Signing a deal is stressful enough without worrying about rates moving against you before closing. Deal-contingent hedging solves this problem.

What is Deal-Contingent Hedging?

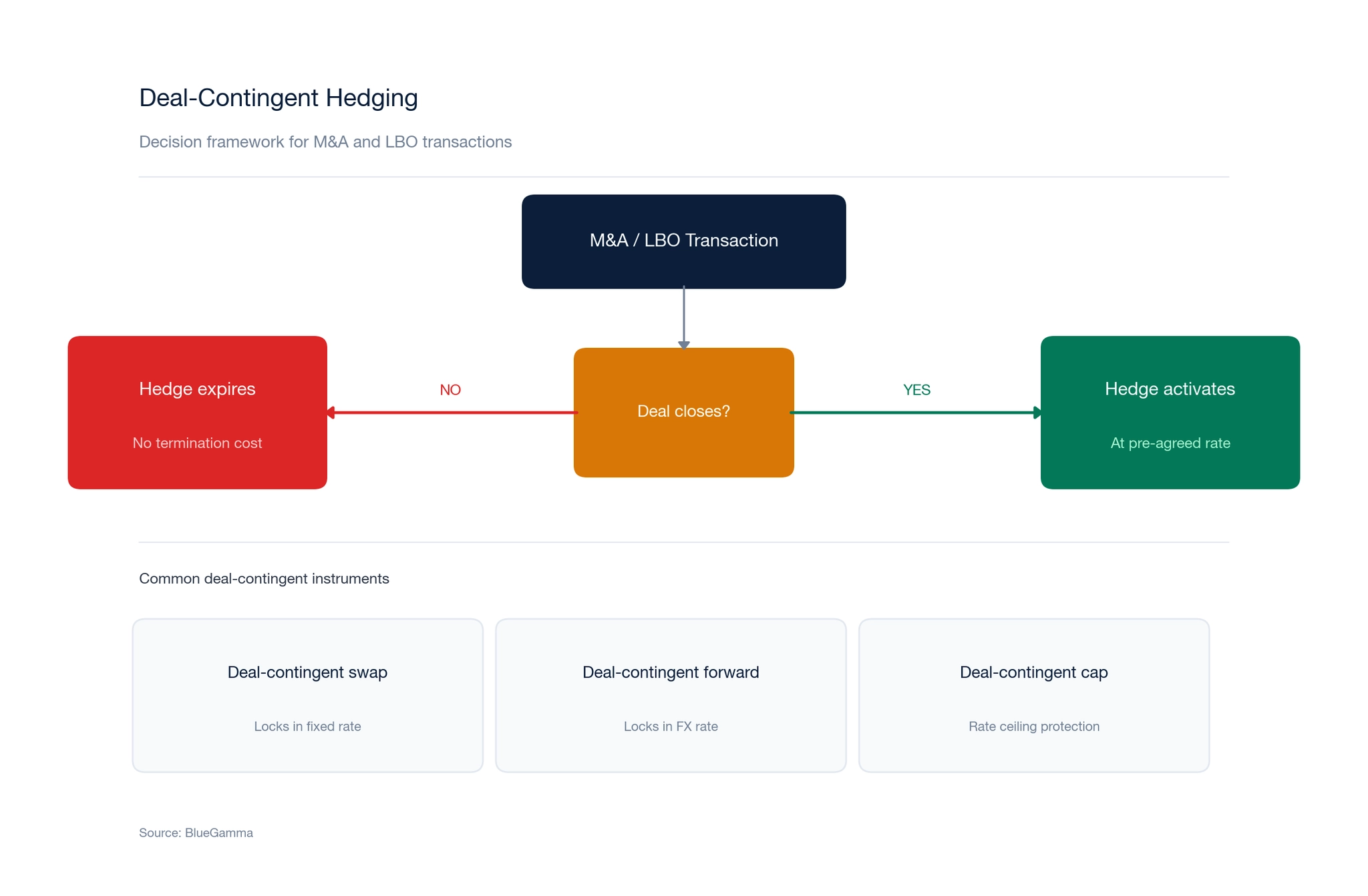

A deal-contingent hedge is a derivative contract whose activation is conditional on the successful completion of a specified transaction, typically a merger, acquisition, or leveraged buyout. If the deal closes, the hedge takes effect at pre-agreed terms. If the deal fails, the hedge expires with no termination cost to the hedging party.

This structure addresses a fundamental problem in M&A: the borrower needs to lock in financing costs before the deal closes, but entering a standard hedge creates the risk of an expensive unwind if the transaction does not complete.

Why Deal-Contingent Hedging Exists

In a typical leveraged acquisition, several months may pass between signing and closing. Regulatory reviews, including antitrust clearance, can extend this timeline considerably. During this period, interest rates and exchange rates can move significantly. A private equity sponsor acquiring a company with $200 million in floating-rate debt faces material exposure: a 100 basis point move in rates could change annual debt service costs by $2 million.

The sponsor has three choices:

1. Do nothing and hedge after closing. This leaves the deal economics exposed to rate movements during the interim period. If rates rise sharply between signing and closing, the projected returns deteriorate.

2. Enter a standard hedge at signing. This locks in a rate immediately but creates a new risk: if the deal falls through, the sponsor must unwind the hedge at market value. Depending on rate movements, this could mean a substantial loss on a transaction that never occurred.

3. Enter a deal-contingent hedge. This provides rate certainty from signing, with the hedge activating only upon successful deal completion. The premium is higher than a standard hedge, but the downside in a failed deal is limited to the premium paid.

Types of Deal-Contingent Hedges

Deal-Contingent Swap

A deal-contingent interest rate swap locks in a fixed rate on the acquisition financing. The swap terms (notional, tenor, fixed rate) are agreed at signing but the swap only becomes effective upon deal completion.

For example, a sponsor acquiring a company with a $150 million, 5-year floating-rate term loan could enter a deal-contingent swap at the current 5-year SOFR swap rate of approximately 3.59%. If the deal closes three months later, the swap activates at 3.59% regardless of where rates have moved. If the deal fails, no swap exists and no unwind is required.

The premium for the deal-contingent feature is typically embedded in the fixed rate, which will be higher than the equivalent standard swap rate. The spread over the standard rate reflects the optionality: the deal-contingent swap is effectively a standard swap plus a swaption that allows the hedger to walk away.

Deal-Contingent Forward

A deal-contingent FX forward locks in an exchange rate for the currency conversion required at closing. This is common in cross-border M&A where the buyer's funding currency differs from the target's operating currency.

For instance, a UK-based acquirer purchasing a European target for EUR 100 million would face EUR/USD or EUR/GBP exchange rate risk between signing and closing. With EUR/USD currently at 1.1698 spot and the 6-month forward at 1.1787 (a 0.76% forward premium), a deal-contingent forward would lock in a rate near 1.1787 that activates only upon completion.

Deal-Contingent Cap

A deal-contingent interest rate cap provides a ceiling on the borrower's floating rate exposure, activating upon deal completion. This structure is used when the borrower wants upside participation if rates fall but protection against a significant rise.

The cap premium is paid upon deal completion, not at signing. This is particularly attractive for sponsors who do not want to deploy capital on a hedge before the deal is certain.

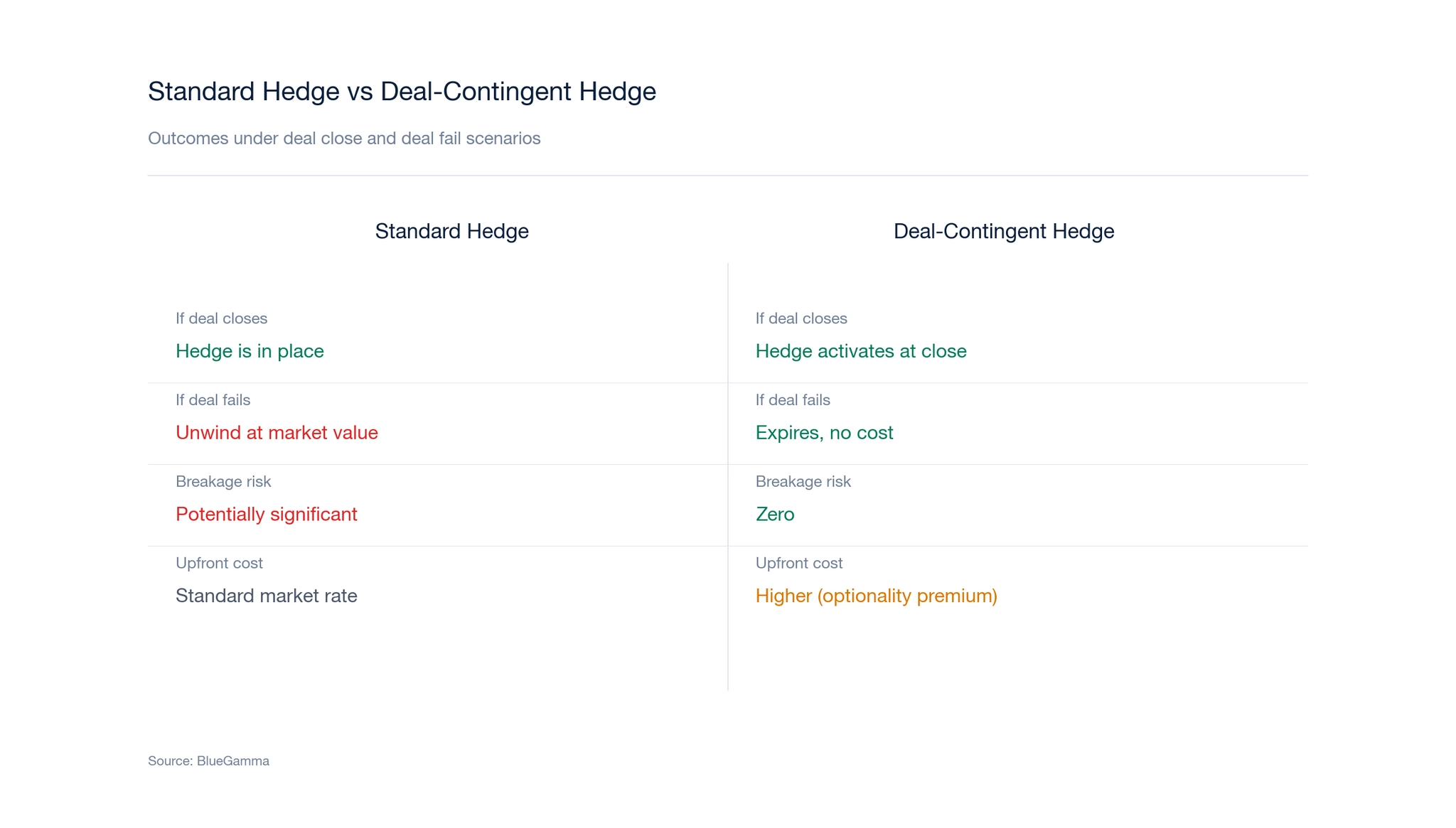

Deal-Contingent vs. Standard Hedge

| Feature | Standard Hedge | Deal-Contingent Hedge |

|---|---|---|

| Rate Lock | Immediate from trade date | From signing, activates at close |

| If Deal Closes | Hedge is in place | Hedge activates at pre-agreed terms |

| If Deal Fails | Must unwind at market value (potential loss) | Hedge expires, no cost beyond premium |

| Cost | Standard swap rate or cap premium | Higher rate or premium (reflects optionality) |

| Counterparty Risk | Standard bilateral | Provider takes deal completion risk |

| Typical Premium | N/A | 10-50 bps over standard hedge, depending on deal certainty and tenor |

How Deal-Contingent Hedges Are Priced

The premium for a deal-contingent hedge reflects three primary factors:

Deal completion probability. The higher the likelihood of completion, the lower the premium. A deal with regulatory approval already obtained will price tighter than one still facing antitrust review or other regulatory hurdles. Providers typically assess deal certainty through their own due diligence and may require representations from the sponsor.

Time to closing. Longer signing-to-closing periods increase the premium because the provider bears market risk for a longer duration without knowing whether the hedge will activate.

Market volatility. Higher interest rate or FX volatility increases the optionality value of the deal-contingent feature, driving up the premium. In the current environment, with SOFR swap rates ranging from 3.55% (3-year) to 3.59% (5-year), the cost of this optionality depends on the vol surface and the expected closing timeline.

Notional amount and tenor. Larger notionals and longer tenors carry more risk for the provider, increasing the premium.

The pricing is typically done by the provider's structuring desk using a combination of swaption models (for the rate optionality) and a probability-weighted model (for the deal completion risk).

Steps to Implement a Deal-Contingent Hedge

1. Define the hedging requirement

Identify the exposure: what notional amount needs hedging, in what currency, for what tenor, and against which risk (interest rate, FX, or both). Align these parameters with the financing term sheet.

2. Engage providers early

Deal-contingent hedges are offered by a limited number of banks and specialist providers. Engage at least two to three counterparties during the financing process to ensure competitive pricing. Not all banks offer deal-contingent structures, as they require the provider to take deal completion risk.

3. Agree terms and triggers

Define the precise conditions under which the hedge activates. The trigger is typically the funding date of the acquisition financing. In transactions where antitrust approval or other regulatory conditions may delay closing, the longstop date should provide sufficient buffer. Ensure the trigger definition is clear and aligned between the hedge provider and the lending group.

4. Execute documentation

Deal-contingent hedges are documented under standard ISDA agreements with additional provisions covering the contingent activation. The documentation should address what constitutes deal completion, the notification process, and the treatment of material adverse changes.

5. Monitor rates between signing and closing

Even with a deal-contingent hedge in place, the sponsor should monitor market rates to understand how the hedge is performing relative to current market levels. This is relevant for assessing the deal's overall economics and for discussions with lenders.

BlueGamma's real-time swap rate dashboard enables sponsors and their advisors to track hedging levels continuously between signing and closing. The platform provides live SOFR, EURIBOR, and SONIA swap rates across all tenors, accessible through the web app, Excel add-in, and API.

6. Activate or expire

Upon deal completion, notify the hedge provider per the agreed process. The hedge activates at the pre-agreed terms. If the deal does not complete by the specified longstop date, the hedge expires automatically.

Key Considerations

Provider selection. The deal-contingent hedge provider need not be the same as the lending bank, although there are often practical advantages to using a lender who already has visibility on the deal timeline and completion conditions.

Interaction with financing. Ensure the hedge terms are consistent with the financing documentation, particularly around notional amounts, amortisation schedules, and the reference rate (e.g., Term SOFR vs. Daily SOFR).

Accounting treatment. Deal-contingent hedges present unique accounting considerations. Hedge accounting designation typically cannot begin until the hedge activates, since the hedged item (the acquisition debt) does not exist until closing. Borrowers should consult their auditors on the transition to hedge accounting post-completion.

Break clauses. Some deal-contingent structures include partial activation clauses for deals that close at a reduced size, or extension provisions if the closing is delayed beyond the original timeline.

Summary

Deal-contingent hedging provides a mechanism to lock in interest rates or exchange rates for M&A transactions without the risk of unwinding costs if the deal fails. The premium over standard hedging reflects the optionality provided to the borrower.

With current 5-year SOFR swap rates at 3.59% and 7-year rates at 3.68%, deal-contingent structures are particularly relevant for sponsors looking to provide rate certainty to investment committees and lenders during the signing-to-closing period.

The choice between a deal-contingent swap, forward, or cap depends on the nature of the underlying exposure and the sponsor's risk appetite.

This article is for informational and educational purposes only and does not constitute financial, investment, legal, or tax advice. BlueGamma does not provide advisory services. Readers should consult qualified professional advisors before entering into any derivative transaction. Market data shown is indicative and sourced from BlueGamma as of the date stated.

Frequently Asked Questions

What is a deal contingent hedge?

A deal contingent hedge is a derivative contract that becomes effective only upon the successful completion of a specified transaction, such as a merger, acquisition, or leveraged buyout. If the deal closes, the hedge activates at pre-agreed terms. If the deal fails, the hedge expires with no termination cost beyond any premium paid. This structure is used primarily by private equity sponsors and corporate acquirers to manage rate risk during the signing-to-closing period.

How is a deal contingent swap priced?

A deal contingent swap is priced as a standard interest rate swap plus a premium that reflects the optionality of cancellation if the deal fails. The premium, typically 10 to 50 basis points over the standard swap rate, depends on the assessed probability of deal completion, time to closing, market volatility, and notional size. Providers use a combination of swaption pricing models and probability-weighted deal completion analysis.

What is a deal contingent forward?

A deal contingent forward is an FX forward contract that locks in an exchange rate for the currency conversion required at deal closing. Like other deal-contingent instruments, it activates only upon successful completion of the transaction. This is particularly common in cross-border M&A where the buyer's funding currency differs from the target's operating currency.

When should you use deal contingent hedging?

Deal contingent hedging is appropriate when there is material interest rate or FX exposure during the period between signing and closing, and when there is meaningful risk that the transaction may not complete. It is most commonly used in leveraged buyouts by private equity firms, cross-border acquisitions with extended regulatory approval timelines, and transactions involving bridge loans that will be refinanced with permanent financing post-close.