Ready to integrate forward curves directly into your workflows? This guide will show you how to fetch forward rates using Python and the BlueGamma API.

Step 1: Set Up Your Environment

Before we begin, ensure that you have Python installed along with the requests and matplotlib libraries. If you don't have them yet, install them using:

pip install requests matplotlib

Step 2: Fetch SOFR Forward Rates

The /forward_rate endpoint in the BlueGamma API lets you fetch forward rates for specific start dates and tenors. Let's start with an example for a single date:

import requests

# API endpoint

url = "https://api.bluegamma.io/v1/forward_rate"

# Query parameters for a single forward rate

querystring = {

"index": "SOFR", # Reference rate

"start_date": "2025-06-30", # Start date

"end_date": "3M" # Fixed tenor of 3M

}

# API headers (replace 'YOUR_API_KEY' with your actual API key)

headers = {"X-Api-Key": "YOUR_API_KEY"}

# Fetch the forward rate

response = requests.get(url, headers=headers, params=querystring)

if response.status_code == 200:

data = response.json()

print("Forward Rate:", data["forward_rate"])

else:

print("Error:", response.status_code, response.text)

The script fetches the 3-month SOFR forward rate starting on 2025-06-30. The response includes the forward rate and other relevant details.

Step 3: Build a SOFR Forward Curve

Now, let's expand this to fetch forward rates for a set of pre-definded dates. By doing so, we'll plot a SOFR forward curve to visualise how the rate evolves over time.

import requests

import matplotlib.pyplot as plt

# API endpoint

url = "https://api.bluegamma.io/v1/forward_rate"

# Define predefined start dates (end of June and December each year)

start_dates = [

"2025-06-30", "2025-12-31",

"2026-06-30", "2026-12-31",

"2027-06-30", "2027-12-31",

"2028-06-30", "2028-12-31",

"2029-06-30", "2029-12-31",

"2030-06-30", "2030-12-31"

]

# Fixed tenor (3M)

tenor = "3M"

forward_rates = [] # To store forward rates

# API headers (replace 'YOUR_API_KEY' with your actual API key)

headers = {"X-Api-Key": "YOUR_API_KEY"}

# Fetch forward rates for each predefined start date

for start_date in start_dates:

querystring = {

"index": "SOFR", # Reference rate

"start_date": start_date, # Start of forward period

"end_date": tenor # Fixed tenor of 3M

}

response = requests.get(url, headers=headers, params=querystring)

if response.status_code == 200:

data = response.json()

forward_rates.append(data["forward_rate"]) # Append the forward rate

else:

print(f"Error fetching data for start date {start_date}: {response.status_code}")

forward_rates.append(None) # Add a placeholder for missing data

# Plot the 3M forward curve

plt.figure(figsize=(12, 6))

plt.plot(start_dates, forward_rates, marker='o', linestyle='-', color='blue', label='3M SOFR Curve')

# Customize the plot

plt.title('3M SOFR Forward Curve (2025-2030)', fontsize=16)

plt.xlabel('Start Date', fontsize=12)

plt.ylabel('Forward Rate (%)', fontsize=12)

plt.xticks(rotation=45) # Rotate x-axis labels for readability

plt.grid(True, linestyle='--', alpha=0.7)

plt.legend(fontsize=10)

plt.tight_layout()

# Display the graph

plt.show()

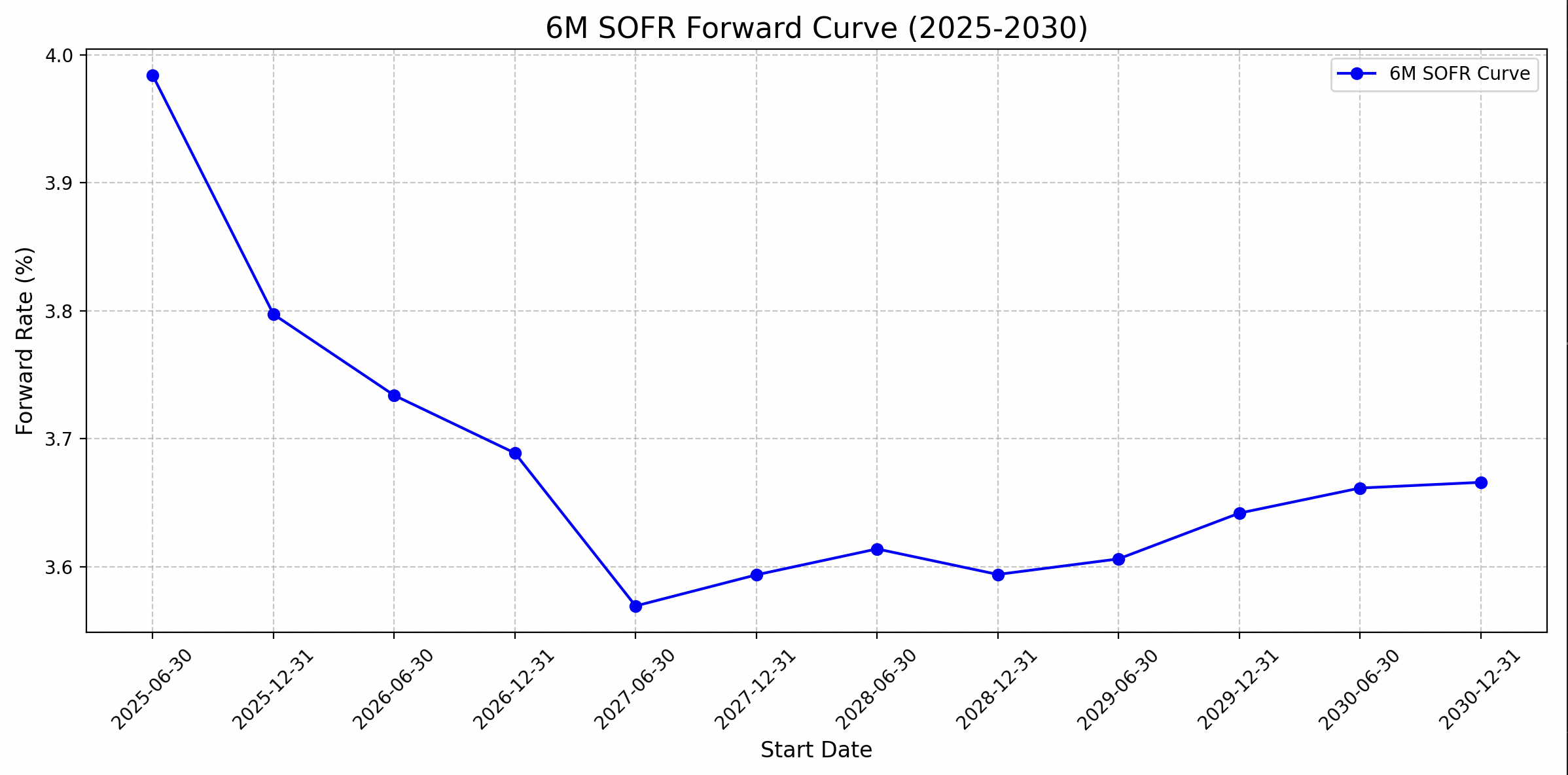

Step 4: Understand the Output

The graph plots the 6-month SOFR forward curve with:

- x axis: Predefined start dates

- y-axis: forward rates for 6M compounded SOFR

Try it Yourself!

Whether you're forecasting interest costs or performing valuations, the BlueGamma API makes it easy to fetch real-time swap rates and build forward curves. Request access to the API here.

Check out our other API tutorials on Euribor API and CORRA API.