If you've ever fixed your interest rate through your lending bank, you've almost certainly been on one side of a back-to-back swap, even if you didn't know it.

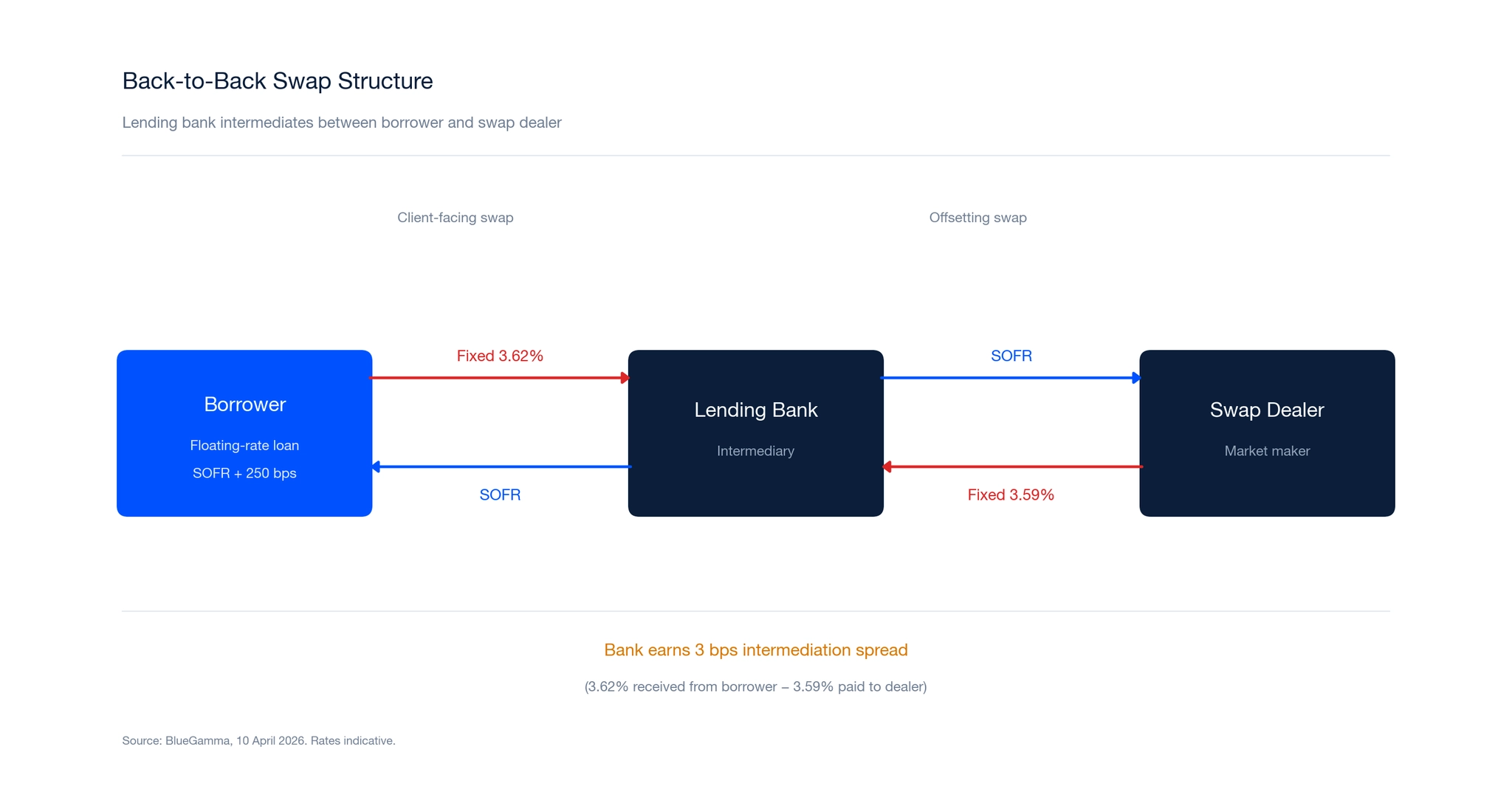

A back-to-back swap is a structure in which a lending bank enters into two offsetting interest rate swaps: one with its borrower (the client-facing swap) and a second, mirror-image swap with a swap dealer or the interbank market (the offsetting swap). The bank acts as an intermediary, earning a spread between the two transactions while transferring the interest rate risk to the broader derivatives market.

Back-to-back swaps are one of the most common structures in commercial lending. They allow borrowers to convert floating-rate loans to fixed rates through their existing banking relationship, without needing to access the derivatives market directly. For a broader overview of interest rate swap mechanics, see our guide to interest rate swaps.

How a Back-to-Back Swap Works

The structure involves three parties and two separate swap transactions.

Swap 1: Client-facing swap. The borrower enters into an interest rate swap with its lending bank. The borrower pays a fixed rate to the bank and receives a floating rate (typically SOFR or the relevant benchmark). The floating rate received under the swap offsets the floating rate on the underlying loan, leaving the borrower with a net fixed rate.

Swap 2: Offsetting swap. The lending bank enters into a mirror swap with a swap dealer or through the interbank market. In this swap, the bank pays a floating rate and receives a fixed rate. This second swap offsets the bank's exposure from the client-facing swap.

The bank's fixed rate received on Swap 2 will be slightly lower than the fixed rate charged to the borrower on Swap 1. The difference is the bank's intermediation spread.

Worked Example

Consider a commercial borrower with a $75 million floating-rate term loan at SOFR + 250 basis points. The borrower wants to fix their interest rate exposure for five years.

| Component | Rate | Direction |

|---|---|---|

| 5-Year SOFR mid-market swap rate | 3.59% | Reference |

| Swap 1 (Client-Facing) | ||

| Borrower pays fixed to bank | 3.62% | Borrower pays |

| Bank pays SOFR to borrower | SOFR | Bank pays |

| Swap 2 (Offsetting) | ||

| Bank pays SOFR to dealer | SOFR | Bank pays |

| Dealer pays fixed to bank | 3.59% | Dealer pays |

| Bank intermediation spread | 3 bps | 3.62% - 3.59% |

Swap rates sourced from BlueGamma. 5-year SOFR mid-market rate: 3.59%.

The mid-market swap rate of 3.59% used in this example is sourced from BlueGamma's live SOFR swap curve. Banks and borrowers can monitor these rates in real time through the BlueGamma web app, Excel add-in, or API.

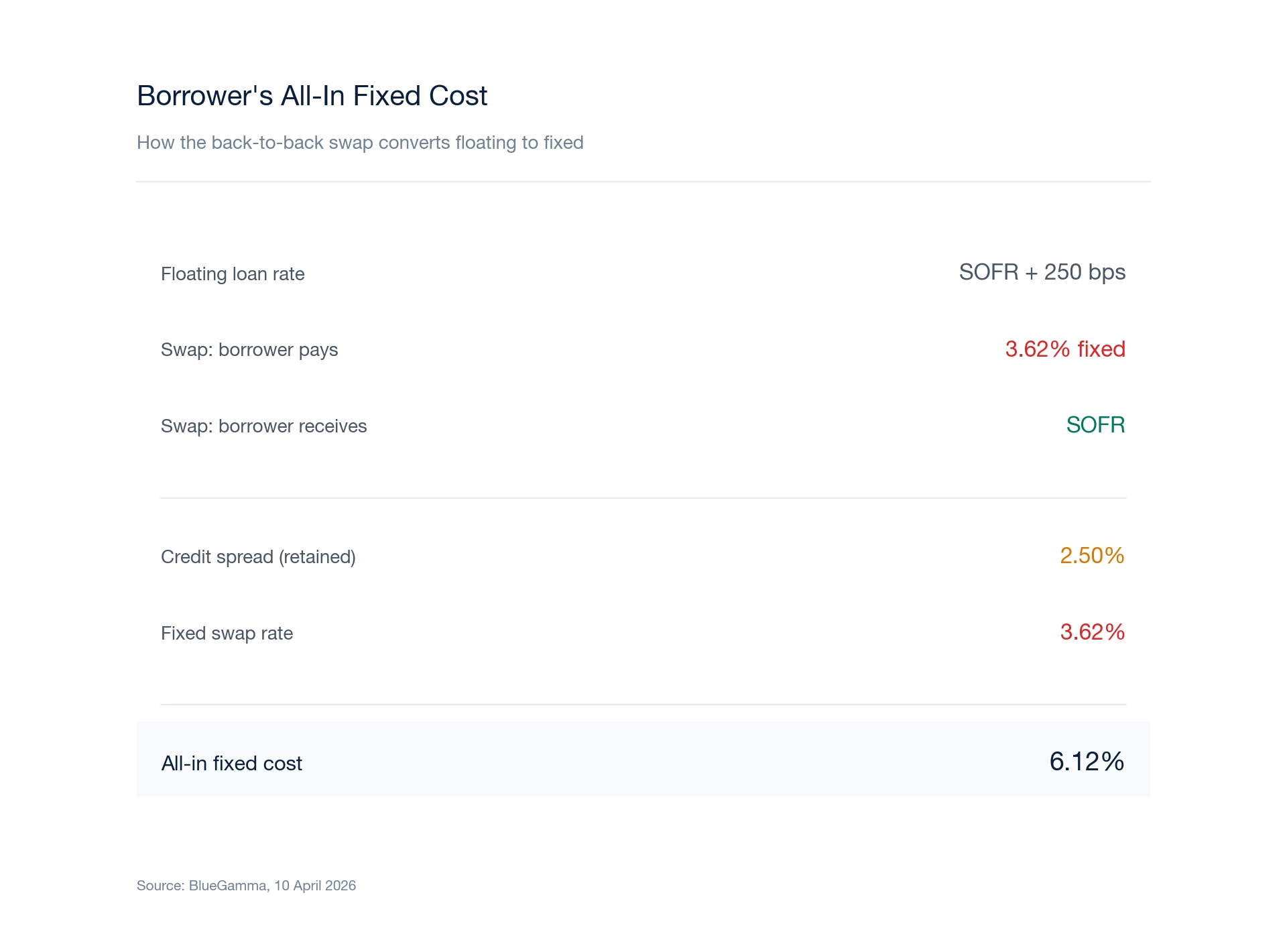

The borrower's effective all-in fixed rate is:

- Floating leg cancels: SOFR received on swap offsets SOFR paid on loan

- Credit spread retained: 250 basis points

- Fixed swap rate paid: 3.62%

- All-in fixed cost: 6.12%

The borrower has converted a floating-rate loan into a synthetic fixed-rate obligation. The lending bank earns 3 basis points per annum on $75 million ($22,500 per year) for intermediating the swap, with no residual interest rate risk.

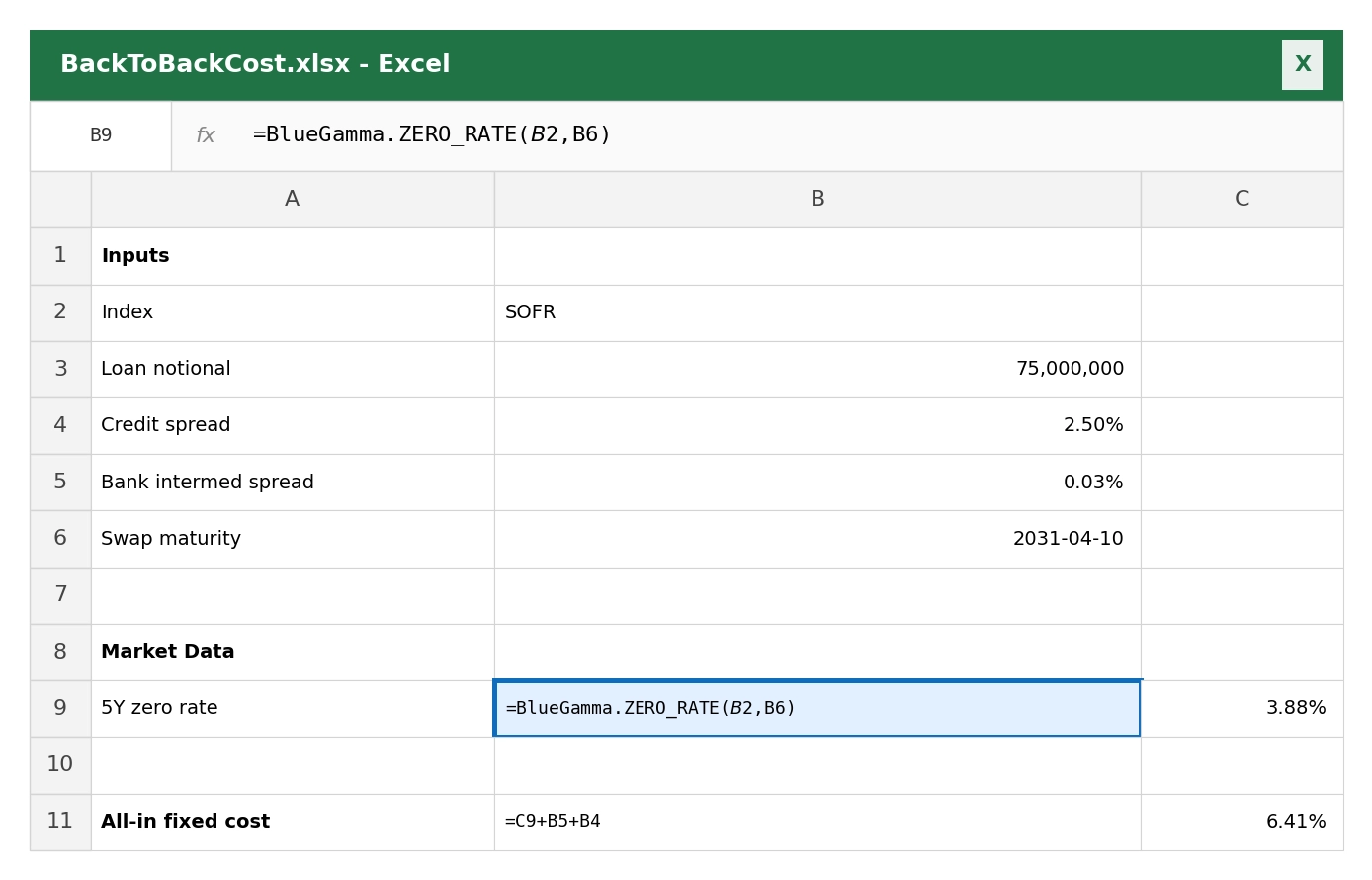

Calculating the All-In Borrower Cost in Excel

Many community banks and CRE borrowers model back-to-back swaps directly in Excel. Using the BlueGamma add-in, you can pull the mid-market swap rate and construct the all-in borrower cost.

The borrower's fixed cost is the sum of the mid-market swap rate, the bank's intermediation spread (typically 2 to 10 basis points), and the credit spread on the underlying loan. With the current 5-year SOFR mid-market rate around 3.59%, a 3 bps intermediation spread, and a 250 bps credit spread, the all-in fixed cost is approximately 6.12%.

Why Banks Use Back-to-Back Swaps

Risk management

Banks do not typically want to warehouse the interest rate risk from client-facing swaps. By entering an offsetting swap with the market, the bank eliminates its exposure to rate movements. The bank's profit is locked in at the spread between the two swaps, regardless of where rates move subsequently.

Revenue generation

The intermediation spread, while small on a per-transaction basis (typically 2 to 10 basis points), is a meaningful revenue source for commercial banks across their lending portfolio. On a large book of swaps, these spreads compound into significant fee income.

Client service

Borrowers prefer to transact with their lending bank rather than seeking out a swap dealer independently. The back-to-back structure allows the bank to offer hedging as an integrated part of the lending relationship, which strengthens the overall client proposition.

Why Borrowers Benefit

Simplicity

The borrower deals with a single counterparty (the lending bank) for both the loan and the hedge. Documentation is streamlined, and the swap terms typically align automatically with the loan terms (notional, amortisation schedule, payment dates).

Netting and collateral

Because the swap is with the lending bank, the bank can net the swap exposure against the loan collateral. This means the borrower often avoids posting separate collateral (variation margin) for the swap, which would be required if transacting directly with an external dealer under a standard CSA.

Integrated amortisation

The client-facing swap can be structured to amortise in line with the loan, including scheduled principal repayments and any mandatory prepayment provisions. This ensures the hedge remains right-sized throughout the loan's life.

Risks and Considerations

Credit risk. The bank is exposed to the credit risk of the borrower on the client-facing swap. If the borrower defaults, the bank may have an out-of-the-money position on Swap 1 that is not offset by the loan recovery. The offsetting Swap 2 with the dealer remains in force, potentially leaving the bank with a net loss.

Prepayment risk. If the borrower prepays the loan early, the client-facing swap may need to be terminated. The termination value depends on market conditions at the time. The bank must also unwind the corresponding portion of the offsetting swap, though this should be a matched transaction.

Spread compression. Competitive pressure in commercial lending has compressed intermediation spreads over time. Banks must balance the revenue from the swap spread against the operational and credit costs of providing the service.

Documentation. The client-facing swap is documented under a separate ISDA Master Agreement between the borrower and the bank. The offsetting swap is documented under the bank's existing ISDA with the dealer. Ensuring consistency between the two agreements (particularly around payment dates, day count conventions, and early termination triggers) is essential.

Regulatory treatment. Under the Dodd-Frank Act, certain standardised interest rate swaps must be cleared through central counterparties. A borrower that qualifies as a non-financial commercial end-user using the swap to hedge or mitigate commercial risk can elect the CFTC end-user exception to avoid mandatory clearing on the client-facing leg. The exception is not automatic: the borrower must be eligible (it must not be a "financial entity" as defined under the Commodity Exchange Act, which excludes many REITs, captive finance subsidiaries, and private funds) and must satisfy the CFTC's election and reporting requirements. The bank's offsetting swap with a dealer is typically subject to the clearing mandate where it falls within the CFTC's required classes.

Back-to-Back Swaps vs. Direct Market Hedging

| Feature | Back-to-Back (via Bank) | Direct Market Hedge |

|---|---|---|

| Counterparty | Lending bank | Swap dealer / cleared |

| Fixed Rate | Mid-market + bank spread (e.g. 3.62%) | Closer to mid-market (e.g. 3.59%) |

| Collateral | Often netted against loan collateral | Variation margin required (cash or securities) |

| Amortisation | Aligned with loan schedule | Must be specified separately |

| Documentation | Integrated with loan relationship | Separate ISDA required |

| Best For | Mid-market borrowers, integrated hedging | Larger corporates with existing dealer relationships |

For mid-market borrowers, the convenience and collateral benefits of the back-to-back structure typically outweigh the slightly higher fixed rate. For larger corporates with existing ISDA agreements and the ability to post collateral, direct market access may produce tighter pricing.

Summary

Back-to-back swaps are the standard mechanism through which commercial banks provide interest rate hedging to borrowers. The bank intermediates between the borrower and the derivatives market, earning a spread while eliminating its own interest rate risk.

With the 5-year SOFR swap rate at 3.59%, a typical back-to-back swap might result in the borrower paying 3.62% fixed, with the bank earning a 3 basis point intermediation spread. The borrower benefits from integrated hedging, simplified documentation, and favourable collateral treatment.

This article is for informational and educational purposes only and does not constitute financial, investment, legal, or tax advice. BlueGamma does not provide advisory services. Readers should consult qualified professional advisors before entering into any derivative transaction. Market data shown is indicative and sourced from BlueGamma as of the date stated.

Frequently Asked Questions

What is a back-to-back swap?

A back-to-back swap is a structure in which a lending bank enters into two offsetting interest rate swaps: one with its borrower and a mirror-image swap with a dealer or the interbank market. The two swaps cancel each other out from the bank's perspective, leaving the bank with no net interest rate risk and a locked-in intermediation spread.

Why do banks use back-to-back swaps?

Banks use back-to-back swaps to offer interest rate hedging to their borrowers without retaining the associated interest rate risk. The structure generates fee income through the bid-offer spread between the client-facing swap and the offsetting market swap, while allowing the bank to provide hedging as an integrated part of the lending relationship.

What is the difference between a back-to-back swap and a direct swap?

In a back-to-back swap, the borrower transacts with their lending bank, which then offsets the risk with a separate market counterparty. In a direct swap, the borrower transacts with a swap dealer or through a clearinghouse without the lending bank acting as intermediary. Back-to-back swaps typically carry a slightly higher fixed rate (reflecting the bank's intermediation spread) but offer benefits including simplified documentation, integrated amortisation with the loan, and favourable collateral treatment.