BlueGamma Research | October 2025

By the BlueGamma Interest Rate Strategy Team

The UK interest rate market has undergone a profound structural repricing over the past twelve months, with the SONIA forward curve shifting 50-90 basis points higher across all tenors. Our analysis of September 2025 market data reveals three critical developments that challenge the prevailing narrative of imminent policy normalization:

Key Takeaways:

- Curve Steepening Reflects Structural Concerns: The 2s10s spread has widened 62 bps year-over-year (from -24 bps to +38 bps), with 10-year swaps rising 54 bps to 4.15% while 2-year rates declined 8 bps to 3.77%. This divergence signals market skepticism about the BoE's ability to sustainably lower rates without reigniting inflation.

- Exceptional Volatility Indicates Policy Uncertainty: 5-year swap rates exhibited a 72 bps trading range in 2025 (3.61% - 4.33%), the widest annual range since 2022. This volatility reflects genuine market uncertainty about the inflation trajectory and the appropriate terminal rate.

- "Higher for Longer" Now Embedded in Forwards: The forward curve prices 3-month rates at 4.10% by 2030 and 4.91% by 2035—substantially higher than the 3.48% and 4.00% respectively priced in September 2024. This 90 bps repricing of long-term expectations suggests markets view elevated inflation as more persistent than previously anticipated.

Bottom Line: We expect the BoE to maintain a cautious stance through Q4 2025, with the first rate cut likely delayed until Q1 2026. However, the magnitude and pace of subsequent easing will be constrained by fiscal pressures and sticky inflation dynamics. Our base case sees Bank Rate ending 2026 at 4.00%, well above the 3.25% priced in markets a year ago.

I. Market Overview: A Year of Repricing

Current Rate Landscape (as of September 30, 2025)

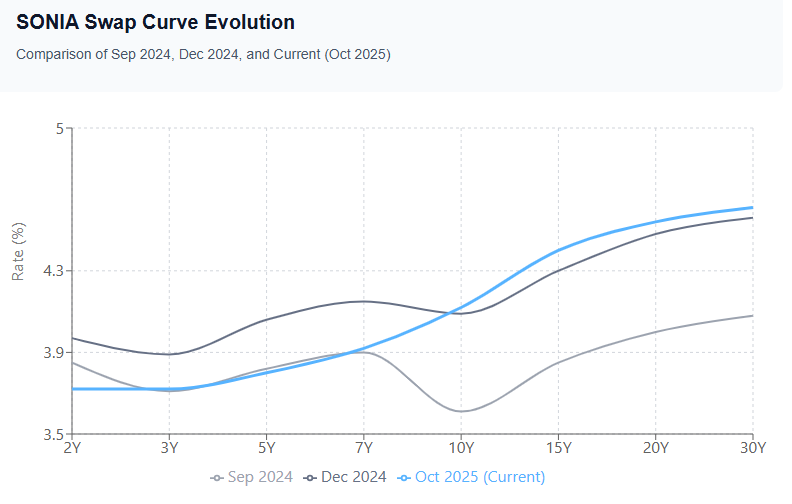

The UK rates market closed September with SONIA fixing at 3.97%, reflecting the BoE's continued restrictive stance. The swap curve exhibits notable steepening compared to both year-end 2024 and September 2024:

| Tenor | Sep 2025 | Sep 2024 | Change (bps) | Dec 2024 | Change from Dec (bps) |

|---|---|---|---|---|---|

| 2Y | 3.77% | 3.85% | -8 | 3.97% | -20 |

| 5Y | 3.84% | 3.82% | +2 | 4.06% | -22 |

| 10Y | 4.15% | 3.61% | +54 | 4.09% | +6 |

| 30Y | 4.63% | 4.08% | +55 | 4.56% | +7 |

Figure 1: SONIA Swap Curve Evolution

The current curve structure reveals several important dynamics:

Front-End Anchoring: Short-dated swaps (< 2Y) remain tightly anchored to current policy expectations, with the market pricing approximately 25 bps of cumulative easing by end-2026.

Mid-Curve Inflection: The 3-7 year sector has become the key battleground, with rates reflecting the tension between near-term easing expectations and medium-term inflation concerns.

Long-End Premium: Rates beyond 10 years have repriced significantly higher, suggesting elevated long-term inflation risk premium and concerns about fiscal sustainability.

FX Market Context

Sterling has maintained relative stability through this repricing:

- GBP/USD: 1.344 (vs 1.345 in Sep 2024)

- GBP/EUR: 1.146 (vs 1.155 in Sep 2024)

The modest EUR strength reflects diverging policy expectations, with the ECB viewed as closer to its terminal rate than the BoE.

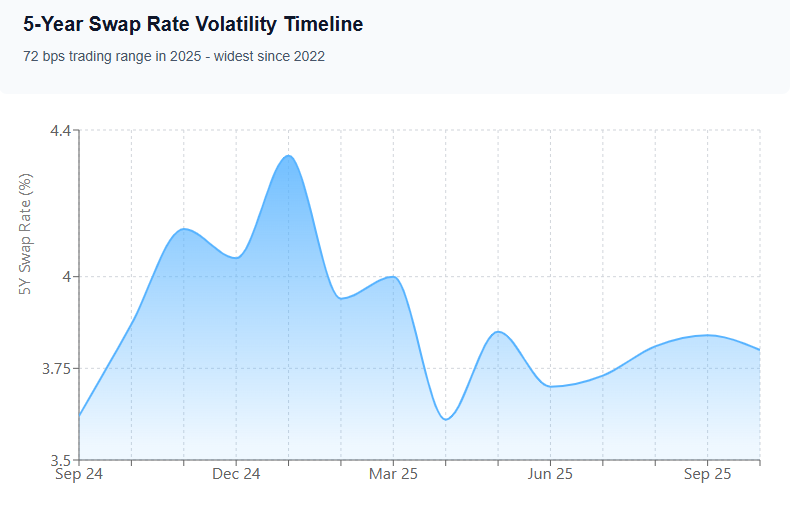

II. The Volatility Story: Markets Struggle to Find Equilibrium

Q1 2025: Inflation Fears Drive Rates Higher

The year began with persistent inflation concerns driving a sharp repricing higher. 5-year swap rates peaked at 4.33% on January 14, reflecting:

- Upside surprises in December 2024 CPI (4.2% YoY vs 4.0% expected)

- Stronger-than-expected wage growth (6.1% YoY)

- Services inflation remaining stubbornly elevated at 6.8%

The market rapidly repriced out multiple rate cuts, with the implied terminal Bank Rate rising from 3.75% to 4.50%. 10-year swaps rose in sympathy, touching 4.35%—the highest level since November 2023.

Key Driver: Concerns that the BoE's August 2024 rate cut (from 5.25% to 5.00%) had been premature, and that the bank would need to hold rates higher for longer to anchor inflation expectations.

Q2 2025: The Dovish Pivot

April brought a dramatic reversal. 5-year swaps plunged 72 bps from their January peak to 3.61% by April 30, driven by:

- March CPI surprising to the downside (3.1% vs 3.4% expected)

- BoE Governor Bailey's dovish testimony suggesting "significant progress" on inflation

- Weaker economic activity data, with Q1 GDP growth of just 0.1% QoQ

- Labor market showing signs of cooling, with unemployment rising to 4.6%

Markets aggressively priced in a cutting cycle, with forwards implying Bank Rate falling to 3.50% by end-2025.

Q3 2025: Reality Reasserts Itself

The summer months saw a partial retracement as inflation proved more persistent than the April optimism suggested:

- June CPI ticked higher to 3.4%

- Services inflation remained elevated at 6.2%

- Wage growth remained above the BoE's 4% comfort level

- Fiscal concerns emerged as government borrowing exceeded forecasts

By September 30, 5-year swaps had stabilized at 3.84%—well off the April lows but below the January peak. This 72 bps annual trading range compares to:

- 45 bps in 2024

- 38 bps in 2023

- 215 bps in 2022 (exceptional due to mini-budget crisis)

Implication: The exceptional 2025 volatility signals genuine uncertainty about the inflation outlook and appropriate policy stance. Markets are grappling with conflicting signals: cooling growth but persistent inflation, improving headline CPI but stubborn services inflation, weak consumer confidence but resilient employment.

III. Forward Curve Analysis: The "Higher for Longer" Regime

Parallel Shift Higher Across All Tenors

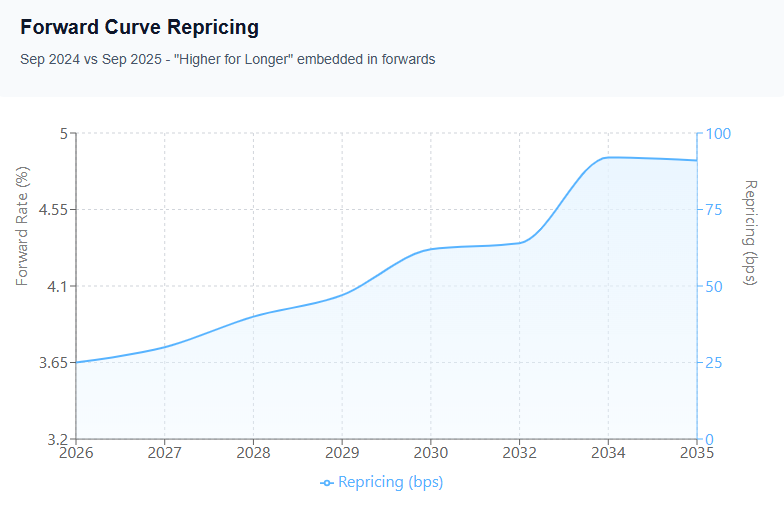

Perhaps the most significant development in 2025 has been the wholesale repricing of the forward curve. Comparing September 2025 to September 2024:

| Period | Sep 2024 Forward | Sep 2025 Forward | Change (bps) |

|---|---|---|---|

| Late 2026 | 3.36% | 3.61% | +25 |

| Late 2027 | 3.36% | 3.66% | +30 |

| Late 2028 | 3.36% | 3.76% | +40 |

| Late 2029 | 3.40% | 3.87% | +47 |

| Late 2030 | 3.48% | 4.10% | +62 |

| Late 2032 | 3.63% | 4.27% | +64 |

| Late 2034 | 3.86% | 4.78% | +92 |

| Late 2035 | 4.00% | 4.91% | +91 |

Figure 2: SONIA 3-Month Forward Curve Comparison

This parallel upward shift of 50-90 bps reveals several critical insights:

1. Terminal Rate Has Been Repriced Higher

A year ago, markets expected the BoE to ultimately settle at a "neutral" rate around 3.50%. Today, forwards imply a terminal rate closer to 4.00-4.25%. This 50-75 bps repricing reflects:

- Upward revision to inflation expectations: Markets now price long-term inflation closer to 2.5% vs. the 2.0% target

- Higher equilibrium rate: Structural factors (deglobalization, energy transition, fiscal expansion) suggest r* has risen

- Greater uncertainty premium: The volatility of recent years has increased the compensation markets demand for duration risk

2. Near-Term Easing Still Expected, But More Modest

The forward curve still slopes downward through 2026, implying the BoE will deliver cuts. However:

- September 2024 pricing: Implied 100 bps of cuts by end-2026

- September 2025 pricing: Implies just 40 bps of cuts by end-2026

This dramatic repricing suggests markets now expect:

- First cut delayed from Q4 2025 to Q1 2026

- Slower pace of cuts (one per quarter vs. one every meeting)

- Higher terminal rate (4.00% vs. 3.50%)

3. The 2027-2030 Period Is Key

The forward curve shows its steepest ascent from 2027-2030, with rates rising 44 bps over this period. This reflects market expectations that:

- Initial cuts will prove insufficient to durably lower inflation

- The BoE will need to reverse course and tighten again

- Structural inflation pressures will reassert themselves as the economy reaccelerates

This expectation of a policy reversal—cutting then tightening again—is reminiscent of the Fed's 1970s experience and signals deep skepticism about the BoE's ability to achieve a "soft landing."

4. Long-End Repricing Reflects Structural Concerns

The 90 bps repricing of 2035 forwards is particularly striking. At this horizon, cyclical factors fade and structural considerations dominate:

- Fiscal sustainability: UK debt/GDP projected to exceed 100%, raising questions about debt monetization

- Demographic headwinds: Aging population puts upward pressure on inflation and downward pressure on real rates

- Energy transition costs: The path to net zero involves substantial inflationary pressures

- Post-Brexit structural changes: Reduced labor mobility and trade frictions may elevate the inflation floor

Key Takeaway: The forward curve repricing is not merely about the next few BoE meetings. It represents a fundamental reassessment of the UK's long-term inflation dynamics and the appropriate level of interest rates in this new regime.

IV. Policy Implications: The BoE's Constrained Path

The Case for Near-Term Caution

We expect the BoE to maintain Bank Rate at 5.00% through end-2025, despite mounting political pressure to ease. Several factors support this view:

1. Inflation Remains Above Target

- Headline CPI at 3.2% (September), well above the 2.0% target

- Core CPI at 4.8%, showing limited progress

- Services inflation at 6.2%, indicating persistent domestic price pressures

2. Labor Market Resilience

- Unemployment at 4.6%, below the BoE's estimate of NAIRU (4.8%)

- Wage growth at 5.8% YoY, inconsistent with 2% inflation

- Job vacancies remain elevated at 950,000

3. Recent History Counsels Caution

- The August 2024 cut now looks premature given subsequent inflation dynamics

- The MPC cannot afford another policy error that damages credibility

- Markets are clearly skeptical, as evidenced by the forward curve repricing

4. Global Central Bank Positioning

- Fed maintaining restrictive stance longer than expected

- ECB also proceeding cautiously despite weaker European growth

- No major central bank has successfully navigated back to 2% inflation yet

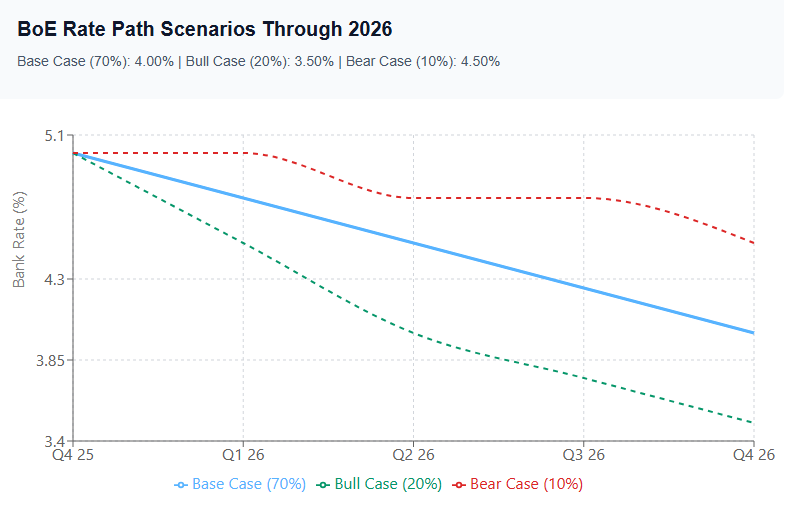

Forecast: The Path Through 2026

Base Case (70% probability):

- Q4 2025: Bank Rate maintained at 5.00%

- Q1 2026: First 25 bps cut to 4.75% (February meeting)

- Q2 2026: Second cut to 4.50% (May meeting)

- Q3-Q4 2026: Two additional cuts to 4.00%

- End-2026 Bank Rate: 4.00%

This path implies 100 bps of cumulative easing over five quarters—a deliberate, data-dependent approach.

Bull Case (20% probability): Faster disinflation allows more aggressive easing

- Inflation falls faster than expected due to demand weakness

- BoE delivers 150 bps of cuts, ending 2026 at 3.50%

- Triggers renewed sterling weakness and potential inflation rebound in 2027

Bear Case (10% probability): Persistent inflation forces extended pause

- Services inflation remains sticky above 5%

- BoE delivers only 50 bps of cuts, ending 2026 at 4.50%

- Raises recession risk in 2027 but preserves credibility

Risks to Our View

Upside Risks (Higher Rates):

- Fiscal expansion: Government spending programs prove more inflationary than expected

- Wage-price spiral: Inflation expectations become unanchored, forcing BoE to tighten

- Sterling weakness: GBP depreciation passes through to import prices

- Energy shock: Geopolitical developments drive renewed commodity inflation

Downside Risks (Lower Rates):

- Economic deterioration: Growth weakens sharply, forcing aggressive easing

- Credit event: Financial stability concerns override inflation mandate

- Disinflationary surprise: Structural factors (technology, demographics) drive inflation below target

- Global recession: Synchronized global downturn necessitates policy support

V. Trading Implications and Positioning

Recommended Strategies

1. Curve Steepeners

- Trade: Pay 2Y vs. receive 10Y

- Rationale: 2s10s at 38 bps appears too flat given policy uncertainty and term premium considerations

- Target: 60 bps (current Sep 2024 average)

- Stop: 25 bps

The forward curve repricing suggests markets have insufficiently priced medium-term inflation risks. Historical precedent suggests the curve should be steeper when:

- Policy uncertainty is elevated (72 bps volatility in 5Y rates)

- Inflation is above target (3.2% vs 2.0%)

- Central bank is near peak of tightening cycle

2. Short Duration in 5-10Y Sector

- Trade: Pay 5Y and 7Y swaps

- Rationale: Mid-curve most vulnerable to repricing if BoE easing disappoints

- Entry: 5Y at 3.84%, 7Y at 3.95%

- Target: 5Y to 4.00%, 7Y to 4.15%

The dramatic Q2 rally (5Y to 3.61%) has partially reversed, but rates remain below levels consistent with current inflation dynamics. The forward curve implies the BoE will cut to 3.60% then reverse course—a low-probability scenario that leaves mid-curve rates vulnerable.

3. Long-End Value Opportunity

- Trade: Receive 20-30Y swaps

- Rationale: Long-end repricing may have overshot near-term

- Entry: 30Y at 4.63%

- Target: Carry with potential for compression to 4.45-4.50%

The 55 bps repricing in 30Y rates appears to have adequately priced fiscal concerns and structural inflation risks. Further cheapening would require a material deterioration in fundamentals. Meanwhile, carry at 4.63% is attractive relative to expected inflation over this horizon.

4. Cross-Currency Opportunities

- Trade: Receive GBP vs. pay EUR in 5-10Y sector

- Rationale: Rate differential appears excessive given similar inflation dynamics

- Entry: GBP 5Y at 3.84% vs. EUR 5Y at 2.45% (139 bps differential)

- Target: Differential compression to 120 bps

The UK/EU rate differential has widened to 139 bps (from 110 bps in September 2024) despite similar inflation challenges. While Brexit factors and fiscal concerns justify some premium, 139 bps appears excessive, particularly if the ECB maintains restrictive policy longer than currently priced.

Hedging Considerations

For Asset Managers:

- Curve steepening provides natural hedge against duration extensions

- Consider dynamic hedging that increases long-end exposure if rates reach 4.75-5.00% on 10Y

- Maintain flexibility for potential policy errors (either direction)

For Corporate Treasurers:

- Current environment favors locking in floating-to-fixed swaps in 3-5Y sector

- Rates around 3.80-3.90% represent reasonable hedging levels relative to historical ranges

- Consider callable structures to maintain optionality if rates move higher

For Liability-Driven Investors:

- Long-end rates at 4.50-4.70% provide attractive hedging opportunities for pension funds

- Consider layering in hedges over next 6-12 months rather than attempting to time bottom

- Focus on liability matching rather than rate speculation

VI. Looking Ahead: Key Factors to Monitor

Near-Term Catalysts (Q4 2025)

1. November CPI Release (Mid-November)

- Consensus: 3.1% YoY (vs 3.2% in September)

- Core: 4.6% YoY (vs 4.8% in September)

- Market Impact: Further disinflation could trigger rally in 2-5Y sector

2. November BoE Meeting (November 7)

- Expected: Rates held at 5.00%

- Focus: Updated inflation forecasts and forward guidance

- Key Risk: Any dovish language could trigger sharp curve flattening

3. Autumn Budget (Late November)

- Potential fiscal expansion or tax changes

- Implications for gilt supply and inflation outlook

- Market Impact: Fiscal concerns could pressure long-end

4. December Employment Report (Mid-December)

- Key metric: Wage growth (currently 5.8% YoY)

- Target: Need to see trend toward 4.0% for confidence in easing

- Market Impact: Wage dynamics critical for Q1 2026 policy decision

Medium-Term Factors (2026)

1. U.S. Policy Evolution

- Fed's path will influence BoE's degrees of freedom

- USD strength could pressure GBP and import inflation

- Watch for policy divergence (Fed tightening while BoE eases)

2. Brexit Adjustments

- Ongoing trade friction and labor market impacts

- Potential for new arrangements to ease supply constraints

- Long-term structural implications still unfolding

3. Energy Markets

- Oil prices and natural gas supply remain wild cards

- Energy transition costs feeding through to consumer prices

- Government energy subsidies may need to be unwound

4. Financial Stability

- UK property market showing signs of stress

- Commercial real estate concerns

- Banking sector resilience to sustained higher rates

VII. Conclusion: A New Regime Emerges

The past year has witnessed a fundamental repricing of UK interest rate expectations. The 50-90 bps parallel shift higher in the forward curve represents more than a cyclical adjustment—it signals a regime change in how markets view inflation dynamics, policy credibility, and the appropriate level of interest rates.

Three conclusions emerge:

First, the era of ultra-low rates is definitively over. Markets now price long-term rates near 5%, compared to pre-pandemic averages around 1.5-2.0%. This reflects structural shifts: deglobalization, fiscal expansion, energy transition costs, and demographic pressures all point to a higher inflation regime.

Second, policy credibility remains fragile. The exceptional volatility in 2025 (72 bps range on 5Y swaps) reveals market skepticism about the BoE's ability to orchestrate a smooth return to 2% inflation. The premature August 2024 cut damaged credibility; rebuilding it will require a sustained period of restrictive policy and patient, data-dependent decision-making.

Third, the path back to neutral will be longer and more uncertain than markets anticipated a year ago. The forward curve's repricing—from expecting Bank Rate at 3.25% by end-2026 to now pricing 4.00%—reflects growing recognition that inflation will prove persistent and the terminal rate has risen structurally.

For investors, this environment demands active management. The curve offers opportunities for those willing to take views on the pace of BoE easing, the evolution of term premium, and relative value across tenors. Our base case sees 100 bps of easing through 2026, but with significant two-way risks.

For policymakers, the message is clear: markets are demanding proof that inflation can be durably brought back to target. Premature easing risks a repeat of the 1970s policy errors. The BoE must prioritize credibility over political pressure, accepting near-term growth weakness as the price of medium-term stability.

The coming year will be critical in determining whether the UK can successfully navigate back to price stability or whether the current inflation episode becomes entrenched. The forward curve's message is unambiguous: markets are betting on "higher for longer"—and the BoE would do well to heed this signal.

About BlueGamma

BlueGamma is the default choice for interest rate data, providing institutional investors, corporates, and financial institutions with real-time access to comprehensive curve data, forward rates, and historical analytics across all major rate indices. Our API delivers the same quality data trusted by leading global institutions, with seamless integration and 24/7 support.

Contact: support@bluegamma.io | www.bluegamma.io