Looking for Term SOFR Data?

Access current and historical Term SOFR data with ease, updated daily.

Easily access 1/3/6/12 Month data

Plug the data into your model with ease

No queues, Always available

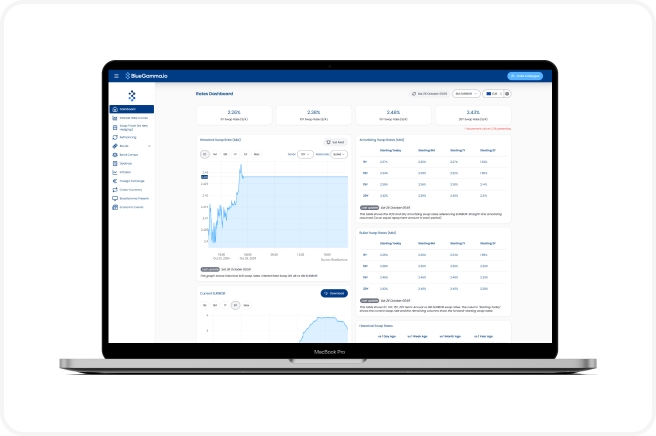

The fastest way to access Term SOFR data

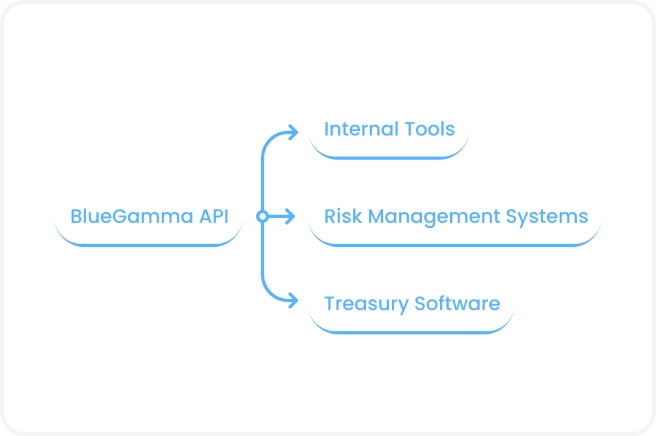

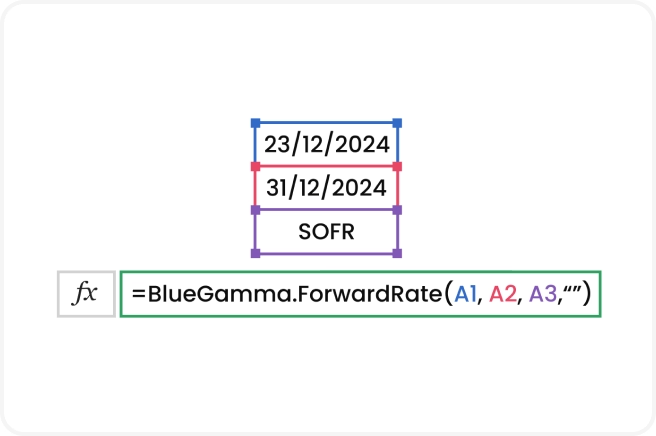

Get interest rate curves, swap rates, term tenors and more via Web Platform, API or Excel Add-in.

Real-time access to the data on-demand.

Seamlessly integrate the data into your software.

Pull the data directly into your spreadsheets.

Term SOFR vs Compounded SOFR

Compounded SOFR

Term SOFR

Both are based on SOFR but serve different purposes: Term SOFR provides predictability, while Compounded SOFR reflects realised market costs.

Trusted by

financial modellers

funds, advisors and IPPs

of models powered by BlueGamma

Team Access

Multiple users, one platform

Flexible Seat Based Pricing

One licence, every analyst

No more "queuing for the single terminal"

Log in from any laptop, pull the numbers, move on

The complete rates toolkit

Forward Curves

Swap Pricing

FX Forwards

Inflation Forecasts

Bond Yields & Ratings

FAQs

What is Term SOFR?

How is Term SOFR calculated?

Who administers and publishes Term SOFR?

When is Term SOFR published?

Is Term SOFR an officially endorsed rate?

Term SOFR vs. Compounded SOFR, What is the difference?

Daily Simple SOFR vs. Term SOFR

What types of financial products use Term SOFR?

How does Term SOFR compare to LIBOR?

What is adjusted term SOFR?

More from BlueGamma

SOFR Forward Curve

Access the latest SOFR forward curve data and forecasts.

SONIA Forward Curve

Access the latest SONIA forward curve data and forecasts.

EURIBOR Forward Curve

Access the latest EURIBOR forward curve data and forecasts.

BBSW Forward Curve

Access the latest BBSW forward curve data and forecasts.

CORRA Forward Curve

Access the latest CORRA forward curve data and forecasts.

SARON Forward Curve

Access the latest SARON forward curve data and forecasts.

TONA Forward Curve

Access the latest TONA forward curve data and forecasts.

HIBOR Forward Curve

Access the latest HIBOR forward curve data and forecasts.

WIBOR Forward Curve

Access the latest WIBOR forward curve data and forecasts.

BKBM Forward Curve

Access the latest BKBM forward curve data and forecasts.

STIBOR Forward Curve

Access the latest STIBOR forward curve data and forecasts.

NIBOR Forward Curve

Access the latest NIBOR forward curve data and forecasts.

CIBOR Forward Curve

Access the latest CIBOR forward curve data and forecasts.

EIBOR Forward Curve

Access the latest EIBOR forward curve data and forecasts.

JIBAR Forward Curve

Access the latest JIBAR forward curve data and forecasts.

PRIBOR Forward Curve

Access the latest PRIBOR forward curve data and forecasts.

MIBOR Forward Curve

Access the latest MIBOR forward curve data and forecasts.

SAIBOR Forward Curve

Access the latest SAIBOR forward curve data and forecasts.

BUBOR Forward Curve

Access the latest BUBOR forward curve data and forecasts.

TELBOR Forward Curve

Access the latest TELBOR forward curve data and forecasts.

TAIBOR Forward Curve

Access the latest TAIBOR forward curve data and forecasts.