In project finance, locking in a fixed rate through an interest rate swap is more than just good practice—it's a requirement. Whether you're modeling senior debt repayments or stress-testing CFADS, the swap rate calculation feeds directly into affordability, DSCR, and overall project viability.

At BlueGamma, we help teams calculate swap rates accurately and instantly. Here's how it works—and why it's critical for infrastructure debt and renewable energy projects.

What Is a Swap Rate?

A swap rate is the fixed interest rate that equates the present value of the fixed leg and the floating leg of an interest rate swap. In project finance, swaps are used to convert floating-rate debt into fixed-rate obligations to reduce interest rate risk.

Why Swap Rates Matter in Project Finance

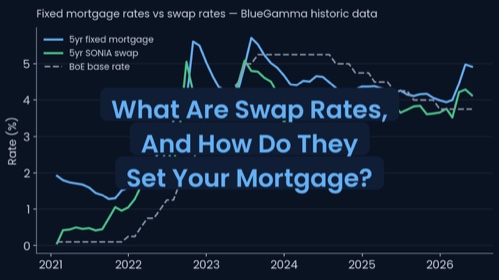

Many infrastructure and renewable energy projects are funded with floating-rate loans indexed to benchmarks like SONIA, SOFR, or EURIBOR. Sponsors use interest rate swaps to hedge that exposure.

A small error in swap pricing can lead to:

- Over- or underestimating base case DSCR

- Incorrect debt sizing

- Inaccurate reserve account planning

That's why it's critical to calculate swap rates precisely—and reflect the real project cash flow profile.

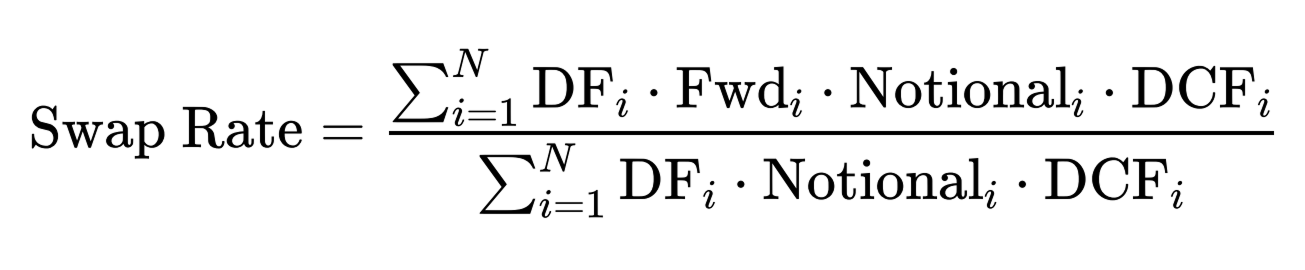

The Swap Rate Calculation Formula

To price a swap, we equate the present value of the floating cash flows with the fixed leg using this formula:

Where:

- DFi : Discount Factor for period i

- Fwdi : Forward rate for period i

- Notionali : Outstanding notional for period i

- DCFi : Day count fraction for period i

Example: 10-Year Swap with a Amortising Notional Profile

Let's walk through an illustrative example using a typical project finance-style amortisation.

| Period | Notional (USD) | Forward Rate (%) | Day Count Fraction | Discount Factor |

|---|---|---|---|---|

| 1 | 100,000,000 | 5.00% | 0.25 | 0.987 |

| 2 | 90,000,000 | 5.10% | 0.25 | 0.974 |

| 3 | 80,000,000 | 5.20% | 0.25 | 0.961 |

| 4 | 70,000,000 | 5.30% | 0.25 | 0.948 |

| 5 | 60,000,000 | 5.40% | 0.25 | 0.935 |

| 6 | 50,000,000 | 5.50% | 0.25 | 0.922 |

| 7 | 40,000,000 | 5.60% | 0.25 | 0.909 |

| 8 | 30,000,000 | 5.70% | 0.25 | 0.896 |

| 9 | 20,000,000 | 5.80% | 0.25 | 0.883 |

| 10 | 10,000,000 | 5.90% | 0.25 | 0.870 |

You can plug these into Excel with the following formula:

=SUMPRODUCT(DFs, Fwds, Notionals, DCFs) / SUMPRODUCT(DFs, Notionals, DCFs)

This returns the par swap rate—the fixed rate that would exactly offset the floating cash flows in present value terms.

Make This Automatic With BlueGamma

BlueGamma makes swap rate calculation effortless. Our tools are used by infrastructure funds, advisors, and treasury teams to:

- Price amortising swaps

- Export results to Excel

- View historical movement of amortising swap rate

Here's a video showing how to price an amortising interest rate swap like this one using BlueGamma:

🎯 Start Your Free Trial

Ready to take control of your swap pricing?

👉 Create a Free Trial Account and get instant access

No credit card required. Just accurate swap rates in seconds.