What is a Forward-Starting Swap?

A forward-starting swap is an interest rate swap that begins on a future date. The counterparties agree today on the fixed and floating terms, but payments and notional exchange start later, often to hedge or lock in rates for a future funding period.

In essence, it’s a standard interest rate swap with a deferred start date and they’re widely used to manage future interest rate exposure, especially around refinancing or bond issuance schedules.

How Do Forward-Starting Swaps Work?

On the trade date, terms like notional, fixed rate, floating index, tenor, start/end dates) are agreed. This typically includes a the forward period: No cashflows occur before the effective date (also known as the start date). After the forward period, or rather once the effective date has passed, the swap period begins which includes regular fixed vs. floating interest payments over the agreed term.

The swap effectively locks in the future swap rate between the forward start and maturity.

Why Use a Forward-Starting Swap?

- Lock in future funding costs ahead of issuance or refinancing.

- Hedge anticipated interest rate risk tied to future liabilities.

- Express rate views without current balance sheet exposure.

- No Upfront Payment is a Key Feature

Advantages and Disadvantages of Forward-Starting Swaps

Advantages

- Hedge future rate exposure efficiently

- Customisable structure and tenor

- Zero initial cashflow

Disadvantages

- Valuation sensitive to curve shifts

- Counterparty credit exposure

- Potential collateral requirements under CSA

Customisation and Flexibility in Forward-Starting Swaps

These swaps can be fully tailored similar to regular interest rate swaps, here’s what you can customise:

- Effective Start Date: Choose a start date from a few days to several years in the future.

- Swap Term (Tenor): Define the length of the swap, from several months to over 30 years.

- Contractual Details: Specify payment frequencies, day count conventions, and the underlying floating rate benchmark (such as SOFR or EURIBOR).

Practical Applications of Forward-Starting Swaps

Forward-starting swaps are instruments used by various market participants to manage future interest rate risk. Here are some of the most common applications:

- Corporate Hedging for Future Debt Issuance: A corporation planning to issue a bond in six months or a year faces the risk that interest rates will rise before the issuance date, increasing their future borrowing costs. By entering into a forward-starting swap, the company can lock in today's interest rate for the period corresponding to the life of the bond. This effectively hedges against adverse rate movements and provides certainty for financial planning, pre-hedging their interest rate risk exposure.

- Real Estate and Project Finance: Consider a real estate developer who secures a short-term, floating-rate construction loan. Once construction is complete, this loan is set to convert into a long-term, permanent mortgage, which is also often at a floating rate. The developer is exposed to the risk that interest rates could be significantly higher when the permanent financing begins. To mitigate this, the developer can execute a forward-starting swap at the beginning of the project to pre-hedge their interest rate risk exposure, fixing the interest rate on the permanent loan well in advance. This provides crucial cost certainty for the project's long-term viability.

- Asset Managers Adjusting Duration Exposure: Investment managers use forward-starting swaps to adjust the interest rate sensitivity (duration) of their portfolios for a future period. For instance, if a portfolio manager anticipates that interest rates will rise in the future but does not want to sell current holdings, they can enter a forward-starting swap to receive a fixed rate and pre-hedge their interest rate risk exposure. This effectively reduces the portfolio's duration at a future date, protecting its value from the anticipated rate increase.

Pricing and Structuring a Forward-Starting Swap

Pricing is derived from the current swap curve using discount factors and forward rate projections. The fixed rate is set so the swap has zero present value at inception.

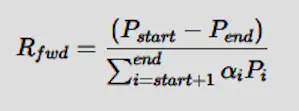

Forward-Starting Swap Rate Formula

The forward swap rate is calculated from discount factors:

Where:

- Pstart and Pend = discount factors at the start and end dates

- αi = accrual fraction for each floating period

- Pi= discount factor for each payment date

This formula ensures the fixed leg equals the floating leg in PV terms at the forward start.

Forward-Starting Swap Valuation

Valuation follows standard swap principles:

- The fixed leg PV uses the locked-in forward rate.

- The floating leg PV uses forward rates from the yield curve.

- The difference between legs gives the mark-to-market value.

If yield curves shift after trade inception, the value changes, even before the swap’s start date.

Forward-Starting Swap Example and Calculation

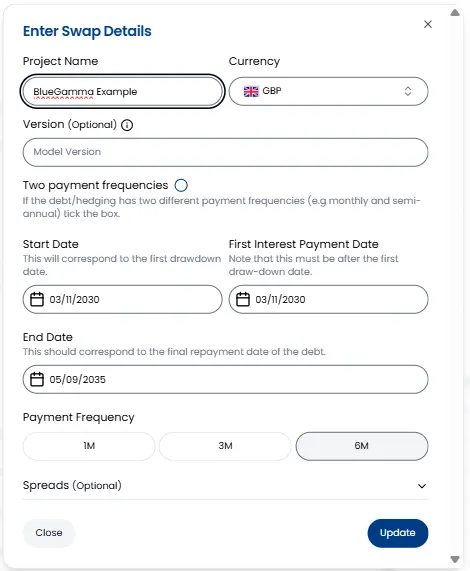

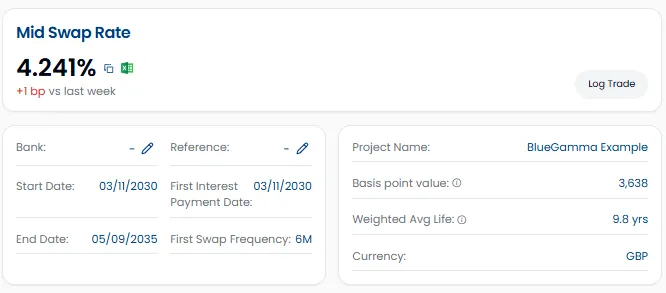

Step 1: Enter the Swap Details in BlueGamma

Pricing a Forward Starting Swap with the BlueGamma Interest Rate Swap Calculator is super easy, all that you need to do is enter the swap details with the Start Date and First Interest Payment Date in the future, the rest is done for you!

So first, navigate to the Swap Pricer in your BlueGamma account and input the full details of the swap as if it were a standard swap.

- Project Name: Give your project a descriptive name, like "Forward-Starting Hedge".

- Currency: Select GBP.

- Start Date: Enter the future date when the swap's interest payments will begin, in this case, 03/11/2030.

- First Interest Payment Date: This will be the first date a payment is made, for a 6M frequency, this would be 03/11/2030.

- End Date: Enter the final maturity date of the swap, 05/09/2035.

- Payment Frequency: Select 6M.

Once you have entered these details, click "Update" or "Create" to proceed to the main pricing screen.

Step 2: Interpret the Result of your Forward Starting Swap

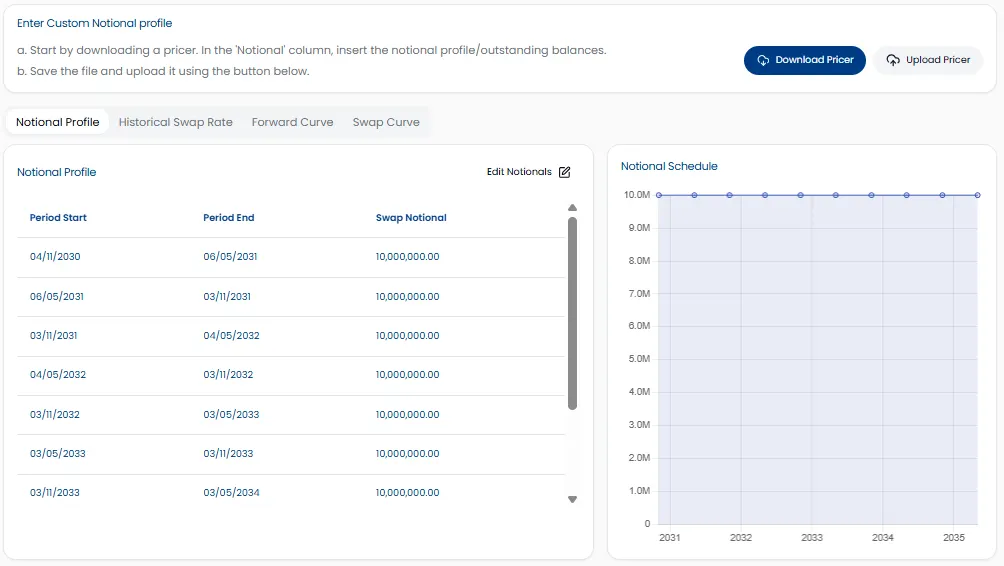

So once you’ve create the Forward Starting Swap, you can see the notational values are automatically set to the future start of your swap.

Now it’s time to Interpret the Result.

Our Interest Rate Swap Calculator shows you some valuable info on your Forward Starting Swap

Mid Swap Rate and Project Details:

Notational Profiles (which you can easily edit):

Your Forward Starting Swap’s Forward Curve:

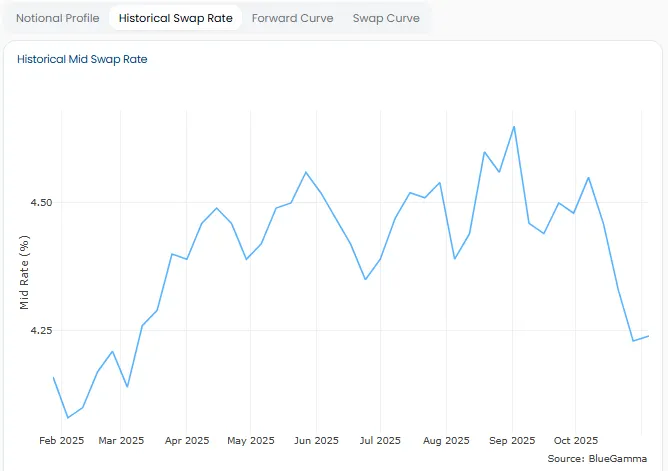

Historical Mid Swap Rate:

Swap Curve:

To further analyse the cash flows or integrate the forward curve into your own financial models, you can also download the forward curve directly from the "Forward Curve" tab.

Key Considerations Before Entering into a Forward-Starting Swap Agreement

- Ensure hedge matches the terms of the underlying exposure so it is not seen as speculation.

- Ensure hedge accounting treatment aligns with corporate policy.

- Understand credit support and margining implications.

- Model mark-to-market volatility during the forward period.

- Compare with DSF or options-based alternatives for flexibility.