Every quarter, your finance team needs to know what your derivatives are worth. Whether it's for your accounts, your lenders, or your own decision-making, accurate valuation matters.

Derivative valuation (also called derivative pricing) is the process of determining the fair market value of a derivative contract at a given point in time. Whether the instrument is an interest rate swap, a cap, an FX forward, or a more complex structured product, the underlying principle is the same: calculate the present value of all expected future cash flows.

Accurate derivative valuation is essential for financial reporting, collateral management, hedge accounting, regulatory compliance, and informed decision-making around early termination or restructuring.

This guide covers the main valuation methodologies, the key market inputs, and practical considerations for corporate treasury teams.

The Foundation: Discounted Cash Flows

At its core, derivative valuation follows a simple framework:

- Project future cash flows based on current market conditions (forward rates, FX rates, volatility)

- Discount those cash flows to present value using the appropriate discount curve

- Sum the present values of all future cash flows to arrive at the derivative's mark-to-market value

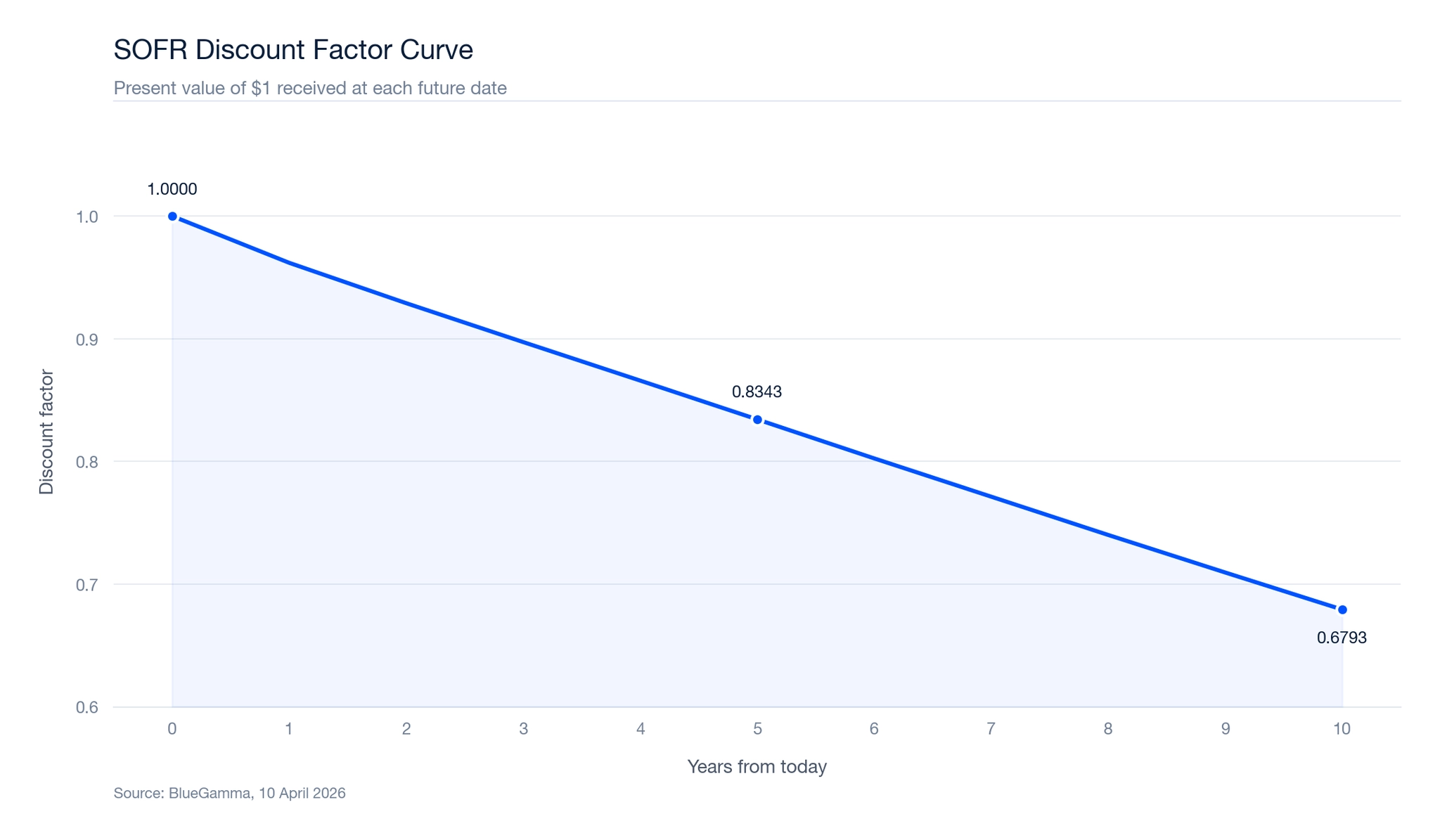

The discount curve translates future cash flows into present value. A dollar received in five years is worth less than a dollar today. The discount factor quantifies exactly how much less.

| Years | 0 | 1 | 2 | 3 | 5 | 7 | 10 |

|---|---|---|---|---|---|---|---|

| Discount Factor | 1.0000 | 0.9619 | 0.9290 | 0.8973 | 0.8343 | 0.7713 | 0.6793 |

Source: BlueGamma SOFR OIS discount curve.

A $1 million cash flow due in 5 years has a present value of $834,300. In 10 years, the same cash flow is worth only $679,300 today.

Valuation by Instrument Type

Interest Rate Swaps

A swap is valued by calculating the present value of each leg separately:

Fixed leg: Each future fixed payment is known and discounted using the relevant discount factor.

Floating leg: Each future floating payment is estimated using the forward rate for that period, then discounted.

The swap's mark-to-market value is the difference between the two legs. At inception, this difference is zero (the swap is priced at fair value). Over time, as rates move, one leg becomes more valuable than the other.

Example: Consider a 5-year SOFR swap entered 2 years ago at a fixed rate of 4.00%. Current 3-year swap rate (the remaining term) is 3.56%. The fixed-rate payer is paying above the current market rate, so the swap has a negative mark-to-market for the fixed-rate payer and a positive mark-to-market for the floating-rate payer.

To calculate the mark-to-market, each remaining cash flow is valued individually:

- For each future payment date, calculate the difference between the original fixed rate (4.00%) and the current market forward rate for that period

- Multiply the rate difference by the notional and the day count fraction for that period

- Discount each resulting cash flow to today using the appropriate discount factor

- Sum all discounted cash flows

As a rough approximation, the MTM can be estimated using the annuity factor (the sum of discount factors for remaining payment dates):

MTM ≈ (Current Par Rate - Original Fixed Rate) x Notional x Annuity Factor

MTM ≈ (3.56% - 4.00%) x $50M x 2.79 = approximately -$614,000

Here, 2.79 is the annuity factor (the sum of the three remaining annual discount factors: 0.962 + 0.929 + 0.897 = 2.79). This is a simplification. The exact calculation uses the full term structure of forward rates and individual discount factors for each cash flow, which may produce a somewhat different result.

Interest Rate Caps and Floors

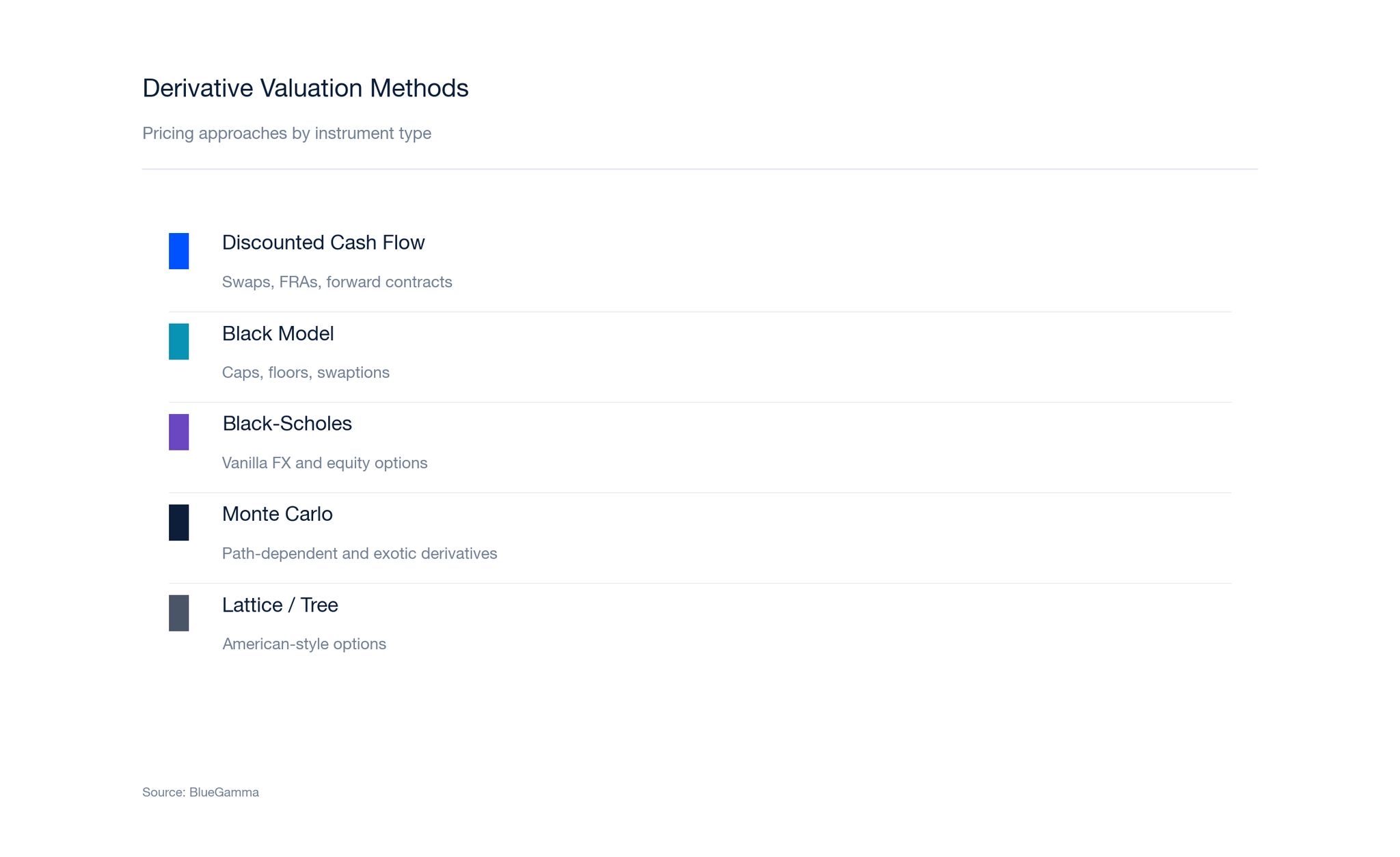

Caps and floors are valued as portfolios of options (caplets and floorlets). Each caplet is valued individually using the Black model or a more sophisticated volatility model (such as SABR).

The key inputs for each caplet are:

- Forward rate for the relevant period

- Strike rate

- Implied volatility (from the cap/swaption volatility surface)

- Discount factor to the payment date

- Time to expiry

The total cap value is the sum of all caplet values. For a detailed breakdown of caplet-level valuation, see our interest rate cap guide.

FX Forwards

An FX forward is valued by comparing the contracted forward rate with the current market forward rate for the same settlement date, then discounting the difference to present value.

MTM = Notional x (Current Forward Rate - Contracted Rate) x Discount Factor

Swaptions

Swaptions are valued using the Black model applied to swap rates, with the key inputs being the forward swap rate, the strike, implied volatility, and time to expiry.

Complex and Path-Dependent Derivatives

Monte Carlo simulation is the standard derivative pricing method for instruments whose payoff depends on the path of interest rates over time. Examples include range accruals, callable structures, and other path-dependent derivatives. The method generates thousands of random rate paths using calibrated stochastic models, calculates the payoff under each simulated path, and averages the discounted results to arrive at a fair value. Monte Carlo is computationally intensive but flexible, and it handles derivative pricing models that cannot be solved analytically. For most corporate derivatives (swaps, caps, forwards), closed-form solutions are faster and sufficient, but Monte Carlo remains essential for structured and exotic products.

Fetching Discount Curves via API

You can retrieve the SOFR discount curve programmatically using the BlueGamma API:

import requests

# Fetch SOFR discount curve for derivative valuation

response = requests.get("https://api.bluegamma.io/v1/discount_curve", params={

"index": "SOFR",

"start_date": "2026-04-09",

"end_date": "10Y",

"frequency": "12M"

})

curve = response.json()

for point in curve['curve'][:5]:

print(f"{point['date']}: DF = {point['discount_factor']:.6f}")Response:

{

"curve": [

{"date": "2026-04-09", "discount_factor": 1.000000},

{"date": "2027-04-30", "discount_factor": 0.961886},

{"date": "2028-04-30", "discount_factor": 0.928991},

{"date": "2029-04-30", "discount_factor": 0.897341},

{"date": "2030-04-30", "discount_factor": 0.865925}

]

}Valuing a Swap in Excel

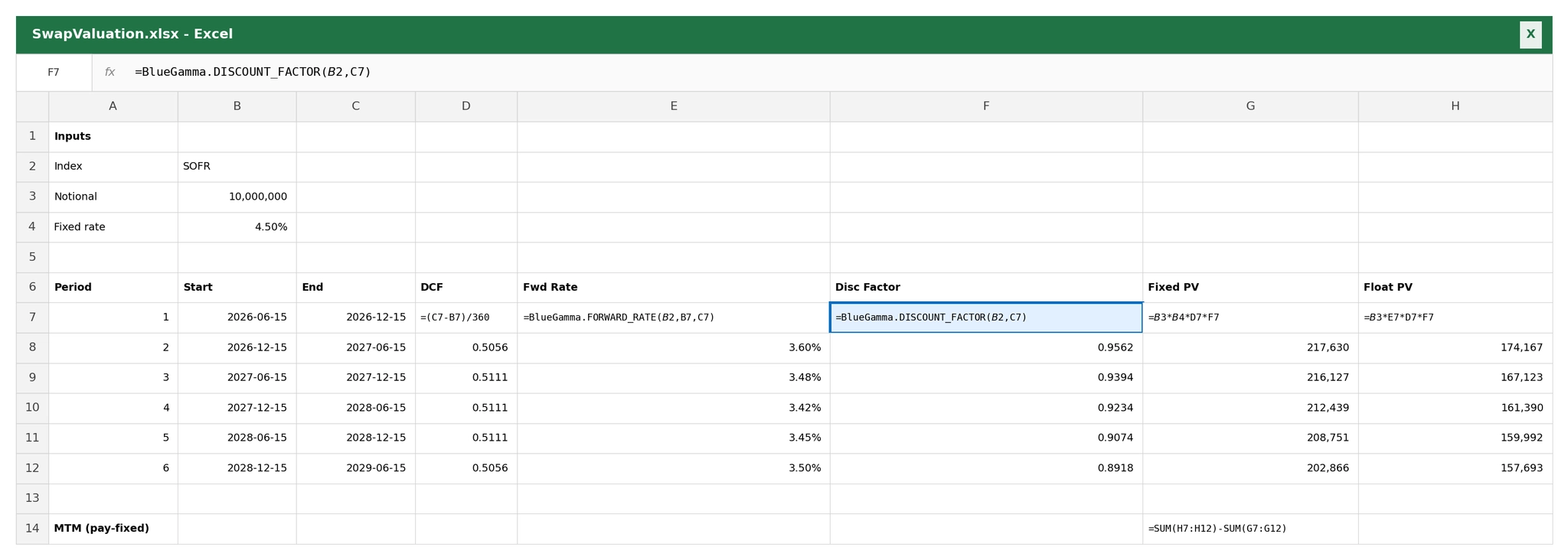

For day-to-day derivative valuation work, many treasury teams prefer Excel. The BlueGamma add-in pulls the same live data used by the web app and API directly into your spreadsheet.

The BlueGamma add-in automatically refreshes with live market data whenever Excel recalculates, producing a live mark-to-market for the swap from the fixed payer's perspective.

Key Market Inputs

Accurate valuation depends on reliable market data. The critical inputs are:

Interest rate curves. The discount curve (for present-valuing cash flows) and the forward curve (for projecting future floating rates). These are constructed from market-observable swap rates, futures, and overnight index swap rates. BlueGamma constructs these curves from live market data across all major currencies. The full discount curve, forward curve, and swap curve are available through the web app, Excel add-in, and API.

Volatility surfaces. For options-based instruments (caps, floors, swaptions), implied volatility is a critical input. The volatility surface maps implied vol across different strikes and expiries.

FX rates. Spot and forward exchange rates for cross-currency instruments.

Credit spreads. For instruments with credit-sensitive counterparties, credit valuation adjustments (CVA) may be applied.

Why Derivative Valuation Matters

Financial reporting

Under IFRS 9, ASC 815, and ASC 820, derivatives must be reported at fair value on the balance sheet. Under ASC 820 (US GAAP) and IFRS 13, fair value is defined as the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants. Accurate valuation is essential for financial statement preparation and audit compliance.

Collateral management

Derivatives traded under bilateral CSA agreements or cleared through central counterparties require regular mark-to-market calculations to determine collateral (margin) requirements. Inaccurate valuations can lead to disputed margin calls.

Hedge accounting

Hedge effectiveness testing compares the change in value of the hedging instrument with the change in value of the hedged item. This requires consistent and accurate valuation of both sides.

Early termination decisions

When considering whether to unwind or restructure a derivative, the mark-to-market value determines the termination payment. Understanding the current value helps borrowers make informed decisions about refinancing, blend and extend strategies, and other restructuring options. The same DCF framework underlies the fair value measurement of debt instruments under ASC 820 and IFRS 13. These mark-to-market values are available on BlueGamma to help evaluate termination or restructuring decisions.

Regulatory compliance

Financial institutions are required to value their derivative portfolios regularly for capital adequacy, risk reporting, and regulatory submissions.

Common Valuation Challenges

Curve construction differences. Different market participants may construct their curves differently, leading to small but meaningful valuation differences. Standardising on a consistent curve construction methodology (such as OIS discounting) reduces these discrepancies.

Volatility model selection. The choice between flat volatility, SABR, or other smile models can produce different valuations for the same instrument, particularly for deep out-of-the-money or in-the-money options.

Day count conventions. Seemingly minor differences in day count conventions (Actual/360 vs Actual/365 vs 30/360) can affect valuations, especially for large notionals or long tenors.

Timing of market data. Derivative valuations can change significantly intraday. Ensuring that all market inputs (rates, FX, volatility) are sourced at the same point in time is important for consistency.

Summary

Derivative valuation reduces to a simple principle: project future cash flows and discount them to present value. The complexity lies in the market inputs (curves, volatility surfaces, FX rates) and the models used to estimate future cash flows for instruments with optionality.

With the current SOFR discount curve showing discount factors ranging from 0.9619 at 1 year to 0.6793 at 10 years, the time value of money remains a significant factor in derivative valuations across all tenors.

This article is for informational and educational purposes only and does not constitute financial, investment, legal, or tax advice. BlueGamma does not provide advisory services. Readers should consult qualified professional advisors before entering into any derivative transaction. Market data shown is indicative and sourced from BlueGamma as of the date stated.

Frequently Asked Questions

How are derivatives valued?

Derivatives are valued by projecting all expected future cash flows based on current market conditions (forward rates, FX rates, volatility) and discounting them to present value using the appropriate discount curve. The sum of these discounted cash flows is the derivative's fair value, or mark-to-market value. The specific derivative pricing models used depend on the instrument type.

What is mark to market for derivatives?

Mark to market is the process of revaluing a derivative contract based on current market data to determine what it would cost to enter into or unwind the position today. A positive mark-to-market value means the contract is an asset to the holder; a negative value means it is a liability. Mark-to-market values change continuously as market rates, volatilities, and credit conditions move.

What inputs are needed to value an interest rate swap?

The primary inputs are the discount curve (for present-valuing cash flows), the forward rate curve (for projecting future floating-rate payments), the original fixed rate, the notional amount, and the payment schedule including day count conventions. For collateralised swaps, the OIS discount curve (such as SOFR) is used for discounting.

How often should derivatives be revalued?

The frequency depends on the use case. For financial reporting under IFRS 9 or ASC 815, derivatives are revalued at each reporting date (typically quarterly). For collateral management under CSA agreements, daily or even intraday revaluation is standard. For internal risk management and decision-making, weekly or monthly revaluation is common for corporate treasury teams.