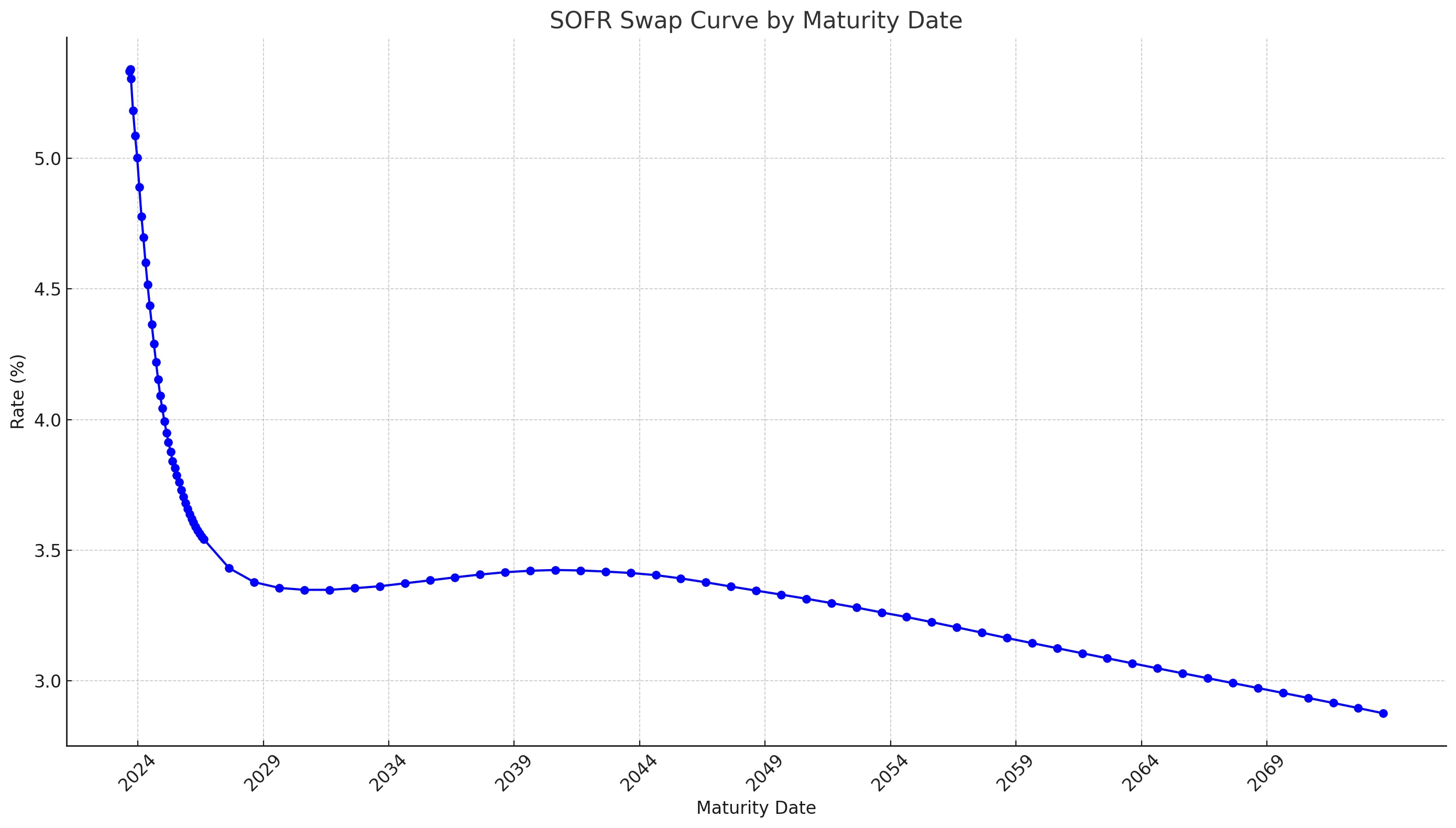

The swap curve is a visualization of interest rates associated with interest rate swaps over various time horizons.

Similar to the yield curve, which illustrates bond yields across different maturities, the swap curve represents the fixed rates agreed upon in interest rate swap contracts. Understanding the distinction between the swap curve and the yield curve is crucial, as each offers unique insights into the market's interest rate expectations.

What Exactly Is a Swap Curve?

A swap curve is a graphical depiction that shows the relationship between swap rates (fixed interest rates) and the maturities of the swaps. These rates are market-determined and reflect the market’s expectations for future interest rate movements.

Here’s a look at the current USD SOFR Swap Curve:

To explore the latest swap curves and gain direct access to the latest USD swap rates, click here.

How Is It Used?

The swap curve plays a pivotal role for financial professionals, serving several key functions:

- Interest Rate Forecasting: It helps in predicting future interest rate trends.

- Valuing Swaps: The curve is crucial for determining the fair value of interest rate swaps.

- Risk Management: Financial institutions use it to manage their exposure to interest rate volatility.

Swap Curve vs. Yield Curve: Why the Difference Matters

While both curves provide important insights, the swap curve vs. yield curve comparison reveals differences in the underlying financial instruments they represent. The swap curve reflects market expectations for interest rate swaps, whereas the yield curve relates to government bond yields. This distinction makes the swap curve particularly useful for pricing derivatives and managing interest rate risk in a more complex financial landscape.

Why Is It Important?

The swap curve offers deeper insights into the interest rate environment, often providing more nuanced information than a simple yield curve. It is a critical component in the pricing of various financial products, such as corporate bonds and mortgage-backed securities.

A thorough understanding of the swap curve is invaluable for those involved in managing interest rate risk or pricing complex financial instruments, enhancing the quality of decision-making in the financial sector.

To explore the latest swap curves and gain direct access to the latest USD swap rates, click here.