This guide breaks down exactly what overnight index swaps are, how they work, and why they are the ‘gold standard’ for risk-free rates.

1. What is an Overnight Index Swap (OIS)?

An Overnight Index Swap (OIS) is a financial contract between two parties to swap interest rate payments for a specific period.

It is a type of ‘interest rate swap’ with a specific structure:

- One party pays a Fixed Rate (a rate agreed upon at the start).

- The other party pays a Floating Rate based on a daily ‘overnight’ reference rate (such as the SONIA rate in the UK or the Federal Funds Rate in the US).

The term ‘overnight’ is key here. Unlike older swaps that might update every 3 or 6 months, an OIS derives its value from an interest rate that is published every single day. While some sources loosely refer to this as an ‘overnight interest swap’, the correct industry term is always Overnight Index Swap.

Think of an OIS as a way to manage exposure to daily interest rate changes. One person wants certainty (Fixed Rate), and the other is willing to take the risk of the daily market moving (Floating Rate). The OIS meaning ultimately boils down to hedging against, or expressing a view on, central bank interest rate moves.

2. How Do Overnight Index Swaps Work?

Understanding how OIS works is easier if you break it down into two ‘legs’ (sides of the deal).

- The Fixed Leg: Party A agrees to pay a fixed interest rate (e.g., 3.0%) on a specific amount of money.

- The Floating Leg: Party B agrees to pay the ‘overnight index’ rate. This rate fluctuates daily.

Important Mechanics:

- Notional Amount: The swap is based on a theoretical amount of money (e.g., £10 million). However, this £10 million is never actually exchanged. It is just used to calculate the interest.

- Net Settlement: Most OIS contracts settle only once at maturity. The two parties do not swap the full interest payments; they only swap the net difference.

- If the accrued Floating interest is higher than the Fixed interest, the Floating payer pays the difference.

- If the Fixed interest is higher, the Fixed payer pays the difference.

In an OIS swap, money rarely changes hands until the contract ends. Because the principal amount isn’t exchanged, and the contract is usually settled on a ‘net’ basis, the risk of one party running away with the money is significantly lower than in a standard loan.

3. Overnight Index Swap Example

Let’s look at a simplified overnight index swap example to see the mechanics.

The Setup:

- Notional Value: £10,000,000

- Duration: 3 Days

- Party A: Pays Fixed Rate of 3.00%

- Party B: Pays Floating (SONIA/Overnight Rate)

The Daily Rates (Floating):

- Day 1: 2.90%

- Day 2: 2.95%

- Day 3: 3.15%

The Calculation:

In OIS, we do not simply average the percentages. The daily rates are annualised (divided by 360 or 365 depending on the currency) and compounded daily on the principal.

- Rough Geometric Average ≈ 3.00%

- Fixed Rate = 3.00%

In this scenario, the rates matched closely. However, if the Bank of England had hiked rates on Day 2 to 4.0%, the total floating interest would exceed the fixed interest. Since Party B is the ‘Floating Payer’, Party B would owe Party A the difference.

The maths behind OIS swaps relies on compounding daily interest (geometric averaging). While we use simple percentages in this example, real pricing models account for ‘day-count fractions’. Over a year on a billion-pound trade, the difference between simple averaging and daily compounding is massive.

4. The OIS Rate & Market Indices

When you see the term OIS rate, it refers to the Fixed Rate that the market is currently agreeing to. But what is the Floating side based on?

Different currencies use different ‘Overnight Indices’:

- GBP (UK): SONIA (Sterling Overnight Index Average).

- USD (United States): The Effective Federal Funds Rate (EFFR) or the Secured Overnight Financing Rate (SOFR).

- EUR (Europe): €STR (Euro Short-Term Rate).

When you look up an overnight index rate, you are looking at derivatives based on these central bank or market benchmarks.

The OIS rate you see on a terminal is not the same as the current Bank of England Base Rate or Fed Funds Rate. It is the market’s prediction of what the overnight rate will average out to be over the life of the swap.

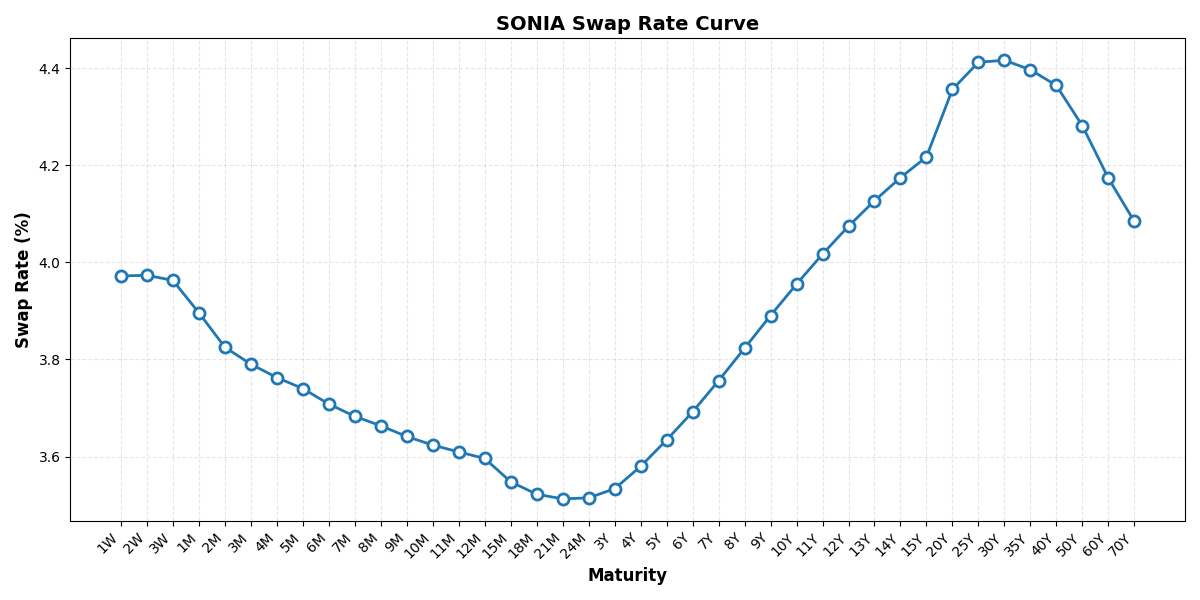

5. The Overnight Index Swap (OIS) Curve

While the "OIS rate" usually refers to a specific contract (like a 3-month swap), the OIS Curve is the graphical representation of OIS rates across all maturities, from one week out to 30 years or more.

The curve plots the market’s expectations for the daily overnight rate at every point in the future.

What the Curve Tells Us:

- The Short End (0–2 Years): This is highly sensitive to immediate central bank policy. If the curve is steep (rising sharply), the market expects the Bank of England or Fed to hike rates aggressively in the near term.

- The Long End (10+ Years): This reflects long-term views on inflation and the ‘neutral’ interest rate, rather than just the next policy meeting.

- Inversion: Just like a bond yield curve, the OIS curve can invert. If the 2-year OIS rate is higher than the 10-year OIS rate, the market is effectively pricing in rate cuts (or a recession) in the future.

OIS Curve vs Government Bond Curve

It is important to distinguish the OIS curve from the Government Bond curve (Gilts in the UK, Treasuries in the US).

- Government Bond Curve: Includes ‘supply and demand’ noise. If the government issues too much debt, yields might spike regardless of interest rate expectations.

- OIS Curve: Is purely an interest rate expectation curve. It is cleaner and generally considered the "truer" representation of risk-free money.

The difference between the two is known as the Swap Spread.

When analysts talk about the "Risk-Free Curve" today, they are almost always referring to the OIS Curve, not the government bond curve. Because OIS implies no exchange of principal, it is free from the supply-demand distortions that affect the bond market.

6. Why OIS is the Standard for Discounting

For decades, government bonds (such as US Treasuries or UK Gilts) were considered the ‘Risk-Free Rate’. However, bonds can be affected by supply and demand (scarcity of bonds).

Today, the OIS swap curve is the primary curve used to ‘discount’ (value) collateralised derivatives.

Why the switch?

- Collateralisation: Most modern derivatives are secured by cash collateral.

- Risk Profile: Because these trades are secured, they are effectively risk-free. Therefore, they should be valued using a risk-free rate.

- Stability: OIS tracks the central bank rate closely and is not distorted by bond supply shortages.

Note: While OIS is the standard for discounting derivatives, government bonds are still often used as the ‘risk-free’ benchmark for other regulatory purposes.

Banks use the OIS rate to value trillions of pounds in derivatives. If you hear about ‘CSA Discounting’ or ‘OIS Discounting’, it refers to using the OIS curve, not LIBOR or Gilts/Treasuries, to determine the present value of future cash flows.

7. OIS vs Standard Interest Rate Swaps (The Post-LIBOR World)

A common point of confusion is: "Can you have a standard interest rate swap based on OIS rates?"

The answer depends on where you are trading.

In the UK & US (Economic Similarity)

Since the discontinuation of LIBOR, standard swaps now reference overnight rates (SONIA in the UK, SOFR in the US).

- Similarity: Both Standard Swaps and OIS now reference overnight rates.

- Difference: Markets still distinguish between them. A ‘SONIA OIS’ usually refers to a swap tracking the specific overnight policy dates, while a ‘Standard SONIA Swap’ is used for broader duration management. They are economically similar but have different conventions.

In Europe (The distinct split)

Europe still distinguishes clearly between the two:

- Standard IRS: Usually tracks EURIBOR (includes bank credit risk).

- OIS: Tracks €STR (Risk-free overnight rate).

In GBP and USD, the ‘Standard Swap’ and ‘OIS’ have converged towards similar overnight structures. In EUR, they remain totally separate products (EURIBOR vs €STR). Always clarify the underlying index!

8. Uses of Overnight Index Swaps

Why is the index swaps market so huge? It is primarily used by banks, hedge funds, and swap dealers for three reasons:

- Pricing & Discounting: As mentioned, OIS is the mathematical foundation for valuing collateralised trades.

- Managing Short-Rate Exposure: Financial institutions use OIS to manage the risk of the central bank changing interest rates overnight. (Note: Corporate borrowers usually utilise Term Swaps, not OIS, to hedge their debt).

- Market Views: Traders use short-term OIS contracts (like the 1-month OIS) to express views on upcoming central bank meetings.

The ‘Front End’ of the OIS curve (short-dated contracts) is one of the most accurate predictor of central bank moves. If you want to know what the Bank of England or Fed will do next month, the overnight index swap rate is a better indicator than news pundits, as it reflects where institutions are actually placing their capital.

We can also use the Forward Curve to predict what central bank moves will be, check out our central bank forecasting pages, where we use the Forward Curve to predict what a central bank will do at their next meeting.

Bank of Canada Interest Rate Forecast