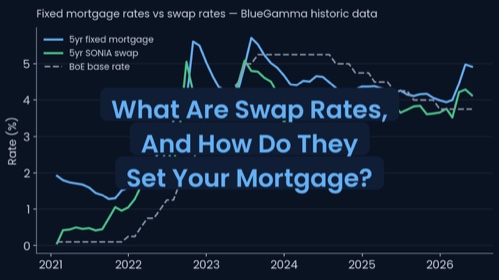

As the global economy recovers from the COVID-19 pandemic and fights of the ensuing inflation, interest rates have been rising across the globe. This has important implications for project finance in the renewable energy sector, which often relies on long-term debt financing to fund large-scale projects. To manage the risk of rising interest rates, companies in the renewable energy sector use interest rate hedging. Generally this is in the form of an interest rate swap but can also take the form of an interest rate cap, or interest rate collar.

Hedging interest rates is often also a requirement imposed by lenders if a company is drawing project finance debt. In the IEA Net Zero Emissions by 2050 Scenario (NZE), they estimate that around 70% of clean energy investment over the next decade will need to be carried out by private developers who will generally use project finance to fund the construction cost. Such lenders will require the project to enter into an interest rate hedge but before you commit - it is important to ask yourself these 5 key questions:

1. What is my risk appetite and my objective?

Interest rate hedging tools come with inherent risks, and you must be at ease with the possible drawbacks of the strategy you opt for. Keep in mind that interest rate hedging involves committing to a specific structure for a duration, and unforeseen or potentially high costs may arise if you need to modify or alter them. To help evaluate this, it is important to consider sensitivity and scenario analysis. For example if you were looking at an interest rate swap, you may consider looking at how your mark-to-market changes with time to ensure you understand potential breakage costs.

2. What type of interest rate hedging instrument is appropriate for my project?

In selecting the ideal interest rate hedging instrument for your project, generally one of three instruments are usually used: interest rate swaps, interest rate caps, and interest rate collars as each of them help limit the maximum amount of interest you will have to pay. The parameters of these instruments can be adjusted to align with your objectives. Each tool has unique features and associated risks, making it essential to evaluate their costs and benefits in light of your project's goals and risk tolerance.

By familiarizing yourself with these instruments and adjusting their parameters within the context of your project or financing structure, you can tailor the hedging strategy to suit your needs. Ultimately, the most suitable instrument is determined by a thorough assessment of your objectives, risk appetite, and how these factors relate to your project's financial model.

3. How will the interest rate hedging strategy impact my project's financial performance?

When implementing an interest rate hedging strategy, it's essential to consider how it will affect your project's financial performance. The chosen instrument, whether it's a swap, cap, or collar, will have direct implications on your interest payments, cash flow, and overall financial stability.

Interest rate swaps can help stabilize cash flow by converting floating-rate payments into fixed-rate ones. However, this may come at the cost of missing out on potential savings if interest rates decrease. Caps, on the other hand, limit your exposure to rising interest rates while allowing you to benefit from lower rates. Although caps often require an upfront premium, they can protect your project from sudden interest rate spikes.

Collars combine the features of both swaps and caps, offering a balance between protection and flexibility. By setting both an upper and lower limit on interest rates, they help manage potential interest rate fluctuations within a specified range. Therefore understanding the impact of your chosen hedging instrument on your project's financial performance is crucial for making informed decisions that align with your objectives and risk tolerance.

4. What are the legal, regulatory and accounting considerations for my interest rate hedging strategy?

It's crucial to navigate the legal and regulatory landscape. For example checking things like the credit rating of your counterparty and whether they are a regulated entity permitted to engage in hedging transactions or are they acting as an intermediary. Familiarize yourself with reporting requirements under regulations like EMIR or Dodd-Frank (or ask your lender to help you with this), and leverage the ISDA Master Agreement for legal certainty in your interest rate hedge. Establish collateral arrangements, such as Credit Support Annex (CSA), and consult legal and tax advisors to understand the implications of different hedging instruments.