Rate: Match the forecast duration of your debt instrument with the relevant SONIA swap rate. For example, if you are modeling a 5-year debt, use the 5-year SONIA swap rate.

- Retrieve Up-to-Date Data: Ensure that you source the most current SONIA swap rates. Websites like BlueGamma provide comprehensive and updated rates.

- Incorporate the Swap Rate: Use the identified swap rate to calculate the interest cost over the life of the debt. Multiply the swap rate by the principal amount to estimate annual interest costs, adjusting for the periodicity of the model.

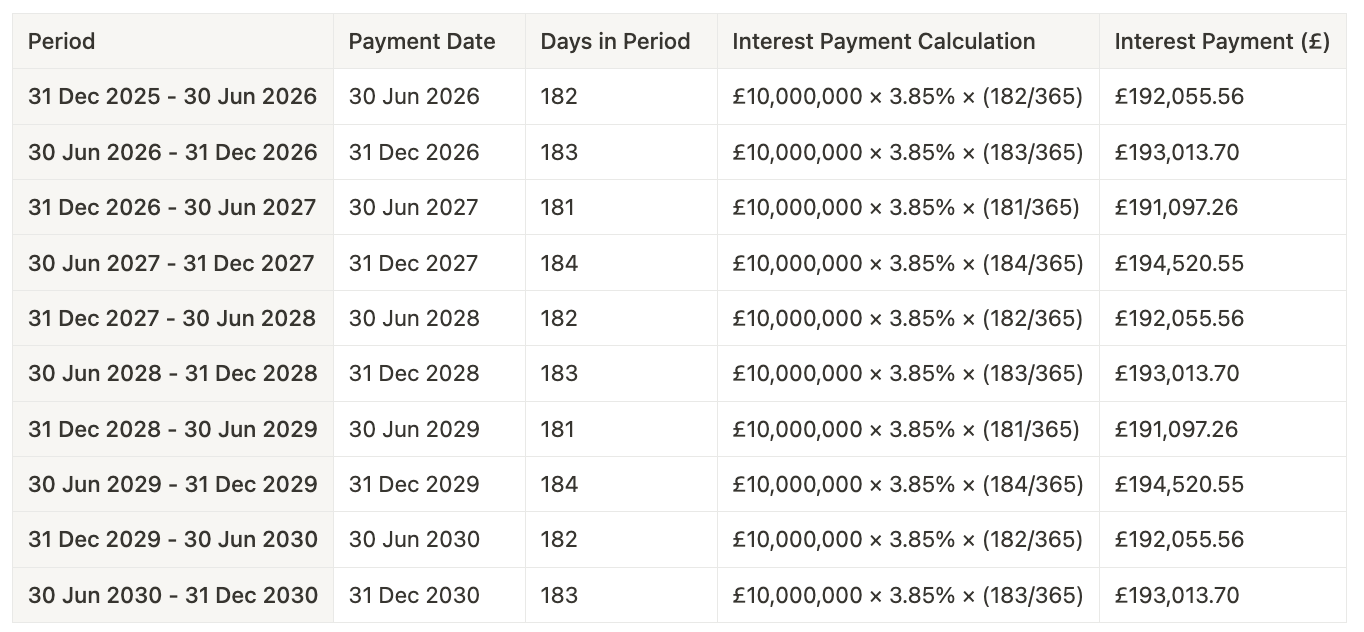

Example

For a 5-year debt instrument with a principal of £10 million and a 5-year SONIA swap rate of 3.85%, the schedule below provides a clear breakdown of the interest payments.

Assumptions

- Principal Amount: £10,000,000

- SONIA Swap Rate: 3.85%

- Semi-Annual Payments

- Payment Dates: Every June 30 and December 31

- That the swap has been taken out to hedge an underlying loan with the same notional amount. As such, we can assume that the interest on the floating leg of the swap nets off with the interest due on the loan

Schedule

Here's an example of what a typical schedule used to calculate interest payments might look like.

Pro-tip: remember, interest cost calculations are not discounted as they are a cash flow that takes place at a future point in time.

BlueGamma takes quotes directly from leading inter-dealer brokers and exchanges, bootstraps them into ready-to-use curves, and validates the output for consistency on a regular basis.

The rates shown on this page are the previous UK business day’s close. Live rates, refreshed every minute, are available in the BlueGamma app with a free trial.

Lenders fund fixed-rate mortgages by hedging with interest rate swaps, so UK fixed mortgage pricing closely tracks SONIA swap rates for the matching term: a 2-year fixed deal is priced off the 2 year SONIA swap rate (the UK 2 year swap), and a 5-year fix off the 5-year SONIA swap rate, plus a lender margin.

When swap rates rise, new fixed mortgage rates typically follow within days or weeks; when swap rates fall, fixed deals tend to get cheaper. The swap rates table above shows the current market levels lenders are pricing against.

More on SONIA

Bank of England Rate Forecast

Market-implied probabilities for the next MPC meeting and the Bank Rate path ahead.

SONIA Forward Curve

The market-implied path for SONIA: live forward curve, charted and downloadable.

Compounded SONIA

Daily and period-compounded SONIA rates for floating-leg calculations.

What is the SONIA rate?

How SONIA is set, what it replaced and how it is used across GBP markets.

Realised SONIA vs the forward curve

How realised SONIA compared with what the forward curve predicted.

Why 50Y SONIA swaps trade below 25Y

The long end of the SONIA curve inverts: what drives the 30Y hump and the dip beyond it.

Forward curve basics

How forward curves like SONIA's are built, read and used in models.

More from BlueGamma

Or browse the full swap rate catalogue, covering all 86 rates across 33 currencies.