In this article, we'll explore Term SOFR vs Compounded SOFR, a common question we get from clients working on project finance or floating-rate loans. Specifically, can you use Compounded SOFR forward curves to model facilities that reference Term SOFR? The short answer: yes, and here's why.

We'll show you how to fetch both forms of SOFR via our API, explain when each rate matters, and share key market statistics that every financing professional should know.

What Are the Four Types of SOFR?

Before diving into the Term vs Compounded comparison, it's worth understanding that SOFR comes in four main forms, each serving different purposes:

| SOFR Type | Publisher | Primary Use |

|---|---|---|

| Daily SOFR | NY Fed | Base rate, published each business day |

| SOFR Averages | NY Fed | 30, 90, 180-day compounded averages |

| SOFR Index | NY Fed | Cumulative compounding factor for custom periods |

| Term SOFR | CME Group | Forward-looking term rates (1M, 3M, 6M, 12M) |

The NY Fed publishes Daily SOFR, SOFR Averages, and the SOFR Index each business day. CME Term SOFR is derived from SOFR futures and is the only forward-looking rate of the four.

The Difference Between Term SOFR and Compounded SOFR

The difference between Term SOFR and Compounded SOFR is timing. Term SOFR is a forward-looking rate published at the start of an interest period, while Compounded SOFR is a backward-looking rate calculated by compounding daily fixings over the period.

| Rate | How It's Set | When You Know It |

|---|---|---|

| Term SOFR | Published daily by CME based on SOFR futures | At the start of the interest period |

| Compounded SOFR (in arrears) | Calculated by compounding daily SOFR fixings over the period | At the end of the interest period |

| Daily Simple SOFR | Simple average of daily SOFR rates (no compounding) | At the end of the interest period |

Term SOFR is essentially the market's forward-looking expectation of where 3-month Compounded SOFR will settle by the end of the period. This makes them fundamentally linked.

Daily Simple SOFR is a third option you'll see in some loan documents—it uses a simple average rather than compounding, resulting in slightly lower rates. However, Compounded SOFR in arrears remains the market standard for derivatives.

The LIBOR Transition: Why We Have Multiple SOFR Variants

The proliferation of SOFR types stems from the LIBOR transition. When LIBOR was discontinued, different market participants needed different SOFR variants:

- Derivatives markets adopted Compounded SOFR in arrears (via ISDA's fallback mechanism)

- US syndicated loans predominantly chose Term SOFR for operational simplicity

- European USD loans have historically favoured Compounded SOFR in arrears

For loans transitioning from LIBOR, a credit spread adjustment (CSA) was applied to account for the historical difference between LIBOR and SOFR. The ISDA-fixed spread adjustments were 11.448 bps for 1-month and 26.161 bps for 3-month tenors.

Key Market Statistics

Understanding the market context helps explain why both rates matter:

- Virtually all new US floating-rate loans now reference SOFR following LIBOR's discontinuation in June 2023

- $1.55 trillion is the size of the US leveraged loan market as of late 2025—a record high

- Over 2,870 firms globally use CME Term SOFR as their benchmark rate

- Compounded SOFR is the rate used in ISDA's fallback mechanism for derivatives, making it the most liquid SOFR variant for interbank trading

The ARRC (Alternative Reference Rates Committee) supports Term SOFR use "for business loan activity, particularly multi-lender facilities, middle market loans, and trade finance loans."

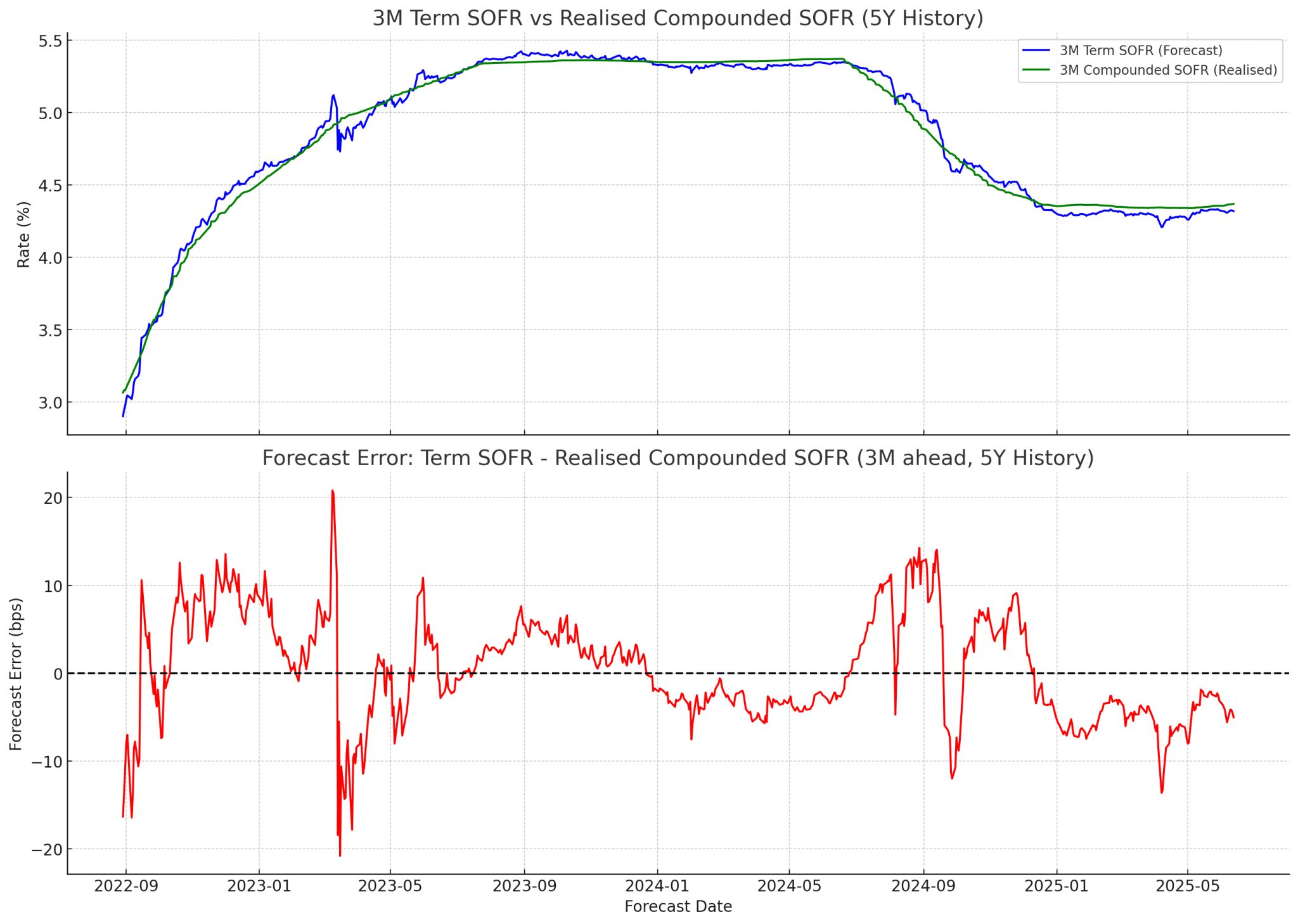

Historical Comparison: How Similar Are They?

We compared over 5 years of data between Term SOFR and realized Compounded SOFR rates. The two rates track very closely, as shown below:

The only meaningful divergences occur when the Federal Reserve surprises markets—for example during emergency rate cuts or unexpected hawkish pivots.

Key Insight: Compounded SOFR forward curves give you a very similar picture to what Term SOFR would, making them interchangeable for most forecasting and modeling purposes.

Practical Implications for Your Financial Models

If your loan documentation specifies Term SOFR (as many syndicated facilities now do), you might worry about whether BlueGamma's Compounded SOFR curves are suitable for your model. Here's the good news:

- For forecasting interest costs: Compounded SOFR forward curves are an excellent proxy for Term SOFR expectations

- For settlement calculations: Use the actual Term SOFR fixing from your reset date

- For historical analysis: Both rates can be fetched via the BlueGamma API

For more context on how SOFR curves are built, see our guide on SOFR Curve Construction.

Fetching Compounded SOFR via the API

Use the /compounded_rate endpoint to calculate realized compounded rates for any period. For a complete overview of our API capabilities, see our Interest Rate API guide.

import requests

url = "https://api.bluegamma.io/v1/compounded_rate"

headers = {"x-api-key": "your_api_key"}

params = {

"index": "SOFR",

"start_date": "2025-09-17",

"end_date": "2025-12-16"

}

response = requests.get(url, headers=headers, params=params)

print(response.json())

Response:

{

"start_date": "2025-09-17",

"end_date": "2025-12-16",

"index": "SOFR",

"rate": 4.090541,

"day_counter": "Actual360"

}

This matches the NY Fed's published 90-day SOFR Average exactly (4.09054%), validating our methodology.

Fetching Term SOFR Fixings

For historical Term SOFR fixings, use the /fixing endpoint:

params = {

"index": "3M Term SOFR",

"valuation_date": "2025-12-16"

}

response = requests.get(

"https://api.bluegamma.io/v1/fixing",

headers=headers,

params=params

)

You can also fetch Term SOFR directly in Excel using our Add-in:

=BlueGamma.FIXING("3M Term SOFR")

When Does It Matter Which Rate You Use?

| Use Case | Recommended Rate |

|---|---|

| Forecasting interest costs in a financial model | Compounded SOFR forward curve |

| Calculating actual interest payment at reset | Term SOFR fixing (from documentation) |

| Pricing an interest rate swap hedge | Compounded SOFR (market standard) |

| Validating lender calculations | Both, compare Term SOFR fixing to compounded rate |

Term SOFR swaps are available to borrowers. However, dealers typically hedge their own Term SOFR exposure using Compounded SOFR swaps, since interdealer Term SOFR trading is restricted.

If you're hedging your floating rate exposure, our Swap Rate Calculation in Project Finance guide covers the key considerations.

Understanding NCCR (Non-Cumulative Compounded Rate)

Some loan documents reference "NCCR" or Non-Cumulative Compounded Rate with specific conventions. "Non-cumulative" means the compounded rate is calculated fresh for each interest period using daily SOFR fixings, rather than derived from a running index like the SOFR Index.

Key parameters include:

- Lookback: Using rates from N days prior (e.g., 5 SOFR Banking Days)

- Observation Period Shift: Whether the observation period is shifted

- Floor: Minimum rate applied to daily SOFR before compounding

A SOFR floor of 0% is common in many loan agreements, preventing negative interest accrual in hypothetical negative rate scenarios.

The BlueGamma API supports all these conventions:

params = {

"index": "SOFR",

"start_date": "2025-09-17",

"end_date": "2025-12-16",

"lookback_days": 5,

"lockout_days": 0

}

For more on how overnight rates work in swaps, see our explainer on Overnight Index Swaps (OIS).

Summary

For practical financial modeling purposes, Compounded SOFR forward curves are an excellent proxy for Term SOFR. The rates track each other closely, and any differences are typically within the margin of error for most forecasting applications.

If you need precise Term SOFR fixings for settlement or audit purposes, BlueGamma provides both via our API and Excel Add-in.

Need help aligning your model to your term sheet? Book a call with our team, we're happy to walk through your specific use case.