Refinancing your loan but stuck with an above-market swap? Blend and extend lets you restructure without the painful termination payment.

A blend and extend is a swap restructuring strategy in which a borrower combines an existing interest rate swap with a new swap extension, producing a single swap at a blended fixed rate over a longer term. Rather than terminating the original swap (which may involve a breakage cost) and entering a new one, the borrower merges the economics of both into one instrument.

This approach is commonly used when a borrower is refinancing or extending their underlying loan and wants to maintain an interest rate hedge without incurring a large upfront termination payment. For the underlying mechanics of swap mark-to-market, see our guide to derivative valuation.

The term "blend and extend" is also used in commercial real estate leasing, where a landlord and tenant renegotiate rent by blending the current lease rate with a new market rate in exchange for a longer lease term. This guide focuses on the interest rate swap and loan restructuring context.

How Blend and Extend Works

The underlying mechanic is simple: the borrower takes the mark-to-market of their existing swap and embeds it into a new swap at an off-market fixed rate. No cash changes hands, but the new swap's fixed rate is set above (or below) the current market rate by just enough to preserve the present value of the old position.

Step 1: Calculate the mark-to-market (MTM) of the existing swap. For a borrower paying an above-market fixed rate, the MTM is negative (a liability).

Step 2: Price a new swap at the desired extended term (e.g. 7 years) at current mid-market rates.

Step 3: Calculate the basis point value (BPV, also called PV01 or DV01) of the new swap. This is the change in the swap's present value per 1 basis point move in the fixed rate.

Step 4: Compute the spread that needs to be added to the mid-market rate so that the new swap's PV offsets the old swap's MTM:

Spread = −MTM / BPV of new swap

Step 5: The blended rate is the new mid-market rate plus this spread.

Blended Rate = New Mid Rate + (−MTM of old swap / BPV of new swap)

This isn't a novation in the legal sense. The transaction can be structured as a termination of the old swap with simultaneous execution of the new swap at the off-market rate, with no cash exchanged. Economically, it's the same as a formal blend and extend. The key point is that the value preservation is what matters, not the specific documentation path.

Worked Example

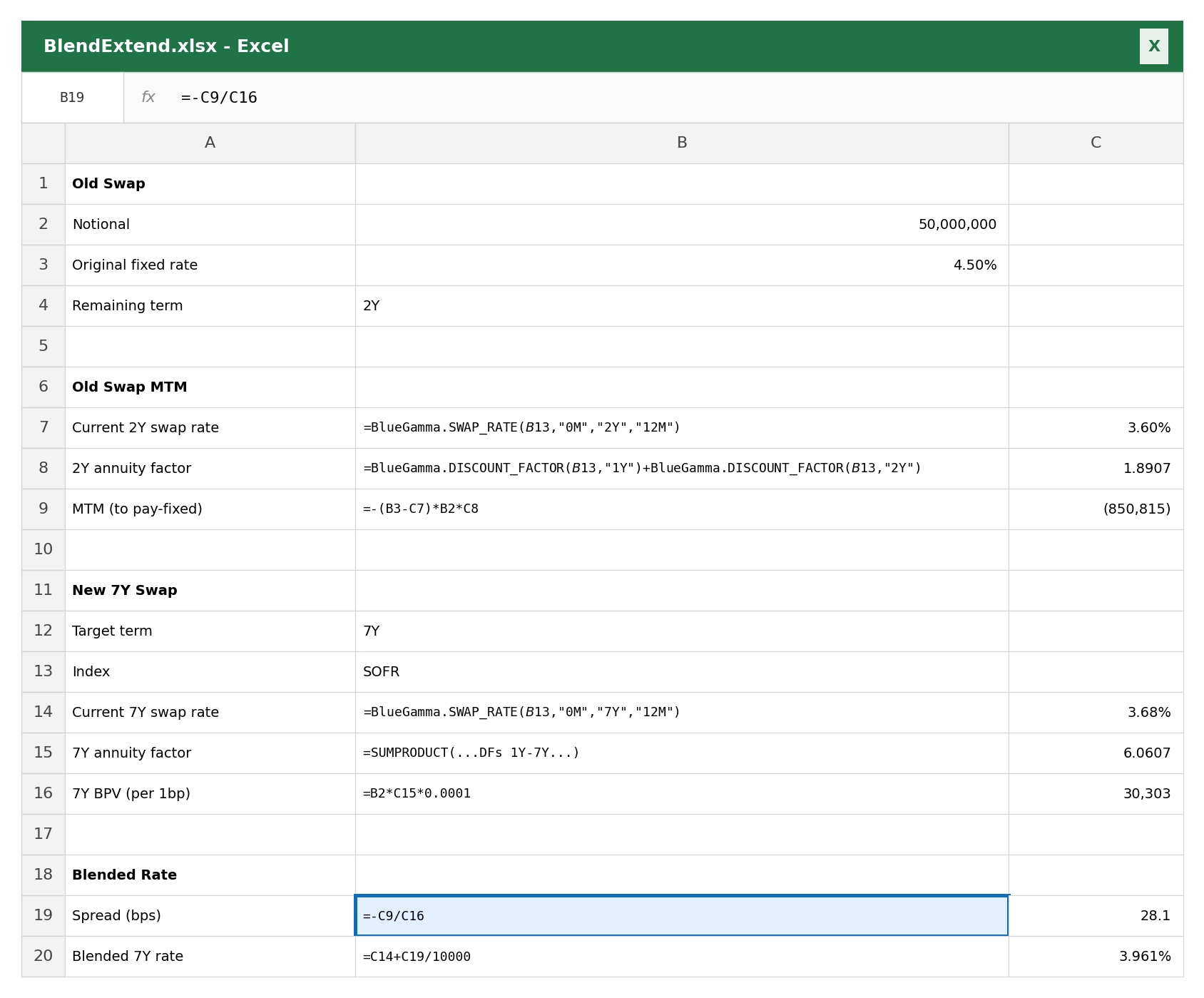

Consider a borrower with an existing pay-fixed swap at 4.50% on a $50 million notional with 2 years remaining. They are refinancing the underlying loan with a new 7-year facility and want to extend the hedge.

| Input | Value |

|---|---|

| Old swap fixed rate | 4.50% |

| Old swap remaining term | 2 years |

| Notional | $50,000,000 |

| Current 2Y SOFR swap rate | 3.60% |

| Current 7Y SOFR swap rate | 3.68% |

Step 1: Calculate the MTM of the old swap.

The borrower is paying 4.50% when the current 2Y market rate is 3.60% — that's 90 bps above market. The MTM (from the pay-fixed borrower's perspective) is approximately:

MTM ≈ −(4.50% − 3.60%) × $50M × 2Y annuity factor

MTM ≈ −0.90% × $50M × 1.8907

MTM ≈ −$850,815

The 2Y annuity factor (1.8907) is the sum of the discount factors to the remaining two annual payment dates, pulled from the SOFR OIS curve. The negative sign reflects that the borrower would owe this amount to terminate the swap today.

Step 2: Calculate the BPV of the new 7Y swap.

BPV (basis point value) is the change in the swap's present value per 1 bp move in the fixed rate. For a 7-year annual swap on $50M:

BPV = Notional × 7Y annuity factor × 0.0001

BPV = $50,000,000 × 6.0607 × 0.0001

BPV = $30,303 per bp

The 7Y annuity factor (6.0607) is the sum of discount factors for all seven annual payment dates.

Step 3: Calculate the spread over mid-market.

To embed the old swap's loss into the new swap, the fixed rate must be higher than mid-market by exactly the amount that offsets the old MTM:

Spread = −MTM / BPV = $850,815 / $30,303 = 28.1 bps

Step 4: Compute the blended rate.

Blended rate = 3.68% + 0.281% = 3.96%

The borrower's new 7-year swap is at 3.96%, which is 28 bps above the current 7-year market rate and precisely reflects the embedded cost of the old swap's negative MTM. No cash changes hands at execution. Over the life of the new swap, the borrower effectively pays the termination cost via the higher-than-market fixed rate.

Importantly, this approach is not dependent on any particular legal structure. Whether the bank documents it as a novation, an amendment, or a simultaneous termination plus new trade, the economics are identical. What matters is the value preservation: old swap MTM divided by new swap BPV gives the spread that makes the two options economically equivalent.

The borrower's new swap has a 7-year term at a blended rate of 3.96%. This is:

- 54 bps below the original swap rate (4.50%), providing immediate relief

- 16 bps above the current 7-year market rate (3.80%), reflecting the cost of carrying the above-market original swap

Importantly, no cash changes hands at the restructuring date. The mark-to-market loss on the original swap is effectively amortised into the blended rate over the extended period.

Calculating a Blended Rate in Excel

The BlueGamma Excel add-in pulls live swap rates, discount factors, and forward rates directly into your spreadsheet, letting you build a blend-and-extend calculator that produces the blended rate from live market data.

The calculator pulls the current 2Y and 7Y swap rates from the BlueGamma add-in, calculates the old swap's MTM using the current mid-market rate and 2Y annuity factor, computes the new 7Y swap BPV, and produces the blended rate as the new 7Y mid plus the offsetting spread.

When to Use Blend and Extend

Loan refinancing or extension

The most common trigger. When the underlying loan is refinanced or its maturity is extended, the borrower needs the hedge to cover the new loan term. Blend and extend aligns the swap with the new financing in a single transaction.

Avoiding a termination payment

If the existing swap has a negative mark-to-market (the borrower is paying an above-market rate), terminating the swap would require an upfront payment to the bank. In the example above, the negative MTM of the 2-year remaining swap at 4.50% might be approximately $800,000 to $1,000,000. Blend and extend avoids this cash outflow by spreading the cost over the extended term.

Reducing the current fixed rate

If market rates have fallen significantly below the borrower's original swap rate, a blend and extend provides immediate reduction in the fixed rate, improving current cash flow. The original rate of 4.50% drops to 3.96% from day one.

Hedge accounting considerations

Under ASC 815, a blend and extend is treated as a termination of the original swap and execution of a new one. The original hedge relationship is discontinued: amounts deferred in AOCI for a cash flow hedge are frozen and reclassified to earnings in line with the original hedged forecasted transactions. The new swap must be designated in a new hedge relationship if hedge accounting is to continue. Because the new swap has a non-zero fair value at inception (the embedded financing component representing the rolled MTM of the original swap), it introduces a source of ineffectiveness that must be considered in the effectiveness assessment. Borrowers for whom hedge accounting continuity is important should discuss the mechanics with their auditors before executing a blend and extend.

Key Considerations

The blended rate will always be between the old rate and the new market rate. If the original rate is above market (the common scenario), the blended rate provides immediate savings. If the original rate is below market (the borrower locked in at a favourable level), blending would increase the rate, which is typically undesirable.

The weighting is time-based. The longer the extension relative to the remaining term, the closer the blended rate will be to the current market rate. In the example, the 5-year extension dominates the 2-year remaining period, pulling the blend toward the market rate.

No free lunch. The blend and extend does not eliminate the mark-to-market loss on the original swap. It defers and amortises it into a higher rate than the borrower would otherwise achieve on a new standalone swap. The present value of the additional rate paid over the extended period equals the termination value of the original swap.

Notional adjustments. If the refinanced loan has a different notional amount than the original, the blend and extend calculation becomes more complex. The bank will adjust the blended rate to account for any change in notional.

Documentation. A blend and extend can be documented several ways: as a formal amendment of the existing ISDA trade, as a novation, or as a simultaneous termination of the old swap with a new off-market swap, with no cash exchanged. The economic outcome is the same. The specific documentation choice may affect hedge accounting continuity and legal treatment, so borrowers should discuss the preferred structure with their counterparty and auditors.

Blend and Extend vs. Terminate and Replace

| Feature | Blend and Extend | Terminate and Replace |

|---|---|---|

| Upfront cost | None (MTM amortised into rate) | Termination payment required |

| New fixed rate | Blended (above market) | Current market rate |

| Cash flow impact | Spread over extended term | Immediate payment, then market rate |

| Total economic cost | Equivalent (in present value) | Equivalent (in present value) |

| Best for | Cash-constrained borrowers, refinancings | Borrowers who prefer clean market-rate trades |

The total economic cost of both approaches is the same in present value terms. The difference is timing: blend and extend defers the cost, while terminate and replace crystallises it upfront.

Summary

Blend and extend is a practical restructuring technique that allows borrowers to extend their interest rate hedges without incurring an upfront termination payment. The blended rate is computed by adding a spread to the current mid-market rate for the new term, where the spread equals the old swap's MTM divided by the BPV of the new swap. This value-preservation approach produces the same economic outcome as terminating the old swap and entering a new one at market — the only difference is the timing of the cash flow.

Say with SOFR swap rates around 3.60% (2-year) to 3.68% (7-year), borrowers with above-market legacy swaps can embed the MTM cost into a longer-dated swap at a rate that reflects both the current market and the inherited loss.

This article is for informational and educational purposes only and does not constitute financial, investment, legal, or tax advice. BlueGamma does not provide advisory services. Readers should consult qualified professional advisors before entering into any derivative transaction. Market data shown is indicative and sourced from BlueGamma as of the date stated.

Frequently Asked Questions

What is a blend and extend swap?

A blend and extend swap is a restructuring technique in which an existing interest rate swap is combined with a new extension period to produce a single swap at a blended fixed rate over a longer term. Rather than terminating the original swap and paying a breakage cost, the borrower rolls the economics of the existing position into the new swap. The blended rate falls between the original swap rate and the current market rate for the extension period.

How is the blended rate calculated?

The blended rate equals the current mid-market rate for the new term plus a spread that offsets the old swap's mark-to-market. The formula is: Blended Rate = New Mid Rate + (−Old MTM / BPV of new swap), where BPV is the present value change per 1 basis point move in the fixed rate. For example, if the old swap has an MTM of −$850,815 and the new 7-year swap has a BPV of $30,303 per bp, the spread over the 3.68% mid-market rate is 28 bps, producing a blended rate of 3.96%.

When should you use blend and extend vs. terminate and replace?

Blend and extend is typically preferred when the borrower wants to avoid a large upfront termination payment, as the mark-to-market cost of the existing swap is amortised into the blended rate over the extended term. Terminate and replace is better suited for borrowers who have the liquidity to pay the termination cost and prefer to transact at the current market rate going forward. The total economic cost of both approaches is equivalent in present value terms.

Does a blend and extend save money?

A blend and extend does not save money in net present value terms compared to terminating the existing swap and entering a new one at the current market rate. The mark-to-market loss on the original swap is embedded in the higher blended rate rather than paid upfront. However, it does provide cash flow relief by eliminating the need for an immediate termination payment, which can be significant for borrowers with constrained liquidity or those who prefer to spread costs over time.