What Is a Swaption?

A swaption (short for "swap option") is an option that gives the holder the right — but not the obligation — to enter into an interest rate swap at a future date. The buyer pays a premium (the option's net present value) upfront for this right.

There are two types:

- A payer swaption gives the right to pay a fixed rate and receive a floating rate. It benefits the holder when interest rates rise above the strike.

- A receiver swaption gives the right to receive a fixed rate and pay a floating rate. It benefits the holder when interest rates fall below the strike.

Think of it this way: if you're a borrower worried that rates will rise before you close on a loan, a payer swaption lets you lock in a worst-case fixed rate today while keeping the flexibility to walk away if rates fall.

| Payer Swaption | Receiver Swaption | |

|---|---|---|

| Right granted | Pay fixed, receive floating | Receive fixed, pay floating |

| Benefits when | Rates rise above the strike | Rates fall below the strike |

| Typical buyer | Borrower hedging future debt | Investor protecting fixed income |

| Analogous to | A call on rates | A put on rates |

How Do Swaptions Work?

A swaption is defined by two time dimensions: the option expiry (when the holder decides whether to exercise) and the underlying swap tenor (the length of the swap that begins if exercised). Market convention expresses this as expiry × tenor — for example, "2Y×5Y" means the option expires in 2 years, and if exercised, the holder enters a 5-year swap.

The key terms of a swaption are:

- Strike rate — the fixed rate of the underlying swap

- Expiry date — when the option can be exercised

- Underlying tenor — the length of the swap post-exercise

- Premium (NPV) — the upfront cost of the option

- Notional — the size of the underlying swap

Exercise Styles

Swaptions come in three exercise styles:

| Style | When Exercisable | Common Use |

|---|---|---|

| European | Only on the expiry date | Most liquid, standard interbank market |

| Bermudan | On a set of predetermined dates | Callable bond hedging, structured products |

| American | Any date up to and including expiry | Rare in practice for interest rate swaptions |

European swaptions are by far the most commonly traded and are the standard in the interbank market. When people refer to "swaption pricing" without qualification, they typically mean European-style.

Payer vs Receiver Swaptions

The choice between a payer and receiver swaption depends on the direction of rate risk you want to hedge.

Payer Swaption — Hedging Rising Rates

A payer swaption is used when a borrower or issuer wants to protect against rates rising before they lock in financing. For example, a corporate treasurer expecting to issue fixed-rate debt in 18 months might buy a payer swaption today. If rates rise, the swaption pays out, offsetting the higher borrowing cost. If rates fall, the treasurer lets the option expire and borrows at the lower market rate.

Receiver Swaption — Hedging Falling Rates

A receiver swaption is used when an investor or lender wants to protect against rates falling. For example, a pension fund receiving fixed income might buy a receiver swaption to ensure they can reinvest at an acceptable rate. If rates drop, the swaption compensates for the lower reinvestment yield.

Payoff at Expiry

At expiry, the swaption's intrinsic value depends on the difference between the strike rate and the prevailing forward swap rate:

- Payer swaption payoff ≈ max(Forward Rate − Strike, 0) × Annuity × Notional

- Receiver swaption payoff ≈ max(Strike − Forward Rate, 0) × Annuity × Notional

Before expiry, the option also has time value — driven by volatility and time remaining — which is why the premium (NPV) is typically higher than the intrinsic value alone.

When Are Swaptions Used?

Swaptions are widely used across corporate treasury, project finance, and portfolio management. Common use cases include:

- Pre-hedging future debt issuance — A borrower buys a payer swaption to lock in a maximum rate for a loan that hasn't closed yet. This is common in project finance where there's a gap between mandate and financial close.

- Rate lock protection — Before a bond issuance or refinancing, issuers use swaptions to cap their worst-case cost of funds while retaining upside if rates fall.

- Portfolio insurance — Fixed-income portfolio managers use receiver swaptions to protect against falling yields eroding portfolio income.

- Volatility trading — Traders express views on rate volatility using swaption straddles (buying both a payer and receiver at the same strike) without taking a directional rate view.

The swaption market is one of the largest options markets globally. According to the Bank for International Settlements, interest rate options (including swaptions) had a notional outstanding of over $45 trillion as of mid-2024.

Swaption Pricing Explained

European swaptions are most commonly priced using the Bachelier (normal) model, which has largely replaced the Black (lognormal) model in the post-LIBOR era. The key advantage of the Bachelier model is that it works correctly when rates are low or negative — something the Black model cannot handle due to its reliance on the logarithm of rates.

The Bachelier model prices a payer swaption as:

Where:

- F = Forward swap rate (the at-the-money rate for the underlying swap)

- K = Strike rate

- σ = Normal (Bachelier) volatility

- T = Time to expiry in years

- Φ(d) = Cumulative normal distribution

- φ(d) = Standard normal density

- d = (F − K) / (σ × √T)

The key inputs that drive a swaption's price are the forward rate (where the market expects the swap rate to be at expiry), the strike (what rate you're locking in), the normal volatility (how much the market expects rates to move), and time to expiry (more time = more uncertainty = higher premium).

Normal volatility is typically quoted in basis points (e.g., 115 bps means the market implies roughly ±1.15% annual rate moves). This differs from Black (lognormal) volatility, which is quoted as a percentage of the rate level.

Swaption Pricing Example

Let's walk through pricing a real swaption using the SOFR curve.

Example 1: ATM Payer Swaption (2Y×5Y SOFR)

We'll price a 2-year into 5-year at-the-money payer swaption on SOFR with a $10 million notional. "At-the-money" means the strike equals the current forward swap rate — so we're not specifying a strike and letting the market set it.

import requests

API_KEY = "your_api_key_here"

BASE_URL = "https://api.bluegamma.io/v1"

headers = {

"x-api-key": API_KEY,

}

response = requests.get(

f"{BASE_URL}/swaption_price",

headers=headers,

params={

"index": "SOFR",

"start_date": "2Y",

"maturity_date": "5Y",

"notional": 10000000

}

)

print(response.json())Response:

{

"index": "SOFR",

"currency": "USD",

"swaption_type": "payer",

"start_date": "2028-02-25",

"maturity_date": "2033-02-25",

"exercise_date": "2028-02-25",

"valuation_time": "2026-02-25T10:50:39Z",

"notional": 10000000,

"forward_rate": 3.30,

"strike_rate": 3.30,

"normal_volatility_bps": 76.1,

"npv": 96709.00,

"dv01": 2850.00,

"vega": 1271.60

}

Here's what each field tells us:

| Field | Value | What It Means |

|---|---|---|

| forward_rate | 3.30% | The market-implied 5Y swap rate starting in 2 years |

| strike_rate | 3.57% | Equal to forward (ATM) since we didn't specify a strike |

| normal_volatility_bps | 76.1 bps | Normal (Bachelier) vol — implies ~1.15% annual rate moves |

| npv | $96,709 | The option premium — what you'd pay for this swaption |

| dv01 | $2,850 | Exactly 0.5 for an ATM payer (50% implied exercise probability) |

| vega | $1,271 | NPV change per 1bp move in normal_volatility_bps |

The premium of $206,000 represents about ~0.97% of notional — the cost of protecting against rates rising above 3.57% over the next 2 years.

Example 2: OTM Receiver Swaption

Now let's price a receiver swaption with a strike of 3.0% — below the forward rate of 3.57%, making it out-of-the-money.

response = requests.get(

f"{BASE_URL}/swaption_price",

headers=headers,

params={

"index": "SOFR",

"start_date": "2Y",

"maturity_date": "5Y",

"strike_rate": 3.0,

"swaption_type": "receiver",

"notional": 10000000

}

)Response:

{

"index": "SOFR",

"currency": "USD",

"swaption_type": "receiver",

"start_date": "2028-02-25",

"maturity_date": "2033-02-25",

"exercise_date": "2028-02-25",

"valuation_time": "2026-02-25T10:50:39Z",

"notional": 10000000,

"forward_rate": 3.30,

"strike_rate": 3.0,

"normal_volatility_bps": 76.1,

"npv": 85000.00,

"dv01": -1710.00,

"vega": 1100.00

}The NPV stays $85,000 — the strike (3.0%) is below the forward rate (3.57%), so the receiver swaption is less likely to be exercised. The dv01 of -$1,710 implies roughly a 30% probability of exercise.

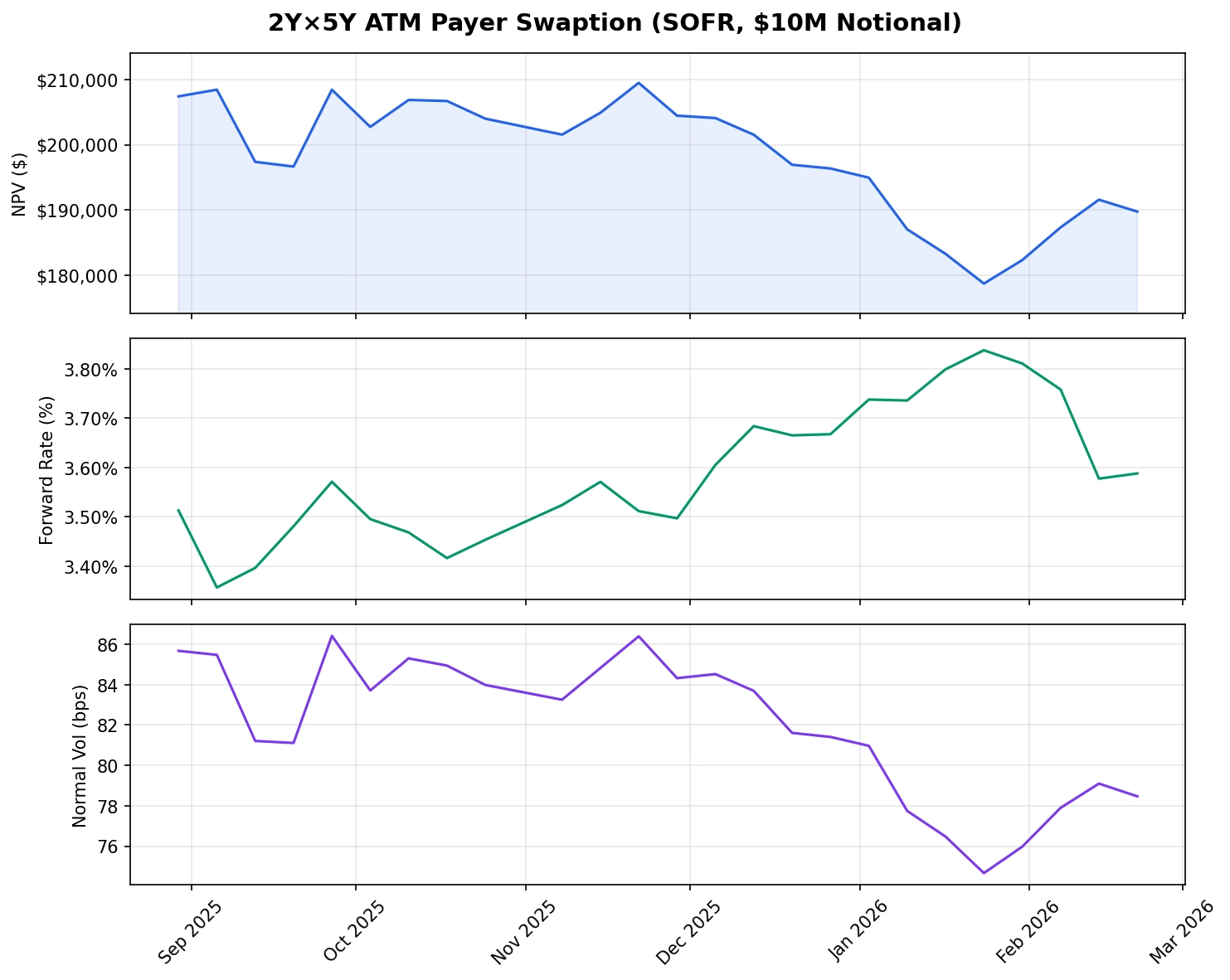

How Swaption Values Change Over Time

A swaption's value doesn't stay static — it moves daily as the yield curve and volatility environment shift. The chart below shows how a 2Y×5Y ATM SOFR payer swaption (with $10M notional) was valued weekly over the past six months:

Two things drive these movements:

- Forward rate changes — When the 5-year forward swap rate rises, the underlying swap becomes more valuable, pushing the ATM swaption premium higher.

- Volatility regime — When market uncertainty increases (normal vol rises), the option premium increases because there's a wider range of possible rate outcomes at expiry.

This kind of historical analysis is useful for P&L attribution (understanding what drove your swaption's value change), back-testing hedging strategies, and timing swaption purchases relative to volatility cycles.

Understanding Swaption Risk Sensitivities: DV01 and Vega

When trading or risk-managing swaptions, two Greeks matter most: DV01 and Vega.

DV01— Rate Sensitivity

DV01 is the NPV sensitivity to a 1bp parallel shift in the underlying swap rate (in currency units). Payer swaption DV01 is positive (gains value when rates rise), receiver is negative (gains value when rates fall).

At-the-money, the swaption DV01 is approximately half of the underlying swap’s PV01. To delta-hedge, you enter a swap whose PV01 offsets the swaption DV01. It’s no longer described as a probability proxy.

Vega — Volatility Sensitivity

Vega measures the NPV change per 1 basis point shift in normal volatility. A vega of $6,100 means that if implied vol rises by 1bp, the swaption's value increases by approximately $6,100.

Vega is highest for at-the-money swaptions and decreases as the option moves deeper in or out of the money. It also increases with time to expiry — longer-dated swaptions have more vega because there's more time for volatility to play out.

| Greek | What It Measures | ATM Payer Value (2Y×5Y, $10M) | Practical Use |

|---|---|---|---|

| DV01 | Swap rate sensitivity / 1bp | ~$2,850 | Hedge ratio vs underlying swap |

| Vega | Vol sensitivity / 1bp | ~$1,271 | Vol risk management, P&L attribution |

Pricing Swaptions with the BlueGamma API

The examples above were generated using BlueGamma's /swaption_price endpoint, which prices European payer and receiver swaptions using a Bachelier model with live yield curves and volatility data.

The endpoint supports 20+ indices including SOFR, SONIA, EURIBOR, SARON, and more — so you can price swaptions across major currencies in a single API call. Inputs are straightforward: specify the index, exercise date, swap maturity, and optionally a strike rate and notional.

POST https://api.bluegamma.io/v1/swaption_priceContent-Type: application/json

x-api-key: your_api_key{"index":"SOFR","start_date":"2Y","maturity_date":"5Y","swaption_type":"payer"}The API returns the forward rate, strike, normal volatility (in basis points), NPV, dv01, and vega — everything you need for pricing, hedging, and risk reporting.

For the full request/response schema, see the interactive API reference. For a step-by-step walkthrough with more examples, see our API guide for swaption pricing. To get started, book a call with our team or email support@bluegamma.io.