What is it?

Pre-hedging in project financing is a strategic financial practice designed to mitigate volatility from market-based inputs such as power prices, interest rates, FX rates, inflation rates and commodity prices. Consider a wind project, for instance:

- Power Price Risk: This arises from selling power at prevailing market rates. It is commonly pre-hedged with a corporate Power Purchase Agreement (cPPA) locked in before financial close

- Interest Rate Risk: Stemming from financing linked to indexes like EURIBOR, this is often pre-hedged using a deal contingent hedge or a forward-starting swap

- FX Risk: Encountered when investing in a foreign currency or procuring components in different currencies, typically pre-hedged with vanilla FX forwards or deal contingent hedges

- Inflation Risk: Given the long term nature of projects, inflation linkage in either revenue or cost contracts is common. This is typically hedged with a revenue swap but may be left unhedged on the cost side, depending on the projects preferences and risk tolerance

- Commodity Price Risk: Related to fluctuations in component costs, such as steel. This risk is often left unhedged due to the complexities and uncertainties in predicting commodity prices

For the purposes of this blog, we'll focus on interest rate risk, where pre-hedging is most commonly seen in project finance.

Why is interest rate pre-hedging common in project finance?

Pre-hedging in the context of interest rates involves locking in the interest rate for future loans or financial obligations before securing the main financing. This practice is particularly crucial in project finance, where the primary source of funding is often a senior-secured term loan provided by a commercial bank. Large-scale projects, such as offshore wind farms, are highly sensitive to even minor fluctuations in interest rates, as these can significantly impact overall costs.

By adopting a pre-hedging strategy, developers and investors can stabilize their financing costs. This creates a more predictable and secure budgeting framework while the main financing is in the process of being arranged. Pre-hedging serves as a proactive approach to managing financial exposure, ensuring cost-effectiveness for projects that have extended timelines, such as in large-scale construction or infrastructure developments.

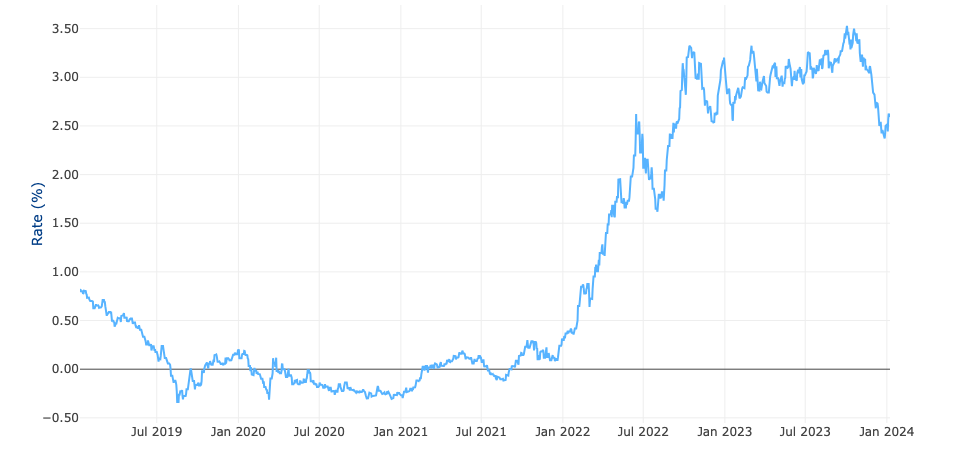

The need for pre-hedging becomes particularly acute in times of market volatility to help with planning. For instance, the 10Y EUR swap rate's rise from 0.3% to nearly 3.5% since the start of 2022 underscores this point.

Developers and investment managers, whose primary responsibility is to mitigate financial risks rather than gamble on interest rate movements, frequently opt for pre-hedging as a safeguard against such uncertainties.

How can a project pre-hedge interest rate risk?

In project finance, there are typically three instruments most often used for pre-hedging interest rate risk.

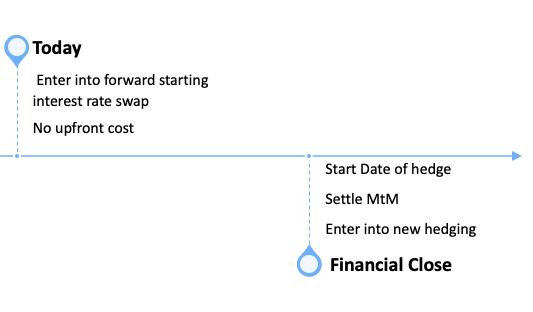

1. Vanilla Forward Starting Swap

A forward-starting swap is an agreement where a project enters into a swap starting at a future date, typically the expected date of the first drawdown. Such instruments are typically used by large corporates who are able to provide guarantees.

Benefits:

- No Upfront Cost: This makes them financially accessible as there's no initial expense to lock in the rate

- Interest Rate Lock-In Before Financial Close: By securing the interest rate early, these swaps significantly de-risk the project from interest rate volatility.

- Cost-Effectiveness: Often considered the cheapest form of pre-hedging, they provide an economical option for managing interest rate risk

Drawbacks:

- Potential Settlement of Mark-to-Market at Financial Close: If interest rates fall, there may be a need to settle the mark-to-market value, which could require a significant payment. Though there are increasingly methods to defer this payment, it remains a consideration

- Complex Execution at SPV Level: Implementing these swaps at the Special Purpose Vehicle (SPV) level typically requires a parental guarantee as security. This can make the documentation process more time-consuming and introduces an additional layer of project-level risk

2. Swaption

A swaption is a financial contract that offers the borrower the right, but not the obligation, to enter into an interest rate swap at a predetermined rate (the strike rate) on a future date (expiry date). There are three kinds of swaptions

- European: Exercisable only on the expiration date, preferred in project finance for their simplicity and cost-effectiveness

- American: Can be exercised at any time up to the expiration date, offering more flexibility but at higher complexity and cost

- Bermudan: Allow exercise on specific dates before expiration, offering a balance between flexibility and complexity, least common in standard project finance

In project finance, European swaptions are often the focus due to their optimal balance of cost and risk mitigation. Here's how a European swaption typically functions:

- Scenario 1 (Swap Rate Exceeds Strike Rate): On reaching the expiry date, if the market swap rate is higher than the strike rate, the borrower can opt to enter the swap at the favorable strike rate, potentially receiving compensation for the difference

- Scenario 2 (Swap Rate Below Strike Rate): If the market swap rate is lower than the strike rate, the borrower may decide not to exercise the swaption. However, the initial premium paid for securing this right is not recovered

Essentially, a swaption serves as a cap on the maximum interest rate payable, providing the borrower with both flexibility and protection against rising interest rates. This theoretically makes swaptions an valuable tool in project finance, but in practise this is rarely seen as getting the expiry date to coincide with the financial close date can be very challenging.

In practice, this means the borrower will pay a maximum interest rate of the strike rate.

Benefits:

- Opportunity to Capitalize on Lower Rates: If interest rates decrease between the present time and the financial close, the project can benefit from these lower rates

- Simplified Trading Process: Swaptions do not require an International Swaps and Derivatives Association (ISDA) agreement and can be traded via a Long Form Confirmation (LFC), streamlining the proces

- Quick Implementation: The process of putting a swaption in place is relatively quick, which is beneficial in time-sensitive project finance scenarios

- Competitive Pricing: Running a competitive process to acquire swaptions ensures that the best possible pricing is achieved, offering cost efficiency

Drawbacks:

- Potential for High Premiums: In times of high market volatility, the cost of securing a swaption (the premium) can be substantial

- Expiry Date Alignment: The swaption's expiry date needs to be closely aligned with the financial close date of the project. If this alignment is not precise, there may be a need to pay additional premiums to extend the swaption's validity

- Complexity in execution and valuation: Swaptions are structured products and require a deep understanding for effective execution and valuation which might necessitate expertise or advisory services

3. Deal-Contingent Hedge

Deal-contingent hedges are specialized financial tools in project finance. They represent agreements set in place before a project's financing is finalized, but they activate only when the financing transaction successfully closes. The unique aspect of these hedges is their contingency: if the project does not reach financial closure within a set timeframe, both parties can dissolve the agreement without any financial repercussions, provided no similar financing is arranged soon after.

In essence, a deal-contingent interest rate swap functions as a forward-starting swap, but with its validity hinging on the project’s successful closure. If the project fails to close, the agreement becomes void, allowing both parties to exit without obligations.

Benefits:

- Interest Rate Certainty: They provide a guaranteed interest rate for the entire duration of the project's debt, offering financial predictability

- Cost-Effective: These hedges are relatively low in cost, especially considering the protection they offer against interest rate volatility

- No Settlement of Mark-to-Market if Project Fails: If the project does not reach financial close, the project company isn't required to settle the mark-to-market (MtM) valuation, reducing financial risk

- Flexibility with Project Documents: They can be implemented even if all project-related documents, such as contracts and permits, are not fully executed, offering flexibility in project timelines

- Alignment with Project Milestones: Deal-contingent hedges can be precisely timed to match key project milestones, ensuring financial stability aligns with project progress.

- Risk Transfer: if structured correctly, the contract effectively offloads interest rate risk from the project sponsors during the most critical phase of the project

Drawbacks:

- Limited Availability: Deal-contingent hedges may not be available for all types of projects or in all market conditions, particularly in cases of high uncertainty or risk

- Price Sensitivity to Project Risk: The cost of a deal-contingent hedge is often sensitive to the perceived risk of the project. Higher risk projects may face higher hedging costs

- High Probability of Financial Close Required: The likelihood of the project reaching financial close needs to be strong, as the hedge is contingent on this event.

- Intensive Due Diligence: The hedge provider will conduct thorough due diligence to assess the probability of the project's financial close. This process can be resource-intensive and time-consuming

- Potential for Hedging Inefficiency: If the project’s timeline is delayed or the scope changes significantly, the hedge may not align perfectly with the new financial needs, leading to inefficiencies or additional costs in restructuring the hedge

It is important to remember that all derivative products can carry significant liabilities and you must take the time to understand potential adverse scenarios before entering into any such instrument. At BlueGamma, we can help you with indicative pricing for such scenarios. Just get in touch 😁